Important Tax Information

advertisement

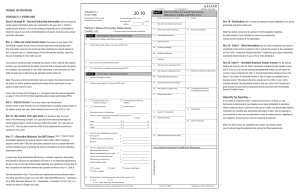

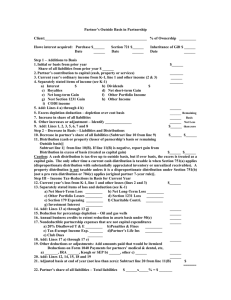

Important Tax Information ATEL Investor Services February 2012 Privacy Policy ATEL values the trust you have placed in us. As a part of our relationship, we respect and acknowledge your privacy. Regulations issued by the Federal Trade Commission and the Securities and Exchange Commission require that ATEL and its affiliates (together, the “ATEL Companies”) and each of the investment programs sponsored and managed by the ATEL Companies (the “Funds”), provide the Funds’ investors with written notice of their policies and procedures for disclosure of the investors’ nonpublic personal information. Dear Investor: Please find your copy of the Schedule K-1 (Federal Form 1065) “Partner’s Share of Income, Credits, Deductions, etc.,” for 2011. Please use this form in preparing your tax return or provide it to your tax advisor. You will receive a separate Schedule K-1 for each ATEL Fund in which you have invested. All the items shown on the Schedule K-1 are subject to future adjustments by federal and state taxing authorities. Our policies relating to disclosure of your nonpublic personal information are as follows: 1. We collect nonpublic personal information about you from the following sources: THE TAX BASIS CAPITAL ACCOUNT VALUE AND THE TAX INCOME/LOSS REFLECTED ON ITEM L ARE USED FOR TAX ACCOUNTING PURPOSES ONLY AND DO NOT REFLECT THE ECONOMIC VALUE OF THE INVESTMENT. THE TRUE VALUE OF YOUR INVESTMENT IS IN THE FUTURE RENTAL REVENUES AND SALES PROCEEDS TO BE GENERATED BY THE EQUIPMENT IN THE FUND. • Information we receive from you on applications or other forms, • Information about your transactions with us, our affiliates, or others, and • Information we receive from a consumer‐reporting agency. 2. We do not disclose any nonpublic personal information about Fund investors or former investors to anyone, except as permitted by law. If your investment is held by a trustee, please note that some trust companies have requested us to send the Schedule K-1 directly to their investors. If you are a tax exempt entity and if your gross Unrelated Business Taxable Income (UBTI) from all sources equals or exceeds $1,000, you are required to file Form 990-T. If you are required to file this form, your share of Unrelated Business Income is reported in Box 20, Code V. The tax identification number on the Schedule K-1 is the trustee’s, not your own. If you have any questions about completing Form 990-T, please contact your trustee/IRA custodian. 3. We restrict access to nonpublic personal information about you to employees and agents of ATEL who need to know that information to provide services to you and the Fund in which you have invested, and require that all such employees and agents adhere to our privacy policy. Furthermore, ATEL has confirmed that each provider of administrative services to the Funds is also governed by the FTC and/or SEC privacy rules and will maintain a similar policy with regard to protecting the privacy of your nonpublic personal information. 4. We maintain physical, electronic, and procedural safeguards that comply with federal standards to guard your nonpublic personal financial information. 5. We will not permit any ATEL Company which has no prior business relationship with you to market its products or services to you based on information another ATEL Company may collect from you, including, but not limited to, information concerning your income and net worth, your credit score and your account history with the ATEL Company. ATEL employees are not familiar with your individual tax circumstances and are not qualified to give you tax advice. In order to assure that you receive the most accurate information, we recommend that you consult your personal tax advisor regarding matters relating to your tax return. For detailed instructions about your Schedule K-1 please visit the IRS website http://www.irs.gov/pub/irs-pdf/i1065sk1.pdf. To visit your local IRS office for assistance, please visit http://www.irs.gov/localcontacts/index.html. To contact the IRS for tax assistance, please call the IRS toll free tax assistance line at 1-800-829-1040 for individual tax questions. If you have any questions about these policies or our use, maintenance and disclosure of your nonpublic personal financial information, please contact our Investor Services Department at (800) 543‐2835, ext. 3. We are required by law to inform you of our privacy policy once a year. Please note that this is not a request for an “opt out” statement from you; the above stated policies are the policies in place at this time. Dean Cash President ATEL Financial Services, LLC ATEL SECURITIES CORPORATION 600 California Street, 6th Floor • San Francisco, CA 94108-2733 • (800) 543-2835 ext. 3 • Fax: (800) 322-2835 • www.atel.com • ais@atel.com 2-11-12 600 California Street, 6th Floor • San Francisco, CA 94108-2733 • (800) 543-2835 ext. 3 • Fax: (800) 322-2835 • www.atel.com • ais@atel.com 651111 FEDERAL TAX REPORTING 20 11 Schedule K-1 (Form 1065) SCHEDULE K-1 (FORM 1065) Items A through M - Partner/Partnership Information: Items A through M contain general information about your investment for the year. Item L “Partner’s capital account analysis” is for tax accounting purposes only and is not intended to reflect the value of your units or the Partnership’s net assets. Consult your tax advisor Final K-1 Department of the Treasury Internal Revenue Service Part III For calendar year 2011, or tax year beginning , 20 Partner’s Share of Income, Deductions, See back of form and separate instructions. Credits, etc. Part I A Information About the Partnership B 1 Ordinary business income (loss) 2 Net rental real estate income (loss) 3 Other net rental income (loss) 4 Guaranteed payments 5 Interest income 6a Ordinary dividends 6b Qualified dividends 15 Credits Box 19- Distributions: Box 19 (code A) represents money distributed to you by the partnership during the taxable year. 16 Foreign transactions interest and the character of the distribution.) Box 20- Code A - Other Information: Box 20, Code A