Morningstar Income Equities Portfolio

Australia & New Zealand

Quarterly Update March 2015

Gareth James

Portfolio Overview

Senior Equity Analyst

The Morningstar Income Equities Portfolio rose an impressive11.0% during the March quarter, outpacing the

+612 9276 4583

gareth.james@morningstar.com

10.3% return of the S&P/ASX 200 Accumulation Index. Long-term portfolio returns remain very strong, with a

16.4% annualised return during the past five years versus just 8.6% for the benchmark. Portfolio returns are

Peter Warnes

even greater when franking credits are included, however, we exclude them from our return calculation as

Head of Australian Equity Research

the benefits vary depending on an individual's tax status.

+612 9904 5331

peter.warnes@morningstar.com

Yield compression and commodity price weakness remained key drivers of the Australian stock market in the

March quarter. The 26% fall in the iron ore price pushed smaller miners towards the brink with knock-on

effects for mining service providers. The 14% fall in the oil price piled even more pressure on oil and gas

Morningstar Style Box

29.4

8.5

6.3

0.0

0.0

Value

Blend

%

Equity Style Value

40.2

Equity Style Core

30.3

Equity Style Growth

29.4

Small

0.0

Mid

24.0

Large

31.7

Equity Style

0.0

producers and Shell"s acquisition of BG Group could be the first of many in the sector. Despite commodity

price weakness, the S&P/ASX 200 Accumulation Index still rose strongly during the quarter with the yield

compression effect exceeding commodity price weakness. The ending of the resources boom has reduced

resources stocks to 19% of the index, whereas interest-rate-sensitive stocks in the financials, real estate,

utilities, and telecommunications sectors now comprise 56% of the index.

The Income portfolio generally avoids resources companies given the volatile nature of their profits, meaning

Growth

commodity price weakness has been a tailwind for portfolio outperformance. Looking forward, we don"t

expect commodity price falls to continue at the same rate and outperformance by typical income stocks is

likely to become harder to achieve. Reflecting this view, we recently increased our exposure to BHP Billiton,

believing the yield to be attractive and sustainable.

Commodity price weakness continues to weigh on the economy with unemployment at a 12-year high and

iron ore price weakness creating a hole in the federal budget. The Reserve Bank of Australia's, or RBA's,

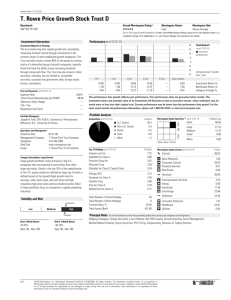

Income Portfolio - Top 10 Holdings

decision to cut the cash rate by 25 basis points to 2.25% in February helped yields compress further and

Weighting %

ASX-listed interest rate futures imply a further two 25 basis-point cuts by year end. Booming residential real

14.7

estate prices represent a challenge to further RBA cuts, though without further cuts, the property market is

Telstra Corp Ltd

Australia and New Zealand Banking Group Ltd

8.2

likely to consolidate. Despite interest rate cuts and yield compression, negative interest rates in Europe and

Westpac Banking Corp

8.1

APA Group

7.3

a 7% fall in the Australian dollar/U.S. dollar exchange rate during the quarter means Australia remains an

National Australia Bank Ltd

7.1

Commonwealth Bank of Australia

7.0

BWP Trust

6.1

Despite strong returns during the past year, portfolio metrics remain attractive with a weighted-average

BHP Billiton Ltd

6.0

yield of 4.7%, or 6.0% grossed up. It remains heavily skewed towards high-quality companies with 96% of

Wesfarmers Ltd

5.5

Scentre Group

4.6

the portfolio in stocks with either a narrow or wide economic moat, and all holdings have either low or

attractive home for foreign capital. With bank deposit rates below 3% and portfolio holdings yielding 5%, or

more than 6% with franking credits, yield compression can continue.

medium fair value uncertainty ratings

Investment Growth of $10,000

Time Period: 1/08/2001 to 31/03/2015

55,000.0

47,500.0

40,000.0

32,500.0

25,000.0

17,500.0

10,000.0

2,500.0

Income Portfolio

2003

2005

2007

2009

2011

2013

2015

S&P/ASX 200 TR

THIS REPORT HAS BEEN PRODUCED USING PRESENTATION STUDIO, A MODULE OF MORNINGSTAR DIRECT

Any Morningstar ratings/recommendations contained in this report are based on the full research report available from Morningstar or your adviser. © 2015 Morningstar, Inc. All rights reserved. Neither Morningstar, its affiliates, nor the content providers guarantee the data or content contained herein to be accurate, complete or

timely nor will they have any liability for its use or distribution. Any general advice or ‘class service’ have been prepared by Morningstar Australasia Pty Ltd (ABN: 95 090 665 544, AFSL: 240892) and/or Morningstar Research Ltd, subsidiaries of Morningstar, Inc, without reference to your objectives, financial situation or needs.

Refer to our Financial Services Guide (FSG) for more information at www.morningstar.com.au/s/fsg.pdf. You should consider the advice in light of these matters and if applicable, the relevant Product Disclosure Statement (Australian products) or Investment Statement (New Zealand products) before making any decision to invest.

Our publications, ratings and products should be viewed as an additional investment resource, not as your sole source of information. Past performance does not necessarily indicate a financial product’s future performance. To obtain advice tailored to your situation, contact a professional financial adviser. Some material is

copyright and published under licence from ASX Operations Pty Ltd ACN 004 523 782 ("ASXO").

