Department of Accountancy

National Cheng Kung University

R112700 ADVANCED

MANAGEMENT ACCOUNTING

(高級管理會計)

Spring 2012 (100 學年度第 2 學期)

Explore and advance theories and practices in accounting to cultivate competitive

professionals with ethical integrity, innovative capabilities and international perspective to

meet business and social needs in the global economy.

General Program Learning Goals (goals covered by this course are indicated):

1

Graduates should be able to communicate effectively verbally and in writing.

2

Graduates should solve strategic problems with a creative and innovative approach.

3

Graduates should demonstrate leadership skills demanded of a person in authority.

4

Graduates should possess a global economic and management perspective.

5

Graduates should possess the necessary skills and values demanded of a true

professional.

Course Information

Course Number/Section: R112700

Course Title: ADVANCED MANAGEMENT ACCOUNTING

Days & Times: Thursday 2:10 pm to 5:00 pm

Professor Contact Information

Professor: Chaur-Shiuh Young

Office Phone: 53445

Email Address: actycs@mail.ncku.edu.tw

Office Location: Accounting 63402

Office Hours: Monday and Wednesday 2:00 pm to 3:30 pm or by appointment

Prerequisites:

MANAGEMENT ACCOUNTING

ECONOMETRICS

Course Description:

An advanced study of the concepts and techniques used by management accountants to

assist decision-makers within the organization. The purpose of this course is to prepare

students for CPA and industrial careers. More in-depth, real-world scenarios will be discussed

1

including process accounting, job-order accounting, measuring quality costs, activity-based

costing, product mix, capacity utilization, and evaluating performance. Students will be

introduced to methods currently being used by global businesses, including service firms and

manufacturers. There will be examinations and group presentations for the class.

Course Objectives:

To acquaint students of business with the fundamental tools of management accounting and to

advance their understanding of the dramatic ways in which the field is changing. This will

include an understanding of the state of the art in managerial accounting—activity-based

accounting, balanced scorecard, benchmarking, customer profitability analysis, just-in-time,

life-cycle costing, target costing and pricing decision. The emphasis through this course is to

equip students with the ability to manage an organization, playing the role of a business

consultant, working side-by-side in cross-functional teams with managers from all areas of

the organization. Students are also expected to be able to produce accounting information and

understand how managers are likely to use and react the information.

Textbooks:

Shank, J.K. 2006. Cases in Cost Management: A Strategic Emphasis. 3rd Ed. Cincinnati, Ohio:

Thomson South-Western Publishing. (華泰代理)

Atkinson, Kaplan, Matsumura, and Young. 2007. Management Accounting 5th ed. Pearson

Prentice Hall. (華泰代理)

Young, M. 2007. Readings in Management Accounting. 5th ed. Pearson Prentice Hall. (華泰

代理)

Cooper, R., and R. S. Kaplan. 1999. The Design of Cost Management Systems: Text & Cases,

2nd Ed. Upper Saddle River, New Jersey: Prentice-Hall.

Hansen, D. R. and M. M. Mowen. 2006. Cost Management: Accounting and Control. 5th Ed.

Mason, Ohio: Thomson South-Western. (華泰代理)

Hilton, R. W., M. W. Maher, and F. H. Selto. 2006. Cost Management: Strategies for

business decisions. 3rd Ed. New York, NY: McGraw-Hill/Irwin.

Lev, B. 2001. Intangibles: Management, Measurement, and Reporting. N.Y., Washington,

D.C.: THE BROOKINGS INSTITUTION.

Sunder, S. 1997. Theory of accounting and control. Cincinnati, Ohio: South-Western

Publishing.

杜榮瑞、華德、吳安妮合譯:轉捩點上的成本管理,遠流出版公司,1991 (原著:

Johnson/Kaplan:Relevance Lost 1987)

陳儀譯:管理會計與決策績效:活用成本控管執行力,打造穩健經營的高獲利組織,2004,

台北:麥格羅希爾 (原著:David Young:Techniques of Management Accounting: An

Essential Guide for Managers and Financial Professionals, 2003)

Course Contents

2

1. Understanding Cost Behavior

2. Resources Allocation, Budgeting and Variance Analysis

Case 9: Boston Creamery, Inc.

