FINANCIAL REPORTING / TAX

The Death of LIFO?

Changing inventory method requires managing the

accounting-tax differences.

BY ROBERT BLOOM AND WILLIAM J. CENKER

JANUARY 2009

Few differences between IFRS and U.S. GAAP loom larger than accounting for inventories, particularly the disallowance

of the last-in, first-out (LIFO) method in IFRS. The proposed shift of U.S. public companies to IFRS could affect many

companies currently using LIFO for both financial reporting and taxation. This is because the conformity rule of IRC § 472

(c) requires taxpayers who apply LIFO for tax purposes to also apply it for income measurement in financial reporting, and

IFRS does not permit LIFO for book accounting.

Therefore, CPAs may be called upon to help manage inventory method changes. Companies using LIFO would have to

switch to FIFO or average cost. The change would place companies in violation of the conformity requirement. Absent

relief from the Treasury Department, it would require them to change their tax method of inventory reporting.

This article highlights the impact of LIFO accounting, widely used in the U.S. but scarcely used elsewhere. It could be

eliminated if U.S. GAAP were to fully conform to IFRS inventory accounting. If LIFO were to disappear, many U.S.

companies could face large income tax liabilities from accelerated income recognition. In 2007, Exxon Mobil Corp.

reported its aggregate replacement cost of inventories at year-end exceeded the inventories’ LIFO carrying value by $25.4

billion. The Sherwin-Williams Co. reported that if it had used FIFO instead of LIFO, its net income for 2005 would have

been $40.8 million higher (Exxon Mobil Corp., 2007 SEC Form 10-K; The Sherwin-Williams Co., 2007 SEC Form 10-K).

The proposed SEC road map released in November contemplates some large U.S. companies voluntarily adopting IFRS,

starting with filings in 2010. Its application could be mandated for large public companies starting in 2014.

Another major difference between IFRS and GAAP is that IFRS requires entities to carry inventory at the lower of cost or

net realizable value. GAAP, on the other hand, values inventories at the lower of cost or current replacement cost, which

is subject to a ceiling of net realizable value and a floor of net realizable value minus a normal profit margin.

ACCOUNTING FOR CHANGES IN INVENTORY METHODS

Currently, the GAAP guidance under Statement no. 154, Accounting Changes and Error Corrections, calls for changes in

inventory costing methods to be retrospectively applied to the prior financial statements presented in annual reports

(paragraph 7), unless it is impracticable to do so. In that case, the new principles can be applied prospectively

(paragraphs 8–9). An entity makes retrospective application only for the direct effects of the change (paragraph 10).

However, indirect effects—for example, bonuses—are reflected prospectively (paragraph 10).

Thus, a typical change in inventory method, such as from average cost to FIFO, is treated retrospectively. The entity

reflects a change from LIFO to FIFO in the same manner. The result (assuming that the accounting basis for inventory

under the new method exceeds the corresponding basis under the prior methods) is (1) an increase in inventory, (2) an

increase in current income taxes resulting from the effective increase in income, and (3) an adjustment to retained

earnings for the effect of the increase in net income. The entity may need to show a deferred tax liability for the temporary

difference between the accounting and tax bases for the inventory change if it were to remain, for example, on average

cost for tax purposes yet switch from average cost to FIFO for book purposes.

Over time, LIFO can have a significant cumulative downward effect on the inventory’s value. The cost of goods sold for

any particular year equals the sum of beginning inventory, plus purchases, less ending inventory. Thus, a lower ending

inventory increases cost of goods sold and reduces taxable income.

INCOME TAXATION OF INVENTORY METHOD CHANGES

For voluntary changes occurring in tax years ending on or after Dec. 31, 2001, IRC § 481(a) generally permits an entity to

deduct the entire change in the year of the change if the adjustment is favorable to the entity. Alternatively, if the

cumulative effect of the change increases the entity’s liability, the change may be taken into account over four years

beginning with the year of the change—with some exceptions—see "Timing Issues," below (Revenue Procedure 2008-52,

section 5.04). Therefore, instead of crediting Income Tax Payable for the total tax bill in the following journal entry, only

one-fourth of the tax would be treated as a current liability. The remainder would go into a Deferred Tax Liability account:

Inventory (asset increase)

Retained Earnings (stockholders' equity increase)

Income Tax Payable (liability increase)

Deferred Tax Liability (liability increase)

For income tax purposes, a change in the accounting method includes a change in the overall plan for reporting gross

income or deductions, or a change in the treatment of any material item (Revenue Procedure 2008-52 and Treas. Reg. §

1.446-1(e)(2)(ii)(a)).