Morningstar Income Equities Portfolio Australia & New Zealand

Quarterly Update March 2015

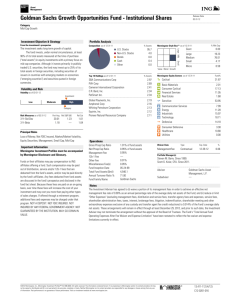

Income Portfolio - Complete List of Holdings

Portfolio Date: 31/03/2015

Code

Price

AUD

PE

Hold

6.00

6.31

17.5

5.1

100

77.1

14.7

Yield Franked

%

%

Telstra Corp Ltd

TLS

É

Narrow

Australia and New Zealand Banking Group Ltd

ANZ

Ç

Wide

Medium Accumulate

42.00

36.64

12.8

5.4

100

101.3

8.2

Westpac Banking Corp

WBC

Ç

Wide

Medium

Hold

41.00

39.38

14.2

5.2

100

122.9

8.1

APA Group

APA

É

Narrow

Medium

Reduce

8.00

9.05

30.8

4.5

19

10.1

7.3

National Australia Bank Ltd

NAB

Ç

Wide

Medium

Hold

43.00

38.55

13.0

5.8

100

93.3

7.1

Commonwealth Bank of Australia

CBA

È

Wide

Medium

Hold

97.00

93.40

15.3

4.9

100

151.4

7.0

BWP Trust

BWP

Ë

Narrow

Medium

Reduce

2.70

3.00

18.4

5.4

0

1.9

6.1

BHP Billiton Ltd

BHP

È

Narrow

Medium Accumulate

40.00

31.03

17.8

5.2

100

99.7

6.0

Wesfarmers Ltd

WES

È

Wide

Medium

44.00

43.96

19.4

5.2

100

49.4

5.5

Scentre Group

SCG

È

Narrow

Medium

Hold

3.80

3.74

16.0

5.7

0

19.9

4.6

Spark New Zealand Ltd

SPK

Ê

Narrow

Medium

Hold

3.00

2.93

16.5

5.6

0

5.4

4.5

WOW

Ç

Wide

Low Accumulate

36.00

29.49

14.2

5.1

100

37.3

4.4

Charter Hall Retail REIT

CQR

Ê

None

Medium

Hold

4.20

4.29

13.9

6.5

0

1.6

3.7

Sonic Healthcare Ltd

SHL

É

Narrow

Medium

Hold

20.00

20.44

17.8

3.9

55

8.2

3.6

AMP Ltd

AMP

É

Narrow

Medium

Hold

7.00

6.44

15.7

5.0

75

19.0

2.8

AGL Energy Ltd

AGL

Ç

Narrow

Medium

Hold

15.00

15.20

15.4

4.4

100

10.3

2.7

Woolworths Ltd

Medium

MktCap Portfolio

AUD Weight

bn

%

Fair

Value

AUD

Style Economic

Uncertainty Recommend

Box

Moat

Hold

3.5

CASH

Note dividends for Spark New Zealand are imputed for New Zealand residents. Australian residents receive unfranked dividends with a supplementary payment.

Morningstar Investment Committee members own the following securities held by the portfolio: BHP, NAB, TLS, WES

Holdings-Based Style Map

Holdings-Based Style Trail

Deep-Val

Core-Val

Core

Core-Grth

Micro

Micro

Small

Small

Mid

Mid

Large

Large

Giant

Giant

Time Period: 30/04/2012 to 31/03/2015

High-Grth

Deep-Val

Income Portfolio

31/03/2015

S&P/ASX 200 TR

31/03/2015

Income Portfolio

Core-Val

Core

30/04/2012 31/03/2015

Core-Grth

High-Grth

S&P/ASX 200 TR

30/04/2012 31/03/2015

The above chart shows the portfolio and index style mix. The shaded area is the region in which

The above chart shows the portfolio and index style mix over time, the smallest dot representing the earliest

75% of the portfolio's holdings fall.

date.

THIS REPORT HAS BEEN PRODUCED USING PRESENTATION STUDIO, A MODULE OF MORNINGSTAR DIRECT

Any Morningstar ratings/recommendations contained in this report are based on the full research report available from Morningstar or your adviser. © 2015 Morningstar, Inc. All rights reserved. Neither Morningstar, its affiliates, nor the content providers guarantee the data or content contained herein to be accurate, complete or

timely nor will they have any liability for its use or distribution. Any general advice or ‘class service’ have been prepared by Morningstar Australasia Pty Ltd (ABN: 95 090 665 544, AFSL: 240892) and/or Morningstar Research Ltd, subsidiaries of Morningstar, Inc, without reference to your objectives, financial situation or needs.

Refer to our Financial Services Guide (FSG) for more information at www.morningstar.com.au/s/fsg.pdf. You should consider the advice in light of these matters and if applicable, the relevant Product Disclosure Statement (Australian products) or Investment Statement (New Zealand products) before making any decision to invest.

Our publications, ratings and products should be viewed as an additional investment resource, not as your sole source of information. Past performance does not necessarily indicate a financial product’s future performance. To obtain advice tailored to your situation, contact a professional financial adviser. Some material is

copyright and published under licence from ASX Operations Pty Ltd ACN 004 523 782 ("ASXO").

Morningstar Income Equities Portfolio Australia & New Zealand

Quarterly Update March 2015

Transactions in the Quarter

Portfolio Fundamentals

Display Benchmark 1: S&P/ASX 200 TR

Inv

Moat Company Pct

96.1

Portfolio Price/Fair Value

0.97

Turnover (2 Yr Avg)

17.3

Forecast Yield Pct

5.01

Forecast Yield Pct (Grossed Up)

Average Market Cap (mil)

Bmk1

Cat Avg

We increased our holding in BHP Billiton in March from 3.5% to 6.5%, funded by a reduction in our APA

Group holding from 11.5% to 7.4%. APA Group was trading at a 17% premium to fair value whereas BHP

Billiton was at a 14% discount, meaning the transaction reduced the portfolio's weighted-average price-tofair-value ratio from 1.05 to 1.03. The proportion of holdings with moats and low or medium uncertainty

ratings was unchanged. The net dividend yield was also unchanged, however, the portfolio's weightedaverage grossed-up yield increased from 5.79% to 5.85%.

