Topic 5: Time Value of Money-Series of Payments Present value of a

advertisement

Topic 5: Time Value of Money-Series of

Payments

Learning Objectives Satisfied:

1. Introduction to Financial Management

Also cover the major foundations of Finance such as

3 Time Value of Money

3 Cash Flow and Taxes and their implications for financial managers

2. Financial Markets and Interests Rates

Objectives: Understand the following topics

3 Inflation and interest rates and their relationship

3. Mathematics of Finance

Objectives: Understand the following concepts

3 Present and future value of perpetuities, annuities, annuities due

3 Loan amortization

Present value of a series of cash flows:

PV = C 0 +

C1

+

(1 +R)1

C2

+

...

+

(1 +R)2

Cn

(1 +R)n

Example 1 (for further practice, see Set 2, #1)

PV = 0

+

110

(1.10) 1

+

121

(1.10) 2

+

133.10

(1.10) 3

PV = 100 + 100 + 100 = 300

Internal Rate of Return:

C0 =

Example1

C1

(1 +R)1

+

...

+

(1 +R)2

Cn

(1 +R)n

(for further practice, see Set 2, #4)

110

300 =

C2

+

(1+R) 1

121

+

+

(1+R) 2

133.10

(1+R) 3

R = 10%

Future value of a series of cash flows:

FV = C 0 (1 +R)n + C 1 (1 +R)n-1 + ... + C n (1 +R)

Example 2 (for further practice, see Set 2, #4)

FV = 0 + 110(1.10)2 + 121(1.10)1 + 133.10

FV = 0 + 133.10

+ 133.10

+ 133.10 = $399.30

FV = 300 (1.10)3 = 339.30

n-n

How to incorporate inflation into a series:

Example (cash flows adjusted for inflation):

PV = 0

+ 100

(1.03)

1

+ 100

(1.03)

2

+ 100 3 = 282.86

(1.03)

Example (nominal cash flows):

PV = 0

+ 110

1

(1.133)

+ 121

2

(1.133)

+ 133.103 = 282.86

(1.133)

r = 3%, i = 10%, therefore R = 13.3%

Annuities are a special kind of cash flow series

• All payments are equal

• The payments are equally spaced through time

Time Value of Ordinary Annuities: (Example 4)

R=10%

0

PV

1

2

3

100

100

100

90.91

82.64

75.13

248.69

FV

0

1

2

3

100

100

100

110

121

331

For further practice, see Set 2, #5-11

Time Value of Ordinary Annuities

-n

1 - (1+R)

PV = PMT

R

[

]

n

FV = PMT

[

(1+R) - 1

R

]

More examples: Let payment = $100, n = 5, and R = 10%.

Then PV=$379.08 and FV=$610.51

Perpetuities

• Perpetuities are ordinary annuities in which n

approaches infinity

PV = PMT/R

FV approaches infinity, so is not calculated

Perpetuities

• Perpetuities are ordinary annuities in which n

approaches infinity

PV = PMT/R

FV approaches infinity, so is not calculated

Examples:

PMT =$100, R = 10%; Then PV = $100/.1 =

$1000

Perpetuities

• Perpetuities are ordinary annuities in which n

approaches infinity

PV = PMT/R

FV approaches infinity, so is not calculated

Examples:

PMT =$100, R = 10%; Then PV = $100/.1 =

$1000

PMT =$40, R = 8%; Then PV = $40/.08 = $500

Time Value of Annuities Due: (Example 5)

R=10%

PV

0

1

2

100

100

100

3

90.91

82.64

273.55

FV

0

1

2

100

100

100

3

110

121

133.10

364.10

More examples: Let payment = $100, n = 5, and R = 10%.

Then PV=$416.99 and FV=$671.56

Side-by-Side

R=10%

PV

0

1

2

3

100

100

100

R=10%

90.91

90.91

82.64

82.64

75.13

0

1

100

2

100

3

273.55

248.69

FV

0

100

PV

1

2

3

100

100

100

110

121

FV

0

1

2

100

100

100

3

110

121

133.10

331

364.10

End Mode

Begin Mode

Ordinary Annuity with Balloon Payment (Example 6)

R=10%

PV

0

1

2

3

100

100

1100

90.91

82.64

826.45

751.31 +75.13

1,000.00

For further practice, see Set 2, #18-19

Annuity Due with Balloon Payment (Example 7)

R=10%

0

1

2

100

100

100

3

1000

90.91

82.64

751.31

1,024.87

Insight into Calculator Software

-n

1 - (1+R)

x = PMT

R

{ [

•

•

•

•

]

k

(1+R) +

Balloon

n

(1+R)

k = 0, j = 0; then x is PV of ordinary annuity

k = 0, j = 1; then x is FV of ordinary annuity

k = 1, j = 0; then x is PV of annuity due

k = 1, j = 1; then x is FV of annuity due

}

jn

(1+R)

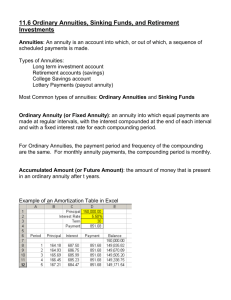

Amortizing Annuities: (Example 8)

•

Consider an annuity of $100 per year for 3 years, with interest of

10% compounded annually. Then the present value would be

$248.69, and the amorization table would be as follows:

Payment

number

1

2

3

Interest

Principal

Balance

$24.87

$17.36

$9.09

$75. 13

$82. 64

$90. 91

$173. 55

90. 91

0

Grouped Cash Flows: (Example 9)

R=10%

0

1

2

50 50

3

4

5

50 100 100

45.45

41.32

37.57

68.30

62.09

254.74

For further practice, see Set 2, #23

Deferred Annuities: (Example 10)

R=10%

0

1

2

3

0

0

0

4

5

100 100

68.30

62.09

130. 39

For further practice, see Set 2, #24

Annuities with Missed Payments:

R=10%

0

1

2

3

4

5

100 100 100 100 100

-100

100 100 0

90.91

82.64

0

68.30

62.09

303.95

100 100

Continuous Payment Streams

Rt

FV = Sum of all payments ×

e

-1

Rt

-Rt

PV = Sum of all payments ×

1-e

Rt

Example 12:

• Future value of $10,000 per year for 5 years,

discounted at 10% compounded continuously, with

payments spread continuously over the life of the

annuity, would be the following:

.5

FV = 50,000 ×

e

-1

= $64,872.13

.5

For further practice, see Set 2, #25

Example:

• Present value of $10,000 per year for 5 years,

discounted at 10% compounded continuously, with

payments spread continuously over the life of the

annuity, would be the following:

-.5

PV = 50,000 ×

1- e

= $39,346.93

.5

For further practice, see Set 2, #26