An accounting change from LIFO to another method is made on Form 3115, Application for Change in Accounting

Method, and can either be an "advance consent request" or "automatic change request" (see instructions to Form 3115).

INCOME EFFECTS

Companies adopt LIFO primarily to lower their income tax liability and to postpone paying taxes, but it also reduces

income for financial reporting purposes. Nevertheless, companies are not required to use the same LIFO method for

taxation and accounting. For example, a unit LIFO method could be used in accounting and a dollar-value LIFO method in

taxation.

A change from LIFO will normally have a significant positive income effect because the accumulation of prior years’ costs

in beginning inventory will replace cost of goods sold valued at current costs. Assuming that the inventory turns over,

income for the year of change would increase by the entire amount of the LIFO reserve.

Rolling-Average Method

Another inventory issue in flux has been use of the rolling-average method. With Revenue Procedure 2008-43, the

Service in June reversed its long-held position against the method. The IRS formerly said the method did not clearly and

accurately reflect income, especially where inventory is held for long periods or its costs fluctuate significantly. The

revenue procedure provides a safe harbor for using a rolling-average method of inventory accounting and taxation. If the

rolling-average method is not used in accounting, this method may not accurately portray taxable income. An entity can

secure automatic consent to change its tax inventory method to the rolling average by complying with all the provisions of

this revenue procedure under IRC § 446(e).

TIMING ISSUES

Fortunately, the accounting change adjustment of establishing the opening LIFO reserve, as well as the initial section

263A capitalization amount, prevent amounts from being duplicated or omitted from income. Should the taxpayer be

required to include the section 481(a) amounts in the year of the change, the potential increase in tax liability can be

significant. Accordingly, such amounts are normally taken into income ratably over four years. If the entity follows

procedures properly, and if the LIFO reserve was not created over a short period, a four-year adjustment period will

normally be permitted. But if the change occurred because the entity did not apply LIFO properly, or did not file a timely

application, the total amount of the change may be required to be taken as income in the year of the change. See Treas.

Reg. § 1.481-4 and Revenue Procedure 2008-52. Thus, there will be a deferred tax liability associated with the switch in

the year of the change and the three following years.

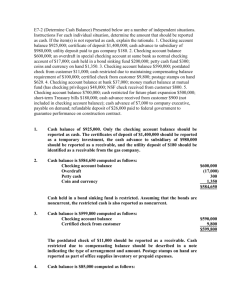

Example. To illustrate an inventory method change, assume BC Co. is a retail business. BC switches from dollar-value

LIFO to FIFO as of Jan. 1, 20X0, for both financial accounting and income taxation. The inventory at FIFO is $20 million,

and the dollar- value LIFO reserve is $4 million. BC secures IRS permission to spread the adjustment over four years.

A change from LIFO to any other method will impact the balance sheet as well as the income statement in the year of the

change. The LIFO reserve is a contra-asset or asset reduction account that companies use to adjust downward the cost

of inventory carried at FIFO to LIFO. Many companies use dollarvalue LIFO, since this method applies inflation factors to

"inventory pools" rather than adjusting individual inventory items. Companies that are on LIFO for taxation and financial

reporting typically use FIFO internally for pricing, purchasing and other inventory management functions.

For financial accounting purposes, the entity applies the change from LIFO to FIFO retrospectively. In this example in

particular, this means that FIFO is used as of day one in the year of the change (no matter when the change was actually

made in that year). All prior periods presented for comparative purposes are adjusted for the effects of the change. The

adjustment in the accounting books is made to reflect (1) an increase in the opening balance of inventory, (2) an increase

in retained earnings, and (3) an adjustment for income taxes. The following journal entries illustrate the effect of the

change from LIFO to FIFO, assuming an effective income tax rate of 35% and IRS approval to prorate the change over

four years:

12-31-20X0

Dollar Value LIFO Reserve

4,000,000

Retained Earnings

2,600,000

Income Taxes Payable

350,000

Deferred Income Taxes Payable

1,050,000

Then BC would prepare the following entry in each of the next three years:

12-31-20X1, 20X2, 20X3

Deferred Income Taxes Payable

Income Taxes Payable

350,000

350,000

In summary, a key difference between accounting and taxation for inventory methods occurs when the accounting method

is changed. The entity treats most of these changes retrospectively in accounting through retained earnings. However, the

Code and regulations require the cumulative effects of inventory method changes to be treated prospectively. In the case

of changing from LIFO, for tax purposes, the entity will generally spread the income effects caused by the change in the

opening inventory valuation over future years. By contrast, in accounting, the change is spread over past years, thus

affecting the deferred tax accounts of the entity.