6.53

25,828.4

28,799.5

26,646.2

P/E Ratio (TTM)

15.0

16.7

17.1

Debt to Capital % (TTM)

38.9

39.1

39.0

ROA % (TTM)

7.4

5.2

5.3

ROE % (TTM)

21.6

16.1

16.2

BHP Billiton is a high-quality business with a narrow economic moat and medium uncertainty ratings, and

the stock is in our Best Stock Ideas. Other cheaper alternatives lacked either the quality or dividend

sustainability required for the Income portfolio. As one of the largest stocks on the market, BHP Billiton offers

exposure to a high-quality, diversified portfolio of low-cost and long-life resources assets. The diversified

nature of BHP Billiton's portfolio should smooth out the earnings volatility normally experienced by mining

companies. BHP Billiton is also one of the lowest-cost producers of iron ore in the world, meaning it should

be able to withstand weak iron ore prices as other miners cease production and the market tightens. The

Asset Allocation

company has a long history of paying and growing fully franked dividends and has committed to continue to

Portfolio Date: 31/03/2015

%

do so in future. BHP Billiton's dividends have grown every year since 2002.

Stock

96.5

The purchase means our underweight exposure to the materials and energy sectors reduced from 11% to

Bond

0.0

8% below market weight. We continue to rate APA Group highly and the company retains its narrow

Cash

3.5

economic moat and Exemplary stewardship ratings. However, the current demand for yield investments has

Other

0.0

pushed the shares above our fair value estimate to the point where the expected returns are low and the

Total

100.0

shares are overvalued.

Equity Country Exposure

Portfolio Date: 31/03/2015

%

Australia

New Zealand

Total

95.3

4.7

100.0

Equity Sectors (GICS)

Portfolio Date: 31/03/2015

%

Materials

Consumer Staples

6.3

10.3

Healthcare

3.8

Financials

49.4

Telecom Services

19.9

Utilities

Total

10.4

100.0

THIS REPORT HAS BEEN PRODUCED USING PRESENTATION STUDIO, A MODULE OF MORNINGSTAR DIRECT

Any Morningstar ratings/recommendations contained in this report are based on the full research report available from Morningstar or your adviser. © 2015 Morningstar, Inc. All rights reserved. Neither Morningstar, its affiliates, nor the content providers guarantee the data or content contained herein to be accurate, complete or

timely nor will they have any liability for its use or distribution. Any general advice or ‘class service’ have been prepared by Morningstar Australasia Pty Ltd (ABN: 95 090 665 544, AFSL: 240892) and/or Morningstar Research Ltd, subsidiaries of Morningstar, Inc, without reference to your objectives, financial situation or needs.

Refer to our Financial Services Guide (FSG) for more information at www.morningstar.com.au/s/fsg.pdf. You should consider the advice in light of these matters and if applicable, the relevant Product Disclosure Statement (Australian products) or Investment Statement (New Zealand products) before making any decision to invest.

Our publications, ratings and products should be viewed as an additional investment resource, not as your sole source of information. Past performance does not necessarily indicate a financial product’s future performance. To obtain advice tailored to your situation, contact a professional financial adviser. Some material is

copyright and published under licence from ASX Operations Pty Ltd ACN 004 523 782 ("ASXO").

Morningstar Income Equities Portfolio Australia & New Zealand

Quarterly Update March 2015

Performance Relative to Peer Group (one month lag)

Quarter Performance

Peer Group (5-95%): All Managed Investments - Australia - Equity Australia Large Blend

The 11.0% return achieved by the Morningstar Income Equities Portfolio in the March quarter was

Return

Top Quartile

24.0

22.0

20.0

18.0

16.0

14.0

12.0

10.0

8.0

6.0

2nd Quartile

3rd Quartile

Bottom Quartile

particularly strong, and well above long term equity market returns. The pleasing 0.7% outperformance of

the benchmark S&P/ASX 200 Accumulation Index was driven by our underweight position in resources

stocks which suffered from commodity price weakness. Longer-term performance is impressive at 22%

compounded for three years, versus the benchmark return of 16%. The concentrated nature of the portfolio

means holdings are often overweight the benchmark and good stock selection translates into index

outperformance.

Contributors

Portfolio outperformance was, once again, driven by commodity price weakness and yield compression. Our

YTD

1 year

Income Portfolio

3 years

5 years

Since

inception

lack of exposure to oil stocks including Santos, Origin Energy, Oil Search, and Woodside Petroleum were all

key contributors to outperformance, as the oil price fell a further 14%. A lack of exposure to Fortescue

Metals Group and Rio Tinto, were also key contributors as the iron ore price fell a further 26%. Longer term,

S&P/ASX 200 TR

we expect the iron ore price to remain low, whereas we expect oil price weakness will be cyclical. However,

most oil stocks are not of sufficient quality for inclusion in the Income portfolio as many lack competitive

Risk-Reward

advantage, bring commodity price risk and do not provide the stable, and preferably growing, income we

Time Period: 1/08/2001 to 31/03/2015

seek.

18.0

Income Portfolio

15.0

S&P/ASX 200 TR

Portfolio holdings that helped outperformance included our overweight positions in APA Group, AMP and

AGL Energy. All three stocks benefitted from good financial results during the February reporting season as

12.0

well as yield compression among blue-chip stocks.

