lafarge surma cement limited - International Leasing Securities Limited

advertisement

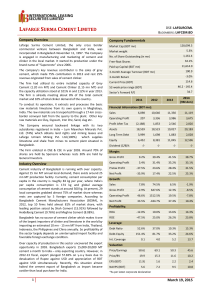

LAFARGE SURMA CEMENT LIMITED Company Overview Company Fundamentals Lafarge Surma Cement Limited – the only cross border commercial venture between Bangladesh and India – was incorporated on November 11, 1997. The Company is engaged in manufacturing and marketing of cement and clinker in the local market. To conduct its operation, it extracts and processes the basic raw materials limestone from its own quarry in Meghalaya, India. The raw materials are transported through a 17-km cross-border conveyor belt from the quarry to the plant. It started its production under the brand name of “Supercrete” since 2006. As per 2012 Annual Report, the firm had utilized its entire installed capacity of Grey Cement (1.20 mn MT) and Cement Clinker (1.15 mn MT) which was 73.75% and 42.17% in year 2011. The firm is already meeting about 8% of the total cement market and 10% of total clinker demand of the country. Market Cap (BDT mn) The Company ensured backward linkage with its two subsidiaries registered in India – Lum Mawshun Minarals Pvt. Ltd. (74%) which obtains land rights and mining leases and Lafarge Umiam Mining Pvt. Ltd.(100%) which supply limestone and shale from mines to cement plant situated in Bangladesh. The Firm enlisted in DSE & CSE in year 2003. Around 70% of shares are held by Sponsors whereas rests 30% are held by General Investors. Industry Overview 56,558.9j 2.5% Market weight 1,161.4 No. of Share Outstanding (in mn) 30.0% Free-float Shares 11,614.0 Paid-up Capital (BDT mn) 85.5 3-month Average Turnover (BDT mn) 3-month Return 55% Current Price (BDT) 48.7 28.4-49.7 52-week price range (BDT) 20.2 Sector’s Forward P/E 2010 2011 2012 2013 (9M Ann) Financial Information (BDT mn): 5,655 6,098 10,640 11,008 Operating Profit (1,115) 207 3,336 4,033 Profit After Tax (1,620) (2,188) 1,853 1,897 Assets 17,915 18,559 18,523 18,617 Long Term Debt 4,961 3,999 1,698 2,167 Equity 2,768 6,452 8,381 9,913 -/- -/- -/- -/- 10.2% 9.2% 39.4% 42.5% Operating Profit -19.7% 3.4% 31.4% 36.6% Pretax Profit -32.4% -37.5% 23.6% 27.9% Net Profit -28.6% -35.9% 17.4% 17.2% Sales -25.0% 7.8% 74.5% 3.5% Gross Profit -80.0% -3.0% 647.6% 11.7% Operating Profit -146.7% -118.5% 1512.5% 20.9% Net Profit -262.7% 35.1% -184.7% 2.3% Sales Dividend (C/B)% Margin: Cement industry of Bangladesh is running with over capacity. Against 15 mn MT annual local demand, there exists around 25 mn MT production facility. Currently, cement consumption per capita in the country is roughly 83 kg per year, where India’s per capita consumption is 174 kg and global average consumption of cement stands at around 500 kg. At present, 29 local companies grabbed almost 75% of market share whereas rests are captured by 5 foreign companies. According to Bangladesh Cement Manufacturers Association (BCMA), in 2012, top 10 firms held almost 81% of market share, with leading position seized by Shah Cement (15.91%) followed by Heidelberg Cement (9.76%) and Meghna Cement (8.08%). Gross Profit Bangladesh has no source of cement clinker which makes it one of the largest importers of clinker and limestone in the world by importing an estimated 10 mn - 15 mn MT from India, Thailand, Indonesia, the Philippines and China annually. So profitability of the sector largely depends on uninterrupted import facility and favorable foreign exchange condition. ROA -9.2% -12.0% 10.0% 10.2% ROE -45.0% -47.5% 25.0% 20.7% Debt Ratio 72.8% 52.6% 37.0% 23.5% Debt-Equity 471.2% 151.4% 81.7% 44.1% Over capacity of production in this sector uncovered the export opportunity in 2003. Bangladesh exports 15,000-20,000 MT cement a month to India – only exporting country. However, in 2012-13 fiscal, export plunged 57.82% on y-o-y basis due to devaluation of Rupee against USD and appreciation of BDT against USD simultaneously. Recently, this situation almost halted the cement export of Bangladesh as import became costlier than local