LIFO SUPPORT?

Companies may well be reluctant to move to IFRS for inventory reporting if they are using LIFO, unless the LIFO

conformity rule were relaxed. Perhaps they would be allowed to still report LIFO for tax but to adhere to IFRS for

accounting. Maybe two sets of financial statements, one on IFRS, the other on GAAP permitting LIFO, would be allowed.

Another possibility would be for the Treasury Department to extend the period over which those tax obligations are due

beyond the currently allowed four years. Still another possibility would be for companies to offset the obligations against

net operating losses with carrybacks and carryforwards. Or perhaps different reporting standards could be used for larger

versus smaller companies. In any case, it is premature to say that LIFO is on its deathbed. Indeed, small companies not

required to use IFRS may very well stay on LIFO.

For tax planning purposes, companies may consider reducing their inventories and their LIFO reserves gradually between

now and changeover dates to IFRS. Some companies may decide to be early IFRS adopters, particularly if a net

operating loss or other tax situation could minimize the impact of recapturing the LIFO reserve. Or they could wait and see

what happens, anticipating some exception to the conformity principle or an extended section 481(a) period.

AICPA Seeks Gentle Transition

The IRS and Treasury had not as of late November issued guidance specific to IFRS-required changes in inventory

accounting methods. On Feb. 15 the AICPA noted in comments to the IRS that acquisitions or a change to IFRS may

require LIFO taxpayers to change to FIFO. "The AICPA does not believe the IRS national office should place impediments

on a taxpayer’s ability to discontinue the use of the LIFO inventory method, particularly in these circumstances," said the

letter signed by Jeffrey Hoops, then chairman of the AICPA Tax Executive Committee, and members of the Accounting

Methods Change Task Force. To facilitate LIFO discontinuance, the IRS should exempt an automatic LIFO termination

from the prior-change scope limitation, the letter recommended. The limitation occurs when a taxpayer has elected the

LIFO method within the previous five years. The letter was in response to a request for comments on proposed procedural

modifications to Revenue Procedure 97- 27 and Revenue Procedure 2002-9.

AICPA RESOURCES

The Tax Adviser and Tax Section

The Tax Adviser is available at a reduced subscription price to members of the Tax Section, which provides tools,

technologies and peer interaction to CPAs with tax practices. More than 23,000 CPAs are Tax Section members. The

Section keeps members up to date on tax legislative and regulatory developments. Visit the Tax Center at

www.aicpa.org/tax. The current issue of The Tax Adviser is available at www.aicpa.org/pubs/taxadv.

CPE

AICPA’s 2008 Corporate Income Tax Returns Workshop by Sid Kess, a CPE self-study course (#735213)

AICPA’s 2008 Tax Review Series: C Corporations, a CPE selfstudy course (#733641)

For more information or to order or register, visit www.cpa2biz.com or call the Institute at 888-777-7077.

EXECUTIVE SUMMARY

Voluntary changes in inventory costing methods generally are applied retrospectively for financial reporting

purposes. For taxation, entities generally may recognize resulting effects that increase tax liability ratably over four years.

Such considerations could come to the fore with the proposed adoption by U.S. public entities of IFRS, which does

not permit last in, first out (LIFO) for financial accounting. Many companies use LIFO primarily because it allows lower

income reporting for tax purposes. The conformity rule of IRC § 472(c) requires those companies to also use it for

financial accounting purposes.

For this and other reasons, CPAs may be called upon to advise companies switching from LIFO to FIFO (first in,

first out) or average cost.

A change from LIFO to FIFO typically would increase inventory and, for both tax and financial reporting purposes,

income for the year or years the adjustment is made.

Although the implications of IFRS for LIFO remain far from clear, companies now using the method may want to

consider reducing inventories and LIFO reserves in anticipation of a required change.

Robert Bloom , Ph.D., is a professor of accountancy at John Carroll University in University Heights, Ohio. His e-mail

address is rbloom@jcu.edu. William J. Cenker , CPA, Ph.D., was a professor of accountancy at John Carroll University.

He died in March.

Copyright © 2011 American Institute of Certified Public Accountants. All rights reserved.