9.0

Detractors

Return

6.0

3.0

Woolworths was the only portfolio holding with a negative return during the quarter, despite announcing

0.0

record profit margins within its Australian food and liquor business with its interim result in February. The

0.0

3.0

6.0

market remains concerned discount supermarkets Aldi and Costco will cause price deflation and operating

9.0 12.0 15.0

deleverage for Woolworths, thereby causing profit margins to compress. We also forecast profit margin

Std Dev

compression, but consider Woolworths to have sufficient headroom to remain an attractive investment.

Spark New Zealand was the largest detractor from outperformance despite generating a positive return of

1.5% as the portfolio's weight is much larger than the index weight. The company reported a disappointing

Income Portfolio - Market Performance

interim result in February with competition making revenue growth challenging. Other detractors from

Time Period: 1/08/2001 to 31/03/2015

Inv

Bmk1

Up Period Percent

68.90

64.02

Down Period Percent

31.10

35.98

Best Month

Worst Month

8.53

7.98

-11.46

-12.61

Best Quarter

17.31

21.50

Worst Quarter

-15.64

-18.25

Up Capture Ratio

82.84

100.00

Down Capture Ratio

46.96

100.00

Inv

Bmk1

outperformance largely comprised stocks we didn't own that performed well, including Macquarie Group,

Toll Holdings, and ResMed Inc. These stocks were excluded from the portfolio either because of a lack of

economic moat or a relatively low dividend yield.

Risk

Time Period: 1/08/2001 to 31/03/2015

Return % pa

13.23

8.89

Std Dev

11.60

12.97

Downside Deviation

5.78

0.00

Alpha

5.22

0.00

Beta

0.68

1.00

57.35

100.00

Sharpe Ratio (arith)

0.71

0.30

Tracking Error

8.67

0.00

R2

THIS REPORT HAS BEEN PRODUCED USING PRESENTATION STUDIO, A MODULE OF MORNINGSTAR DIRECT

Any Morningstar ratings/recommendations contained in this report are based on the full research report available from Morningstar or your adviser. © 2015 Morningstar, Inc. All rights reserved. Neither Morningstar, its affiliates, nor the content providers guarantee the data or content contained herein to be accurate, complete or

timely nor will they have any liability for its use or distribution. Any general advice or ‘class service’ have been prepared by Morningstar Australasia Pty Ltd (ABN: 95 090 665 544, AFSL: 240892) and/or Morningstar Research Ltd, subsidiaries of Morningstar, Inc, without reference to your objectives, financial situation or needs.

Refer to our Financial Services Guide (FSG) for more information at www.morningstar.com.au/s/fsg.pdf. You should consider the advice in light of these matters and if applicable, the relevant Product Disclosure Statement (Australian products) or Investment Statement (New Zealand products) before making any decision to invest.

Our publications, ratings and products should be viewed as an additional investment resource, not as your sole source of information. Past performance does not necessarily indicate a financial product’s future performance. To obtain advice tailored to your situation, contact a professional financial adviser. Some material is

copyright and published under licence from ASX Operations Pty Ltd ACN 004 523 782 ("ASXO").

Morningstar Income Equities Portfolio Australia & New Zealand

Quarterly Update March 2015

Sector and Industry Weightings Analysis

GICS Sector Weights Relative to Benchmark

49.4

48.6

Financials

19.9

Telecom Services

5.7

characteristics that align well with the portfolio's objectives. Sector exposures reflect both our

1.9

Consumer Staples

10.3

6.8

Materials

6.3

macroeconomic thesis and preference for high-quality and sustainable earnings. Earnings growth is likely to

be lower than for companies in the Morningstar Growth Equities Portfolio, and more capital-intensive sectors

such as materials and upstream energy will tend not to feature as they typically do not provide the

14.5

sustainable yield required.

3.8

6.0

Healthcare

Industrials

0.0

Energy

0.0

Consumer

Discretionary

0.0

Technology

0.0

0.7

The financial sector is our largest exposure, at about half of the portfolio, comprising 30% banks, 14% real

estate and 3% diversified financials. The wide moat-rated "big four" banks are a good fit for the portfolio with

7.2

medium fair value uncertainty ratings and highly regarded management teams. All, except National Australia

4.4

Bank have Exemplary stewardship ratings. Grossed-up yields of near 7% are among the highest for moatrated stocks in the S&P/ASX 200 Index. The average price-to-fair-value ratio of 0.93 for the big four banks

4.1

0.0

10.0

though we increased our BHP Billiton holding, and resources exposure, to 6.5% of the portfolio in March.

Banks, real estate, telecommunications and utilities represent 77% of the portfolio given their defensive

10.4

Utilities

The Morningstar Income Equities Portfolio sector exposure remained little changed during the March quarter,

also appeals, both in an absolute sense and relative to the index at 0.97.

20.0

30.0

40.0

50.0

60.0

The telecommunications services sector remains the portfolio's second-largest sector weighting, at 19%,

and the largest overweight position versus the benchmark's 6% weighting. Sector exposure comprises a

Income Portfolio

15% weight to Telstra Corporation and 5% weight to Spark New Zealand, formerly Telecom Corporation of

S&P/ASX 200 TR

New Zealand. Telstra has a net yield near 5%, grossed up to 7%, while Spark New Zealand offers a yield of

5.6% including supplementary dividends. They both have narrow economic moats stemming from low-cost

GICS Industry Group Weights Relative to Benchmark

advantages and long-established dominant positions in their domestic markets, enabling attractive and

sustainable earnings and dividends. These attributes make them valuable portfolio holdings.