Case 27: Petersen Pottery

3. Activity-Based Cost Management

Kaplan, R. S., and R. Cooper. 1998. Cost & effect: Using integrated cost systems to drive

profitability and performance. Boston, MA: Harvard Business School Press.

Case 4: Allied Office Products

Case 31: Sloan Styles

4. Cost/Accounting Information and Decision Making: Cost Information for Pricing and

Product Planning

Case 10: Brunswick Plastics

5. Strategic Cost Management (SCM)

Shank, J.K. 2006. Cases in Cost Management: A Strategic Emphasis. 3rd Ed. Cincinnati, Ohio:

South-Western Publishing.

Shank, J.K. and V. Govindarajan. 1989. Strategic Cost Analysis: The Evolution from

Managerial to Strategic Accounting. Boston, MA: IRWIN.

Shank, J.K. and V. Govindarajan. 1993. Strategic Cost Management: The New Tool for

Competitive Advantage. New York, NY: The free press.

Case 6: Baldwin Bicycle Company

6. The Design of Management Accounting System

7. Intangibles (Intellectual Capital)

8. Performance Evaluation: Nonfinancial Performance & Balanced Scorecard

Case 19: Jones Ironworks

9. Incentive System: CEO Compensation & Turnover

10. Hospital Cost Management and Non-for-Profit Organization

11. The valuation implications of Cost/Non-financial Measures

Case 18: Graham, Inc.

12. Manipulation of Cost/Accounting Information

3

13. Corporate Governance

Grading policy:

(1) Presentations: 25%

(2) Instructor Grade: 20%

(3) Mid-term Exam: 25%

(4) Final Examination: 30%

Note:

1.

You are expected to attend each exam, except under the most extreme circumstances.

You will be required to submit a written letter detailing your reason for missing any exam

before a make-up will be considered.

2. The content and grading criteria of the written paper will be given out in class later.

3. The 20% Instructor grade will consist of 10% of quizzes and 10% on class participation.

Quizzes will be given according to the course schedule. There will be no make-ups for

quizzes; however, I will drop one ‘awful’ quiz when computing your final course grade.

Course Policies

Make-up exams

Make-up exams will be given only under extenuating circumstances arising from

medical or family emergencies. Documented evidence that you were seriously ill or

experienced a family emergency at the scheduled time of an exam is required. In order to

be excused from an exam, you must contact me prior to the exam and be ready to provide

documentation after the exam. Students who do not show up for an exam without making

arrangements with me according to the preceding rules will receive an exam grade of zero. It

is your responsibility to note the exam dates and let me know at the beginning of the semester

if you foresee any conflicts. It is also your responsibility to ensure that you do not schedule

any job interviews or travel for official or personal reasons during exam days.

Class Attendance

Attendance will be randomly taken. 3-4 students per group. Each group acts as the reporting

group and the comment group. There will be ten groups. The reporting group reads, reports

the assigned article and finds out the solutions to the questions attached to the article. The

comment group gives comments on the reports of the reporting group.

Classroom Behavior:

You are expected to be in class on time.

There is no eating or drinking in the classroom.

Turn off cell-phone while in class.

Please come to class with a pen/pencil, paper to write on, and an open mind.

Courtesy and respect for your teacher and classmates is expected and required.

4

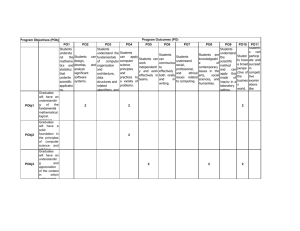

Grading Policy/評量方式:

Presentations

25%

COMMU

CPSI

Oral Commu./ Presentation

Mid-term Exam

25%

Final

Examination

30%

60%

Instructor

Grade

20%

25%

Written Communication

30%

30%

Creativity and Innovation

30%

30%

Problem Solving

40%

40%

25%

Computational Skills

LEAD

GLOB

Leadership & Ethic

Social responsibility

Global Awareness

40%

Values, Skills & Profess.

VSP

Information Technology

Management Skills

5

50%