Solutions to Year-End Review Package: Chapters 1 and 2 PART I

advertisement

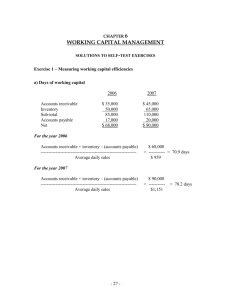

Solutions to Year-End Review Package: Chapters 1 and 2 PART I — MULTIPLE CHOICE 1. 2. 3. d b c 4. 5. 6. a c d 7. 8. 9. d b c 10. 11. 12. c d a 13. 14. 15. b d d 16. 17. 18. c d d PART II — JOURNAL ENTRIES 0. 1. 2. 3. 4. 5. 6. Account(s) Debited 1 8 6 1 None 15 None Account(s) Credited 11 1 10 13 None 1 None 7. 8. 9. 10. 11. 12. 13. Account(s) Debited 17 3 5 1 2 12 18 Account(s) Credited 1 8 1 9 13 1 1 PART III — SHORT PROBLEMS A. Ending Capital, 12/31/01 ................................................................................. Beginning Capital, 1/1/01................................................................................ Increase in capital balance ............................................................................... Withdrawals during 2001 ................................................................................ Investments during 2001 ................................................................................. Net income in 2001 ......................................................................................... $140,000 125,000 15,000 38,000 53,000 20,000 $ 33,000 B. Total liabilities, $50,000 (Beginning of year). Total owner’s equity, $30,000 (End of year). Expenses during the year, $65,000. PART IV — TYPES OF ACCOUNTS Debit 1. 2. 3. 4. 5. 6. 7. 8. 9. 10. Credit Asset Liability Owner’s Equity Solutions: Chapters 3 and 4 PART I — MULTIPLE CHOICE 1. 2. 3. a c b 4. 5. 6. d d b 7. 8. 9. d c a 10. 11. 12. c b a 13. b PART II — FINANCIAL STATEMENT PREPARATION PENA SERVICE AGENCY Income Statement For the Month Ended September 30, 2001 Revenues: Service revenue Expenses: Interest expense Salaries expense Supplies expense Rent expense Insurance expense Total expenses Net income $16,000 $ 400 4,000 1,500 2,000 1,200 9,100 $ 6,900 PENA SERVICE AGENCY Balance Sheet At September 30, 2001 Assets Cash Fees receivable Supplies Prepaid insurance Prepaid rent Equipment Less: Accumulated amortization Total assets Liabilities and Owner’s Equity Liabilities: Notes payable Accounts payable Salaries payable Interest payable Unearned revenue Total liabilities Owner’s equity: J. Pena, Capital (1) Total liabilities and owner’s equity (1) J. Pena, Capital — Beginning $ 9,825 Less: drawings 2,000 Add: net income 6,900 $14,725 $ 6,500 1,000 3,075 2,000 500 $35,000 4,000 31,000 $44,075 $14,000 12,000 1,300 50 2,000 29,350 14,725 $44,075 PART III — ADJUSTING ENTRIES Account(s) Account(s) Dollar Debited Credited Amount 0. 3 12 $500 1. 15 8 $1,440 2. 10 13 $5,000 3. 14 7 $12,000 4. 2 13 $500 PART IV—CLOSING ENTRIES 1. X 6. 2. X 7. 3. C 8. 4. C 9. 5. C 10. D D X X X PART V—BALANCE SHEET CLASSIFICATIONS 1. F 6. D 2. D 7. C 3. A 8. G 4. D 9. G 5. C 10. A Account(s) Debited 5. 17 6. 18 7. 16 8. 3 11. 12. 13. C X X 11. 12. 13. 14. 15. A D C A E Account(s) Credited 4 5 9 12 Dollar Amount $5,000 $1,500 $400 $800 16. 17. G C Solutions: Chapters 5 and 6 PART I — MULTIPLE CHOICE 1. 2. 3. a a b 4. 5. 6. a b d 7. 8. 9. a c b 10. 11. 12. d c d 13. 14. 15. c d b 16. 17. b b PART II — BASIC INVENTORY CALCULATIONS (a) Average ending inventory: 500 × $20 = $10,000 Average cost of goods sold 1,250 × $20 = $25,000 Average cost = $35,000 ÷ 1,750 = $20 (b) FIFO ending inventory: 425 × $26 = 75 × $22 = (c) LIFO ending inventory: 400 × $14 = 100 × $18 = $11,050 1,650 $12,700 FIFO cost of goods sold 400 × $14 = 375 × $18 = 250 × $20 = 225 × $22 = $5,600 1,800 $7,400 LIFO cost of goods sold 425 × $26 = 300 × $20 = 250 × $20 = 275 × $18 = $ 5,600 6,750 5,000 4,950 $22,300 $11,050 6,600 5,000 4,950 $27,600 PART III — CLOSING ENTRIES —————————————————————————————————————————— Not Closed Account Closed Debit Credit —————————————————————————————————————————— 1. Purchase Returns and Allowances ................................................ X 2. Freight In ...................................................................................... X 3. Sales .............................................................................................. X 4. Merchandise Inventory (Ending) .................................................. X 5. Sales Returns and Allowances ..................................................... X 6. H. Carey, Drawings ...................................................................... X 7. Freight Out ................................................................................... X 8. H. Carey, Capital ......................................................................... X 9. Merchandise Inventory (Beginning) ............................................ X 10. Cash ............................................................................................. X *PART IV — INVENTORY: SHORT PROBLEMS A. Net Sales ($200,000 – $25,000) ........................................................................................ Less estimated gross profit (40% × 175,000).................................................................... Estimated cost of goods sold ............................................................................................. $175,000 70,000 $105,000 Beginning inventory.......................................................................................................... Cost of goods purchased ($140,000 – $5,000 + $19,000)................................................. Cost of goods available for sale ........................................................................................ Less: estimated cost of goods sold .................................................................................... Estimated cost of ending inventory ................................................................................... Less: undamaged inventory .............................................................................................. Estimated cost of merchandise lost in fire ........................................................................ $ 30,000 153,000 183,000 105,000 78,000 25,000 $ 53,000 B. Beginning inventory ....................................................................................... Purchases ........................................................................................................ Goods available for sale .................................................................................. Net sales .......................................................................................................... Ending inventory at retail ............................................................................... Cost to retail ratio ($120,000 ÷ $160,000) = 75% Ending inventory at cost ($60,000 × 75%) ..................................................... C. Total cost = Total market Write down required At Cost $ 25,000 95,000 $120,000 At Retail $ 35,000 125,000 $160,000 100,000 $ 60,000 $ 45,000 $19,950 19,610 $ 340 Loss Due to Decline in Net Realizable Value in Inventory .................................... Merchandise Inventory ......................................................................... To record decline in inventory from original cost of $19,950 to current NRV of $19,610. 340 340 PART V –– MULTIPLE-STEP INCOME STATEMENT BYRNE INDUSTRIES Income Statement For the Year Ended December 31, 2002 Sales revenues Sales (sales returns and allowances — $30,000) Less: Sales returns and allowances Net sales Cost of goods sold Gross profit Operating expenses Wages expense Selling expense Amortization expense — store equipment Freight out Total operating expenses $630,000 30,000 600,000 275,000 325,000 $967,500 60,000 16,000 6,000 149,500 Income from operations 175,500 Other revenue and gains Interest revenue $ 2,700 Other expenses and loses Interest expense Loss on sale of equipment Total non-operating expenses and losses $12,300 4,800 $17,100 Net non-operating expenses and losses Net Income 14,400 $161,100 Solutions: Chapters 9 –11 PART I — MULTIPLE CHOICE 1. 2. 3. b b d 4. 5. 6. a c a 7. 8. 9. a a d 10. 11. 12. a c d 13. 14. a b PART III — MATCHING 1. A 2. C 3. C 4. A 5. B PART III — AMORTIZATION METHODS Straight-line [($900,000 – $100,000) ÷ 10] 2000 $ 80,000 Double declining-balance (10% × 2 = 20%) 2000 $900,000 × .20 2001 ($900,000 – $180,000) × .20 $180,000 Units-of-Activity ($900,000 – $100,000) ÷ 1,000,000 = $.80/unit 2000 60,000 × $.80 2001 120,000 × $.80 $ 48,000 2001 $ 80,000 $144,000 $ 96,000 PART IV — RECEIVABLES A. UNCOLLECTIBLE ACCOUNTS (1) Bad Debts Expense ....................................................................................... Allowance for Doubtful Accounts ($500 + $7,000) .......................... (2) (3) (4) 7,500 7,500 Bad Debts Expense (1% × $740,000) ........................................................... Allowance for Doubtful Accounts ................................................... 7,400 Allowance for Doubtful Accounts ................................................................ Accounts Receivable ........................................................................ 400 Accounts Receivable .................................................................................... Allowance for Doubtful Accounts ................................................... 400 7,400 400 400 Cash ............................................................................................................ 200 Accounts Receivable ........................................................................ B. July Nov. Nov. 200 NOTES RECEIVABLE 1 Notes Receivable ........................................................................................ Accounts Receivable ........................................................................ 6,000 6,000 1 Cash .......................................................................................................... 6,160 Notes Receivable .............................................................................. Interest Revenue ............................................................................... 1 Accounts Receivable .................................................................................. Notes Receivable .............................................................................. Interest Revenue ............................................................................... 