13.6

Telecommunication Services

Real estate is the third-largest sector exposure, with a 14% weighting versus a 7% benchmark weight. Real

7.9

Utilities

estate appeals to the Income portfolio given the relatively stable earnings streams and above-average yields.

7.0

Real Estate

We prefer REITs with long-term leases and high-quality tenants, fixed or inflation-linked rent increases and

4.0

Food and Staples Retailing

low vacancy risk relative to the more volatile and less predictable developers. The portfolio owns BWP Trust

and Scentre Group, which fit that bill. BWP Trust's earnings are secured by long-term leases to hardware

0.8

Health Care Equipment and Services

powerhouse Bunnings. Scentre Group offers exposure to high-quality shopping malls which enjoy dominant

Consumer Durables and Apparel

0.0

Household and Personal Products

-0.1

Automobiles and Components

-0.1

Capital Goods

-0.4

Software and Services

-0.7

Media

-0.7

The portfolio has only a 6% exposure to materials via diversified, high-quality and low-cost miner BHP Billiton,

Retailing

-0.7

and very little exposure to upstream energy. The materials and energy sectors comprise 14% and 4% of the

Food, Beverage and Tobacco

-0.8

benchmark respectively so we're significantly underweight both. Resources producers are generally unsuited

Banks

-2.0

Insurance

-2.0

Consumer Services

-2.5

Commercial Services and Supplies

-2.7

Pharmaceuticals and Biotechnology

-3.1

Diversified Financials

-3.5

Transportation

-4.3

Energy

-4.4

Materials

positions in premium locations in Australia and New Zealand.

Our second-largest overweight position is to the utilities sector, comprising 10% of the portfolio against a

benchmark weight of just 1%. Utilities stocks are a core holding for many income portfolios and typically

provide highly defensive earnings, high payout ratios and strong and stable dividends.

to the portfolio given their capital intensity and exposure to cyclical commodity prices, attributes which

generally don't support stable yields. Our natural aversion to resources for this strategy means the portfolio is

likely to outperform in resources bear markets.

-8.5

-20.0 -10.0

0.0

10.0

20.0

THIS REPORT HAS BEEN PRODUCED USING PRESENTATION STUDIO, A MODULE OF MORNINGSTAR DIRECT

Any Morningstar ratings/recommendations contained in this report are based on the full research report available from Morningstar or your adviser. © 2015 Morningstar, Inc. All rights reserved. Neither Morningstar, its affiliates, nor the content providers guarantee the data or content contained herein to be accurate, complete or

timely nor will they have any liability for its use or distribution. Any general advice or ‘class service’ have been prepared by Morningstar Australasia Pty Ltd (ABN: 95 090 665 544, AFSL: 240892) and/or Morningstar Research Ltd, subsidiaries of Morningstar, Inc, without reference to your objectives, financial situation or needs.

Refer to our Financial Services Guide (FSG) for more information at www.morningstar.com.au/s/fsg.pdf. You should consider the advice in light of these matters and if applicable, the relevant Product Disclosure Statement (Australian products) or Investment Statement (New Zealand products) before making any decision to invest.

Our publications, ratings and products should be viewed as an additional investment resource, not as your sole source of information. Past performance does not necessarily indicate a financial product’s future performance. To obtain advice tailored to your situation, contact a professional financial adviser. Some material is

copyright and published under licence from ASX Operations Pty Ltd ACN 004 523 782 ("ASXO").

Morningstar Income Equities Portfolio Australia & New Zealand

Quarterly Update March 2015

Returns Relative to Benchmark

Return

As of Date: 31/03/2015

25.0

22.5

20.0

17.5

15.0

12.5

10.0

7.5

5.0

2.5

0.0

22.6

22.2

11.0

11.0

10.3

3 month

16.4

15.8

14.1

13.2

10.3

8.9

8.6

YTD

1 year

3 years

Income Portfolio

5 years

Since inception* (31/07/2001)

S&P/ASX 200 TR

Performance measures are expressed before fees, costs and taxes are deducted. Dividends are reinvested in the portfolio. The performance displayed is for the Morningstar Income Equities Portfolio and represents modelled performance only. This performance will differ

from actual performance depending on factors such as transaction timing and any divergence from constituent weightings.

* Where inception date is not the beginning of a month, returns are calculated using a start date which is the first day of the month following inception.

Selection Effects

Time Period: 1/01/2015 to 31/03/2015

Outperform

12.00

6

6.00

1

5

14

7 15

9

2

114 12

3

8

5

8

14

12

11

10

2

9

13

15

7

10

-6.00

Underweight

13

6

1

4

3

0.00

Overweight

Relative Weight

Underperform

-12.00

-45.00

-36.00

-27.00

-18.00

-9.00

0.00

9.00

18.00

27.00

36.00

45.00

Relative Return

Best Selections

Investment Type

Weight +/-

Return +/-

1

APA Group

Stock

9.08

10.66

2

Woodside Petroleum Ltd

Stock

-1.81

-13.14

3

Rio Tinto Ltd

Stock

-1.86

-8.69

Effect

Worst Selections

Investment Type

1.14

1

Weight +/-

Return +/-

Effect

Spark New Zealand Ltd

Stock

5.10

-9.86

-0.51

0.26

2

Macquarie Group Ltd.