purchase for India. Int. Coverage (1.5) 0.1 4.0 3.9 Price/Earnings N/A N/A 20.6 21.8** Price/BV 11.8 (1.4) 6.0 (1.9) 5.3 1.6 3.5* 2.2* 4.8 4.4 6.2 9.5* 1 Growth: Profitability: Leverage: Valuation: Restated EPS (BDT) NAVPS (BDT) *As per latest corporate declaration for the year ended 2013 March 20, 2014 Investment Positives Quarterly (3 Months) Restated EPS (BDT) On 10 March 2013, the Company had signed a three year agreement with Madina Cement Industries Ltd. According to the agreement Madina Cement Industries will produce Portland Composite Cement exclusively for Lafarge Surma which will be marketed under the brand name of “Powercete” along with the existing brand “Supercrete”. This indicates increasing demand of firm’s product and higher expected revenue. The firm reduced its huge accumulated loss of BDT 534 crore to only BDT 94 crore. Specifically, in Q4 2013, it registered remarkable profit of BDT 112.3 crore. The Company enjoyed, on an average, around 40% gross profit margin; whereas other players in the industry can avail gross profit margin up to 15% - 20%. The reason is the firm has competitive edge in getting raw materials through its own resources while others have to import the raw materials from abroad. 0.53 0.53 0.60 0.40 0.31 0.31 0.13 Q1 Q2 Q3 Q4 Q1 2012 Q2 Q3 Q4 2013 Last 5 Year's Price Movement (BDT) 90 80 70 60 50 40 30 Investment Negatives 0.97 20 As per 2013 corporate declaration, the Company has accumulated loss of around BDT 94 crore and therefore declared no dividend. As a result, the firm remained as “Z” category in the bourses. The Company has already utilized its existing production capacity fully; therefore, it has to go for contractmanufacturing (i.e., outsource the finished-goods from other manufacturers) which will naturally be more costly than own production. Pricing Based on Relative Valuation: Sector Forward P/E 19.9 Value (BDT) 43.6 Sector Trailing P/E 26.5 42.3 Market Forward P/E 17.4 38.1 Market Trailing P/E 17.8 28.4 3.8 36.1 Multiple Sector P/B 10 0 Mar-09 Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 Concluding Remark Lafarge Surma Cement Ltd. is one of largest foreign investments in Bangladesh (USD 280 mn). The firm suffered from losses due to operational interruption from April 2010 to August 2011; as India's High Court halted mining limestone from Meghalaya because of environmental concerns. This issue was resolved under some conditions by India's Supreme Court’s verdict. During that time, the Company experienced huge losses (BDT 534 crore). The situation is, however, gradually improving in recent times. The Company has reported phenomenal performance in Q4 of 2013 (BDT 112.3 crore) which helped to reduce its existing accumulated loss to BDT 94.5 crore. As on date, 14-days RSI and 14 MFI of the Company were 64.70 and 78.50 respectively. Source: Annual Reports, Lafarge Surma’s website, the Financial Express, the Daily Star, ILSL Research . ILSL Research Team: Name Rezwana Nasreen Towhidul Islam Md. Tanvir Islam Designation Head of Research Research Analyst Research Analyst For any Queries: research@ilslbd.com Disclaimer: This document has been prepared by International Leasing Securities Limited (ILSL) for information only of its clients on the basis of the publicly available information in the market and own research. This document has been prepared for information purpose only and does not solicit any action based on the material contained herein and should not be construed as an offer or solicitation to buy or sell or subscribe to any security. Neither ILSL nor any of its directors, shareholders, member of the management or employee represents or warrants expressly or impliedly that the information or data of the sources used in the documents are genuine, accurate, complete, authentic and correct. However all reasonable care has been taken to ensure the accuracy of the contents of this document. ILSL will not take any responsibility for any decisions made by investors based on the information herein. 2 March 20, 2014