represents your share of Partnership’s name, address, city, state, and ZIP code than real estate. If you have an overall gain after combining the amount reported in Box 3, any prior year un-allowed losses, and all other passive activities, report the investment income which is included in Box 5. Include this amount in the computation on Form 4952, “Investment Interest Deduction” to determine your share of deductible income on Schedule E, Form 1040, Line 28. investment interest expense, if any, on Form 1040, Schedule A. If you have an overall loss after combining the amount on Box 3 with all other passive C loss limitation rules employed on Form 8582. Worksheets in the instructions for Form Royalties 8 Net short-term capital gain (loss) 9a Net long-term capital gain (loss) Box 20, Code V – Unrelated Business Taxable Income: For tax exempt entities the amount in Box 20, Code V represents unrelated business taxable income Check if this is a publicly traded partnership (PTP) D 8582 will assist you in determining the allowable portion of the loss. 7 IRS Center where partnership filed return activities, you must determine the portion of the loss that is allowed under the passive Part II 17 Alternative minimum tax (AMT) items Information About the Partner tax advisor for further guidance regarding the proper filing requirements for your Partner’s identifying number 9b Collectibles (28%) gain (loss) F Partner’s name, address, city, state, and ZIP code 9c Unrecaptured section 1250 gain schedule attached. This attachment should include your share of the Partnership’s 10 Net section 1231 gain (loss) 11 Other income (loss) business income. This amount should be reported on Form 990-T, Line 5 with a If Part I, Box D of your 2011 Schedule K-1 is checked, follow the special instructions on page 12 of the 2011 Form 8582 regarding publicly traded partnerships (PTPs). interest income. These amounts are not considered part of a passive activity subject to 18 Tax-exempt income and nondeductible expenses General partner or LLC member-manager Limited partner or other LLC member H Domestic partner Foreign partner If you reside in a state/city where a state/city income tax is in effect, or if the Partnership is determined to have taxable income (loss) attributable to operations 19 I What type of entity is this partner? J Partner’s share of profit, loss, and capital (see instructions): Beginning share of the Partnership’s section 1231 gain (loss) from sales and exchanges of certain property used in a trade or business. Report the section 1231 gain (loss) on Form 4797. You may need to use Form 8582 to first determine the amount to be 12 Section 179 deduction 13 Other deductions Distributions Ending your residency. Income tax laws vary from state/city to state/city. 20 Other information % % Loss % % (Note: The state income tax regulations are complex. You should consult Capital % % your tax advisor regarding potential state income tax filing requirements.) Partner’s share of liabilities at year end: Nonrecourse depreciation adjustment on property placed in service after 1986: For property placed in service after 1986, the depreciation deduction used to compute alternative L depreciation system. . . $ Qualified nonrecourse financing . $ Recourse . $ . $ . . . . . . . . . . Current year increase (decrease) Withdrawals & distributions Ending capital account . the gain or loss on the sale of these assets. Generally, any adjustments to these gain or loss calculations for alternative minimum tax purposes are found on Box 17, Code B. Tax basis . $ . $ . . $ . . $ ( GAAP ) Section 704(b) book Other (explain) Use the information in Box 17 (as well as your adjustments and tax preference items from other sources) to prepare your Form 6251, Alternative Minimum Tax – Individuals: Form 4626, Alternative Minimum Tax – Corporations; or Schedule I of Form 1041 U.S. Income Tax Return for Estates and Trusts. M Self-employment earnings (loss) *See attached statement for additional information. . Capital contributed during the year and alternative minimum tax depreciation) will result in a corresponding adjustment to 14 Partner’s capital account analysis: Beginning capital account . In most cases, these depreciation differences (i.e. between regular tax depreciation instructions for reporting your partnership information. A return may be required by Profit For IRS Use Only K Box 17, Code A shows within a state/city where a state/city income tax is in effect, you should obtain detailed each state/city in which you are determined to have a taxable presence, regardless of reported on Form 4797. minimum taxable income is generally the amount calculated by using the alternative gross income and your share of deductions directly connected with the Unrelated Business Taxable Income. State/City Tax Reporting — G the passive activity loss rules. Report interest income on line 8a of Form 1040. Box 10- Net section 1231 gain (loss): The amount on Box 10 is your income or loss on Federal Form 990-T, “Exempt Organization Business Income Tax E passive activity income or loss.) Box 5 - Interest Income: This is your share of the Partnership’s (UBTI). If you are a tax exempt entity and are required to file a return, you will report this Return.” Your share of Partnership income or loss is treated as unrelated trade or (Note: The passive activity loss limitation rules are complex. You should consult your Box 17 – Alternative Minimum Tax (AMT) items: (Note: You should consult your tax advisor for further guidance regarding the determination of your adjusted tax basis in your partnership Partnership’s employer identification number Box 3 - Other net rental income (loss): This amount is your share of the Partnership’s passive activity net income (loss) from rental activities other Partner’s Share of Current Year Income, Deductions, Credits, and Other Items , 2011 ending for further information. OMB No. 1545-0099 Amended K-1 Did the partner contribute property with a built-in gain or loss? Yes No If “Yes,” attach statement (see instructions) For Paperwork Reduction Act Notice, see Instructions for Form 1065. Cat. No. 11394R Schedule K-1 (Form 1065) 2011