Stock

-1.47

20.72

-0.29

0.16

3

Woolworths Ltd

Stock

2.15

-12.45

-0.27

4

Suncorp Group Ltd

Stock

-1.30

-11.08

0.15

4

Charter Hall Retail REIT

Stock

3.97

-6.69

-0.27

5

AMP Ltd

Stock

1.49

9.58

0.14

5

BWP Trust

Stock

6.15

-3.29

-0.20

6

Fortescue Metals Group Ltd Stock

-0.31

-38.03

0.13

6

Telstra Corp Ltd

Stock

10.24

-1.61

-0.15

7

Santos Ltd

Stock

-0.56

-21.92

0.13

7

Toll Holdings Ltd

Stock

-0.34

42.78

-0.13

8

AGL Energy Ltd

Stock

2.06

6.14

0.12

8

QBE Insurance Group Ltd

Stock

-1.13

8.32

-0.10

9

Oil Search Limited

Stock

-0.66

-17.73

0.12

9

ResMed Inc DR

Stock

-0.42

23.19

-0.09

10 CSL Ltd

Stock

-2.99

-3.68

0.11

10 Qantas Airways Ltd

Stock

-0.41

19.19

-0.08

11 Origin Energy Ltd

Stock

-0.90

-11.86

0.11

11 Newcrest Mining Ltd

Stock

-0.69

11.96

-0.07

12 Insurance Australia Group Ltd Stock

-1.03

-10.14

0.11

12 Incitec Pivot Ltd

Stock

-0.41

16.77

-0.06

13 BlueScope Steel Ltd

Stock

-0.20

-35.63

0.08

13 Iluka Resources Ltd

Stock

-0.21

34.34

-0.06

14 Amcor Ltd

Stock

-1.15

-5.62

0.07

14 Wesfarmers Ltd

Stock

2.37

-2.50

-0.06

15 Alumina Ltd

Stock

-0.33

-19.98

0.07

15 Henderson Group PLC DR

Stock

-0.23

25.39

-0.05

THIS REPORT HAS BEEN PRODUCED USING PRESENTATION STUDIO, A MODULE OF MORNINGSTAR DIRECT

Any Morningstar ratings/recommendations contained in this report are based on the full research report available from Morningstar or your adviser. © 2015 Morningstar, Inc. All rights reserved. Neither Morningstar, its affiliates, nor the content providers guarantee the data or content contained herein to be accurate, complete or

timely nor will they have any liability for its use or distribution. Any general advice or ‘class service’ have been prepared by Morningstar Australasia Pty Ltd (ABN: 95 090 665 544, AFSL: 240892) and/or Morningstar Research Ltd, subsidiaries of Morningstar, Inc, without reference to your objectives, financial situation or needs.

Refer to our Financial Services Guide (FSG) for more information at www.morningstar.com.au/s/fsg.pdf. You should consider the advice in light of these matters and if applicable, the relevant Product Disclosure Statement (Australian products) or Investment Statement (New Zealand products) before making any decision to invest.

Our publications, ratings and products should be viewed as an additional investment resource, not as your sole source of information. Past performance does not necessarily indicate a financial product’s future performance. To obtain advice tailored to your situation, contact a professional financial adviser. Some material is

copyright and published under licence from ASX Operations Pty Ltd ACN 004 523 782 ("ASXO").

Morningstar Income Equities Portfolio Australia & New Zealand

Quarterly Update March 2015

Allocation Effects

Time Period: 1/01/2015 to 31/03/2015

Outperform

Overweight

Relative Weight

Underperform

12.00

2

5

6.00

2

4

4

3

1

3

1

Underweight

0.00

-6.00

5

-12.00

-15.00

1

2

3

4

5

-12.00

-9.00

Best Weighting

Energy

Utilities

Pharmaceuticals and Biotechnology

Commercial Services and Supplies

Materials

Weight +/-4.86

10.53

-3.17

-2.67

-10.59

-6.00

Return +/-13.58

3.17

-5.36

-6.03

-2.38

-3.00

0.00

Effect

0.69

0.38

0.17

0.17

0.14

1

2

3

4

5

3.00

Worst Weighting

Diversified Financials

Food and Staples Retailing

Transportation

Consumer Services

Real Estate

6.00

9.00

Weight +/-3.24

4.42

-4.12

-2.40

7.51

12.00

15.00

Relative Return

Return +/13.34

-7.40

3.58

5.76

-1.84

Effect

-0.42

-0.33

-0.15

-0.13

-0.12

Cumulative Attribution Effects

Time Period: 1/04/2014 to 31/03/2015

GICS Industry GroupCumulative Attribution Effects

Attribution Effect %

Cumulative Allocation Effect

12.00

Cumulative Selection Effect

Cumulative Active Return

9.00

6.00

3.00

0.00

-3.00

-6.00

4.00

Attribution Effects

Allocation Effect

Selection Effect

Active Return

2.00

0.00

-2.00

4-30-2014 5-31-2014 6-30-2014 7-31-2014 8-31-2014 9-30-2014 10-31-2014 11-30-2014 12-31-2014 1-31-2015 2-28-2015 3-31-2015

THIS REPORT HAS BEEN PRODUCED USING PRESENTATION STUDIO, A MODULE OF MORNINGSTAR DIRECT

Any Morningstar ratings/recommendations contained in this report are based on the full research report available from Morningstar or your adviser. © 2015 Morningstar, Inc. All rights reserved. Neither Morningstar, its affiliates, nor the content providers guarantee the data or content contained herein to be accurate, complete or

timely nor will they have any liability for its use or distribution. Any general advice or ‘class service’ have been prepared by Morningstar Australasia Pty Ltd (ABN: 95 090 665 544, AFSL: 240892) and/or Morningstar Research Ltd, subsidiaries of Morningstar, Inc, without reference to your objectives, financial situation or needs.

Refer to our Financial Services Guide (FSG) for more information at www.morningstar.com.au/s/fsg.pdf. You should consider the advice in light of these matters and if applicable, the relevant Product Disclosure Statement (Australian products) or Investment Statement (New Zealand products) before making any decision to invest.

