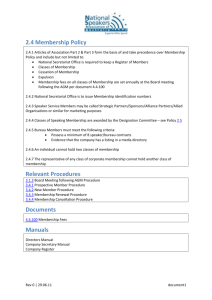

Publication and laying of financial statements and reports — flowchart

advertisement

Publication and laying of financial statements and reports — flowchart Directors have prepared the company’s financial statements and reports for the financial year (Companies Ordinance, Cap 622 (CO), ss 379, 388) Does the company wish to circulate a full set of the reporting documents? Yes Is an annual general meeting (AGM) required? (CO, s 610) The company and the directors must meet any obligation to publish and lay the reporting documents (CO, ss 429, 430) No Yes Members with such notice Do the company’s articles prohibit the sending of summary financial reports? (CO, s 446) No Any notice from members validly requesting a full set of the reporting documents? (CO, ss 442-444) Members without such notice Is an annual general meeting (AGM) required? (CO, s 610) No Is AGM not required by virtue of CO, s 612(1) or (2)? Yes Yes The company must send copies of the reporting documents to members at least 21 days prior to AGM. Directors must then lay a copy before AGM (CO, ss 429(1), 430(1)) If CO, s 612(2) applies If CO, s 612(1) applies No If, by virtue of CO, s 612, an AGM is not required, the company must send copies of the reporting documents to members within a certain period (CO, ss 430(3), 612(1)(b)) The company may send copies of the summary financial report to members at least 21 days prior to AGM. Directors must then lay a copy of the full reporting documents before AGM (CO, ss 429(1), 432(3), 441) The company may send copies of the summary financial report to members within a certain period (CO, ss 430(3), 432(3), 441) The company must send copies of the full reporting documents to members on or before the circulation date of the relevant written resolution (CO, s 612(1)(b)) This Practice Note, in the form of a flowchart, illustrates the general requirements in relation to the publication and laying of the annual financial statements and reports of a company, as set out in Part 9 of the Companies Ordinance (Cap 622) (CO). It also summarises the general requirements in relation to the sending of summary financial reports. The flowchart focuses on requirements that apply to companies in general. Other specific rules in CO relating to financial statements and reports will vary according to whether the company is a small or medium-sized company that is eligible for simplified reporting or whether the company is dormant. Note that if the full reporting documents are to be made available on a website, see CO, ss 430(4), 430(5) and 833. In the context of a member requesting an electronic copy or website publication of either the full reporting documents or summary financial report, see CO, ss 442(3), 442(4), 443(1)(d), 443(3)(d) and 443(4). For more details, see Practice Note: Publication and laying of financial statements and reports and Practice Note: Summary financial reports.