BABY - Smart Woman Securities

advertisement

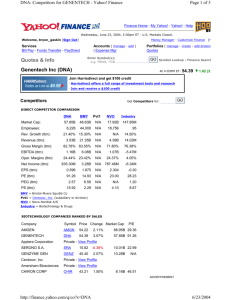

Aleksandra Prokop Sunday, April 22, 2007 Natus Medical, Inc. (BABY) Closing Price: 18.10 General Pitch Natus is a BUY as this is the perfect opportunity to take advantage of this solid company poised for relatively large growth in the near future. Background The Sector (Medical Appliances and Equipment) The Medical Appliances and Equipment sector of the Health Care industry is unique in that it is almost wholly focused on creating products for health care providers rather than direct consumers. The sector encompasses a wide variety of products ranging from diagnostic tools to monitoring systems to general hospital equipment (such as hospital beds, machines, and other related products). Like most health care sectors, Medical Appliances and Equipment faces some rather extensive day-to-day volatility. However, the nature of the sector’s products and services and the limited number direct-to-consumer purchases make this sector a little less vulnerable to economic and consumer-induced fluctuations. The sector’s market cap leader and most famous corporation is Medtronic, Inc. The Company Natus Medical, Inc. was founded in 1987 in San Carlos, California where the company’s headquarters are still located. Natus’s website cites its goal as being, “To improve outcomes and patient care in target markets through innovative screening, diagnostic & treatment solutions”1 with a focus on infant care. They have a wide range of diagnostic tools as well as products to help children with a variety of diseases, most notably hearing impairment. Their five major product categories are Newborn Hearing Screening, Diagnostic Hearing Assessment, Monitoring Systems for Neurology, Diagnostic Sleep Analysis and Newborn Care, including treatment for brain injury and jaundice Recently the company has expanded its product line through three major acquisitions (Bio-logic Systems Corporation, Deltamed S.A. and Olympic Medical, Inc.) and is becoming more involved in creating data management systems. Natus provides products both directly and through distributors to doctors, hospitals, nurses, and government agencies, and has a global presence in over 80 countries worldwide. 1 Natus Corporate Profile. http://www.natus.com/index.cfm?page=company_1&crid=2 Leadership Jim Hawkins = CEO (April 2004)2 Steven J. Murphy = CFO (February 2006) Dr. Christopher Chung, MD = In charge of R&D (June 2003) Mostly educated on the west coast, Natus management is seen as rather conservative and invested in the long-term growth of the company. Their three acquisitions from the last year thus suggest that these were all great buys that have large potential for the company3. 2 Natus Corporate Profile. The Motley Fool. Natus Medical vs. Under Armor. http://www.fool.com/investing/general/2007/03/16/natusmedical-vs-under-armour-natus-medical.aspx 3 Competition DIRECT COMPETITOR COMPARISON4 BABY Pvt1 VAS Pvt2 Industry Market Cap: 373.56M N/A 1.11B N/A 238.14M Employees: 360 N/A 2,365 N/A 293 127.80% N/A 18.60% N/A 12.50% Revenue (ttm): 89.92M N/A 610.42M N/A 78.40M Gross Margin (ttm): 62.69% N/A 47.69% N/A 52.59% EBITDA (ttm): 18.02M N/A 96.18M N/A 5.18M Oper Margins (ttm): 14.12% N/A 10.08% N/A 1.60% -927.00K N/A 28.99M N/A -998.25K EPS (ttm): -0.047 N/A 0.871 N/A N/A P/E (ttm): N/A N/A 38.69 N/A 27.82 PEG (5 yr expected): 0.78 N/A 1.32 N/A 1.47 P/S (ttm): 4.09 N/A 1.83 N/A 3.61 Qtrly Rev Growth (yoy): Net Income (ttm): Natus is in a unique position in that most of their direct competition is privately owned and thus an unlikely stock competitor at this point. As an added strong point, Natus will often partner with competitors in large-scale initiatives (such as Welch Allyn and a recent focus on improving hearing impairment products). Thus, the company obviously has a strong understanding of who their competition is and continuously keeps an eye on this competition. While much smaller than other healthcare industry leaders (such as Medtronic or even a closer competitor, Viasys), Natus has more room to grow in a strong niche market that still has the advantage of a wide range of products. Natus is the only sector leader to have specific segments dedicated to infant care. Out of the whole sector, Natus has a much lower PEG, suggesting that the company is highly undervalued currently. Thus, it may be the perfect time to take advantage of this favorable position. 