Our publications, ratings and products should be viewed as an additional investment resource, not as your sole source of information. Past performance does not necessarily indicate a financial product’s future performance. To obtain advice tailored to your situation, contact a professional financial adviser. Some material is

copyright and published under licence from ASX Operations Pty Ltd ACN 004 523 782 ("ASXO").

Morningstar Income Equities Portfolio Australia & New Zealand

Quarterly Update March 2015

Equity Sectors (GICS)

Time Period: 1/04/2012 to 31/03/2015

100.0

90.0

80.0

70.0

60.0

50.0

40.0

30.0

20.0

10.0

0.0

09/2012

03/2013

Energy %

Consumer Discretionary %

Financials %

Utilities %

09/2013

03/2014

Materials %

Consumer Staples %

Information Technology %

09/2014

03/2015

Industrials %

Healthcare %

Telecom Services %

Equity Style Valuation

Time Period: 1/04/2012 to 31/03/2015

100.0

90.0

80.0

70.0

60.0

50.0

40.0

30.0

20.0

10.0

0.0

09/2012

03/2013

Value %

09/2013

03/2014

Core %

09/2014

03/2015

09/2014

03/2015

Growth %

Equity Market Capitalization

Time Period: 1/04/2012 to 31/03/2015

100.0

90.0

80.0

70.0

60.0

50.0

40.0

30.0

20.0

10.0

0.0

09/2012

Giant %

Small %

03/2013

09/2013

Large %

Micro %

03/2014

Mid %

THIS REPORT HAS BEEN PRODUCED USING PRESENTATION STUDIO, A MODULE OF MORNINGSTAR DIRECT

Any Morningstar ratings/recommendations contained in this report are based on the full research report available from Morningstar or your adviser. © 2015 Morningstar, Inc. All rights reserved. Neither Morningstar, its affiliates, nor the content providers guarantee the data or content contained herein to be accurate, complete or

timely nor will they have any liability for its use or distribution. Any general advice or ‘class service’ have been prepared by Morningstar Australasia Pty Ltd (ABN: 95 090 665 544, AFSL: 240892) and/or Morningstar Research Ltd, subsidiaries of Morningstar, Inc, without reference to your objectives, financial situation or needs.

Refer to our Financial Services Guide (FSG) for more information at www.morningstar.com.au/s/fsg.pdf. You should consider the advice in light of these matters and if applicable, the relevant Product Disclosure Statement (Australian products) or Investment Statement (New Zealand products) before making any decision to invest.

Our publications, ratings and products should be viewed as an additional investment resource, not as your sole source of information. Past performance does not necessarily indicate a financial product’s future performance. To obtain advice tailored to your situation, contact a professional financial adviser. Some material is

copyright and published under licence from ASX Operations Pty Ltd ACN 004 523 782 ("ASXO").

Morningstar Income Equities Portfolio Australia & New Zealand

Investment Methodology and Process

Quarterly Update March 2015

Portfolio Mandate and Typical Positioning

Income Portfolio Strategy

The Morningstar Income Equities Portfolio Australia & New Zealand is an actively managed concentrated portfolio

consisting of our best income ideas in the S&P/ASX 200 Index. The portfolio is constructed with a focus on long-term

fundamental value and bias toward businesses with sustainable competitive advantages (economic moats) and

predictable cash flows.

Total return from the Income Portfolio will tend to be driven more by income than capital appreciation, although both

are desirable. Income holdings have expected sustainable net yields greater than or equal to the benchmark using the

estimates of our research team. In addition, coverage companies with above average dividend per share growth

prospects over the next five years receive preference, all else equal. We may occasionally initiate a position with less

than benchmark net dividend yield if the gross yield is greater than the benchmark’s net yield, dividend per share

growth prospects are well-above average, or to increase the portfolio's share of high quality (narrow or wide economic

moat) companies. Dividend sustainability is a key consideration and is partially accounted for by not allowing Very High

or Extreme uncertainty ratings into the Income Portfolio, as this reduces exposure to difficult to predict cash flows.

Moreover, high uncertainty stocks are infrequently purchased. Sustainability is further tested by ensuring potential and

current holdings can meet the above criteria with long-term normalised payout ratios. Preference is given to

companies that can sustain unexpected shocks and still provide attractive yields.

Investment Strategy Committee Process

Morningstar’s equity portfolios are managed by their portfolio managers and our eight-person investment strategy

committee which comprises selected members of the equities research team. Committee meetings reinforce rigor and

consistency of research methodology through collaborative debate on proposed and existing holdings. A constant

feedback loop between Morningstar’s research team and investment committee members leverages team strengths

in vetting stock calls and portfolio holdings. This constant cycle strengthens team culture, expertise and ratings,

minimising key-person risk and common behavioural pitfalls.

The committee is experienced and well-resourced, ensuring stability and succession planning. Representation from

each sector team ensures cross-market expertise. Committee members have average industry experience of 17 years

and average tenure with Morningstar of 10 years. We are not averse to an occasional portfolio manager change, as

the driving forces behind our portfolio construction process are our bottom-up research and investment committee

overlay.

In-depth research by our large, global, and experienced analyst team is the bedrock of our portfolio management

process and facilitates our high conviction investments. We have more than 100 equity and credit analysts globally,

covering around 1,700 stocks and 700 debt issuers, making us one of the largest independent research teams in the

world. Our 20 Australian and New Zealand-based analysts cover about 230 Australian and New Zealand stocks which

includes extensive research reports, timely event analysis, actionable special reports, and deep discounted cash flow

modelling on every company. This is complimented by our local credit research to help us assess the complete capital

structure and preserve capital while pursing upside opportunities.

Investment Committee Feedback Loop

THIS REPORT HAS BEEN PRODUCED USING PRESENTATION STUDIO, A MODULE OF MORNINGSTAR DIRECT

Any Morningstar ratings/recommendations contained in this report are based on the full research report available from Morningstar or your adviser. © 2015 Morningstar, Inc. All rights reserved. Neither Morningstar, its affiliates, nor the content providers guarantee the data or content contained herein to be accurate, complete or

timely nor will they have any liability for its use or distribution. Any general advice or ‘class service’ have been prepared by Morningstar Australasia Pty Ltd (ABN: 95 090 665 544, AFSL: 240892) and/or Morningstar Research Ltd, subsidiaries of Morningstar, Inc, without reference to your objectives, financial situation or needs.

Refer to our Financial Services Guide (FSG) for more information at www.morningstar.com.au/s/fsg.pdf. You should consider the advice in light of these matters and if applicable, the relevant Product Disclosure Statement (Australian products) or Investment Statement (New Zealand products) before making any decision to invest.

Our publications, ratings and products should be viewed as an additional investment resource, not as your sole source of information. Past performance does not necessarily indicate a financial product’s future performance. To obtain advice tailored to your situation, contact a professional financial adviser. Some material is

copyright and published under licence from ASX Operations Pty Ltd ACN 004 523 782 ("ASXO").

Morningstar Income Equities Portfolio Australia & New Zealand

Quarterly Update March 2015

THIS REPORT HAS BEEN PRODUCED USING PRESENTATION STUDIO, A MODULE OF MORNINGSTAR DIRECT

Any Morningstar ratings/recommendations contained in this report are based on the full research report available from Morningstar or your adviser. © 2015 Morningstar, Inc. All rights reserved. Neither Morningstar, its affiliates, nor the content providers guarantee the data or content contained herein to be accurate, complete or

timely nor will they have any liability for its use or distribution. Any general advice or ‘class service’ have been prepared by Morningstar Australasia Pty Ltd (ABN: 95 090 665 544, AFSL: 240892) and/or Morningstar Research Ltd, subsidiaries of Morningstar, Inc, without reference to your objectives, financial situation or needs.

Refer to our Financial Services Guide (FSG) for more information at www.morningstar.com.au/s/fsg.pdf. You should consider the advice in light of these matters and if applicable, the relevant Product Disclosure Statement (Australian products) or Investment Statement (New Zealand products) before making any decision to invest.

Our publications, ratings and products should be viewed as an additional investment resource, not as your sole source of information. Past performance does not necessarily indicate a financial product’s future performance. To obtain advice tailored to your situation, contact a professional financial adviser. Some material is

copyright and published under licence from ASX Operations Pty Ltd ACN 004 523 782 ("ASXO").

Morningstar Income Equities Portfolio Australia & New Zealand

Quarterly Update March 2015

THIS REPORT HAS BEEN PRODUCED USING PRESENTATION STUDIO, A MODULE OF MORNINGSTAR DIRECT

Any Morningstar ratings/recommendations contained in this report are based on the full research report available from Morningstar or your adviser. © 2015 Morningstar, Inc. All rights reserved. Neither Morningstar, its affiliates, nor the content providers guarantee the data or content contained herein to be accurate, complete or

timely nor will they have any liability for its use or distribution. Any general advice or ‘class service’ have been prepared by Morningstar Australasia Pty Ltd (ABN: 95 090 665 544, AFSL: 240892) and/or Morningstar Research Ltd, subsidiaries of Morningstar, Inc, without reference to your objectives, financial situation or needs.

Refer to our Financial Services Guide (FSG) for more information at www.morningstar.com.au/s/fsg.pdf. You should consider the advice in light of these matters and if applicable, the relevant Product Disclosure Statement (Australian products) or Investment Statement (New Zealand products) before making any decision to invest.

Our publications, ratings and products should be viewed as an additional investment resource, not as your sole source of information. Past performance does not necessarily indicate a financial product’s future performance. To obtain advice tailored to your situation, contact a professional financial adviser. Some material is

copyright and published under licence from ASX Operations Pty Ltd ACN 004 523 782 ("ASXO").

Morningstar Income Equities Portfolio Australia & New Zealand

Quarterly Update March 2015

THIS REPORT HAS BEEN PRODUCED USING PRESENTATION STUDIO, A MODULE OF MORNINGSTAR DIRECT

Any Morningstar ratings/recommendations contained in this report are based on the full research report available from Morningstar or your adviser. © 2015 Morningstar, Inc. All rights reserved. Neither Morningstar, its affiliates, nor the content providers guarantee the data or content contained herein to be accurate, complete or

timely nor will they have any liability for its use or distribution. Any general advice or ‘class service’ have been prepared by Morningstar Australasia Pty Ltd (ABN: 95 090 665 544, AFSL: 240892) and/or Morningstar Research Ltd, subsidiaries of Morningstar, Inc, without reference to your objectives, financial situation or needs.

Refer to our Financial Services Guide (FSG) for more information at www.morningstar.com.au/s/fsg.pdf. You should consider the advice in light of these matters and if applicable, the relevant Product Disclosure Statement (Australian products) or Investment Statement (New Zealand products) before making any decision to invest.

Our publications, ratings and products should be viewed as an additional investment resource, not as your sole source of information. Past performance does not necessarily indicate a financial product’s future performance. To obtain advice tailored to your situation, contact a professional financial adviser. Some material is

copyright and published under licence from ASX Operations Pty Ltd ACN 004 523 782 ("ASXO").