4 Yahoo Finance. Investment Risks The greatest investment risks that Natus faces right now involve its recent acquisitions. Having made three major corporate purchases, the company’s balance sheet looks relatively week right now with income in the negative range. Another factor of concern with Natus is that it does not have a history of moving very quickly. It is a slow, steady grower that may not show incredible stock returns in the next few months. Investment Opportunities In its favor, Natus finds itself in the dominant position of a niche market with a wide variety of products and services. This position is reflected in the fact that the company is facing substantial quarterly revenue growth (it is fourth out of 111 companies in the sector) and has a great operating margin. Furthermore, its strong management team and the high level of positive PR around the company’s products suggest that Natus is in a good place as a corporation overall. In response to the fact that Natus faces a negative income statement, this is easily explained by its recent acquisitions. With three new company’s under its belt, Natus is just getting ready to surface from its previous low balance sheet. Although a slightly more aggressive strategy than before, the purchasing of these companies is a signal from the management that they have faith in the company’s ability to handle this change and that these are promising prospects. The fact that one of Natus’s newest product awards was just received for a product manufactured under one of its acquisitions speaks in favor of this viewpoint. While not usually a huge grower, Natus is primed for one of its strongest growth spurts since going public in 2001. In the next year or so Natus should begin to reap the rewards of its latest acquistions, come out of its balance sheet concerns, and find its stock price reflecting its newly strengthened position within the sector. Financials5 Revenue Cost of revenue Gross profit Operating expenses: Marketing and selling Research and development General and administrative Acquired in-process research and development Restructuring Total operating expenses Income (loss) from operations Other income, net Income (loss) before provision for income tax Provision for income tax Income (loss) from continuing operations Discontinued operations Net income (loss) Earnings (loss) per share: Basic Continuing operations Discontinued operations Net income (loss) $ $ $ $ 89,915 $ 33,665 56,250 43,045 $ 16,092 26,953 36,506 15,015 21,491 21,944 10,604 11,004 9,800 — 53,352 2,898 225 3,123 4,050 (927) — (927) $ 11,396 4,318 5,806 — — 21,520 5,433 1,228 6,661 509 6,152 — 6,152 $ 11,305 3,672 6,626 470 776 22,849 (1,358) 310 (1,048) 297 (1,345) (1,062) (2,407) (0.05) $ — (0.05) $ 0.35 $ — 0.35 $ (0.08) (0.06) (0.14) Operating activities: Net income (loss) $ (927) $ Adjustments to reconcile net income (loss) to net cash provided by operating activities: Acquired in-process research and development 9,800 Accounts receivable reserves 18 Excess tax benefits on the exercise of stock options (1,051) Inventory reserves 278 Depreciation and amortization 3,921 Loss on disposal of property and equipment — Warranty reserves 553 Share based compensation 1,405 Changes in operating assets and liabilities, net of assets and liabilities acquired in acquisitions: Accounts receivable (5,683) Inventories (2,045) Other assets (1,271) Accounts payable (201) Deferred taxes (1,899) Accrued liabilities (493) Deferred revenue 828 Net cash provided by operating activities 3,233 5 Official EDGAC online filing of the company’s 2006 10-K. 6,152 $ (2,407) — (253) — 25 1,988 — 206 — 470 82 — 529 1,849 643 83 367 (1,567) 840 (465) (131) (930) 1,858 160 7,883 (769) 903 (95) (125) — 1,487 (221) 2,796 Investing activities: Acquisition of businesses, net of cash acquired Sale of land, net of costs Acquisition of property and equipment Deposits and other assets Purchases of short-term investments Sales of short-term investments Redemption (purchase) of long term investment Net cash provided by (used in) investing activities (71,773) (480) (5,401) 2,492 — — (2,432) (931) (1,876) 83 10 79 — (24,866) (31,976) 12,163 32,188 40,779 — — 341 (59,467) Valuation6 VALUATION MEASURES Market Cap (intraday): 365.83M Enterprise Value (10-Apr-07)3: 358.38M Trailing P/E (ttm, intraday): N/A Forward P/E (fye 31-Dec-08) 1: 25.43 PEG Ratio (5 yr expected): 0.80 Price/Sales (ttm): 4.16 Price/Book (mrq): 3.69 Enterprise Value/Revenue (ttm)3: 3.99 Enterprise Value/EBITDA (ttm)3: 19.884 Forward PE = 25. 3 The forward PE is high, however this may signal that people are valuing the stock highly and that it will likely face even more impressive growth in the near future. Initial Public Offering (2001) = $11.00 Most recent drop = around March 2006 when there was an announcement in the increase of common stock to finance activities such as debt and proposed acquisitions. 6 Yahoo Finance. Splits:none Reiteration of the Pitch This would be the perfect time to buy this relatively steady performer. Natus may get some unexpected growth in the next few years, while R&D and pipeline products in established parts of the business continue to be strong. This would bring the stock price up in the near future. A good sell price, based on the company’s performance in the last year and consideration of the factors mentioned above, is estimated at about $23.