6,000 160 6,160 6,000 160 PART V — CAPITAL ASSETS: SHORT PROBLEMS A. B. C. D. Land .......................................................................................................... 390,000 Building ...................................................................................................... 210,000 Cash ................................................................................................. 600,000 Revised annual amortization Book value, 1/1/00 ($100,000 – $18,000) .................................................................... Less: New salvage value .............................................................................................. Amortizable cost .......................................................................................................... $ 82,000 12,000 $ 70,000 Remaining useful life ................................................................................................... 5 years Revised annual amortization ($70,000 ÷ 5) ................................................................. $14,000 2000 amortization: $300,000 × .40 × 1/2 = $60,000 2001 amortization: ($300,000 – $60,000) ×.40 = $96,000 Cash .......................................................................................................... 12,000 Accumulated Amortization .......................................................................... Crane ................................................................................................. Gain on Sale of Crane ....................................................................... 7,000 18,000 1,000 PART VI — PAYROLL CALCULATIONS a. b. c. d. e. $330 $314.96 $13.50 Zero $43.99 PART VII — INTEREST ON SHORT-TERM NOTES PAYABLE Note to be Interest Payable 2002 Interest Case Principal Interest Rate Note Given Repaid 12/31/01 Expense ——————————————————————————————————————————— 1. $60,000 8% 9/30/01 9/30/02 $1,200 $3,600 2. $30,000 10% 9/1/00 3/1/01 Zero XXXX 3. $45,000 8% 6/30/01 or 7/1/01 3/31/02 or 4/1/02 $1,800 $ 900 4. $20,000 9% 4/1/01 4/1/02 1,350 XXXX 5. $50,000 12% 12/1/01 3/1/02 XXXX 1,000 6. $80,000 8% 10/1/01 6/1/02 1,600 XXXX Solutions: Chapters 14-15 PART I — MULTIPLE CHOICE 1. 2. 3. 4. 5. 6. d d c d a b 7. 8. 9. 10. 11. 12. a b b a d b 13. 14. 15. 16. 17. c d d d c PART II — DIVIDEND CALCULATIONS 1. 2. 3. $15,000. $60,000. $30,000. 4. 5. 6. $15,000. $10,000. $147,000. PART III — STOCK SPLITS, DIVIDENDS, AND RESTRICTIONS OF RETAINED EARNINGS 1. 2. 3. 4. 5. B C C A C 6. 7. 8. 9. 10. D A B A C PART IV — EARNINGS PER SHARE 1. 2. 3. $2.00 $.70 $1.00 PART V — INCOME STATEMENT AMOUNTS 1. 2. 3. 4. decrease increase decrease $45,000. $56,000. $24,000. $zero. Solutions: Chapter 16 PART I — MULTIPLE CHOICE 1. c 2. b PART II — BOND CALCULATIONS 1. 2. $36,234. $37,480.80. 3. 4. loss of $40,222.50. $51,055.20. PART III — BOND ENTRIES 1. 2. Debit 1 Credit 5 9 Amount $208,000 200,000 8,000 1 800 11,200 12,000 9 6 3. 4. Debit 6 Credit 12 14 Amount $ 11,000 1,000 10,000 1 200,000 4,800 204,800 5 9 Solutions: Chapters 18-19 PART I — MULTIPLE CHOICE 1. 2. 3. 4. 5. a d d b b 6. 7. 8. 9. 10. d d a b d 11. 12. 13. 14. c d a b PART II — RATIO ANALYSIS 1. 2. 3. 4. 5. 20.00 1.60 5.00 47.37 .45 6. 7. 8. 9. 4.00 34.55 8.00 3.00 PART III —CASH FLOW STATEMENT CLASSIFICATIONS 1. 2. 3. 4. 5. F F C D B 6. 7. 8. 9. 10. D B E G A PART IV — CASH FLOW STATEMENT — Indirect Method ZIMMER CORPORATION Cash Flow Statement For the Year Ended December 31, 2002 Cash flows from operating activities Net income Adjustments to reconcile net income to net cash provided by operating activities Amortization expense Increase in accounts receivable Decrease in inventory Increase in accounts payable Decrease in accrued expenses payable Net cash provided by operating activities Cash flows from investing activities Purchase of equipment Net cash used by investing activities Cash flows from financing activities Payment of dividends Net cash used by financing activities Net increase in cash Cash at beginning of period Cash at end of period Noncash investing and financing activities Land was acquired by issuing common shares $28,000 $25,000 (7,000) 10,000 43,000 (6,000) 65,000 93,000 (50,000) (50,000) (5,000) (5,000) 38,000 20,000 $58,000 $70,000 PART IV — CASH FLOW STATEMENT — Direct Method ZIMMER CORPORATION Cash Flow Statement For the Year Ended December 31, 2002 Cash flow from operating activities Cash receipts from customers ($290,000 – $7,000) Cash payments: To suppliers ($110,000 – $10,000 – $43,000) For operating expenses ($90,000 – $25,000 + $6,000) For interest For income taxes Net cash provided by operating activities Cash flows from investing activities Purchase of equipment Net cash used by investing activities Cash flows from financing activities Payment of dividends Net cash used by financing activities Net increase in cash Cash at beginning of period Cash at end of period Noncash investing and financing activities Land was acquired by issuing long-term bonds $283,000 $57,000 71,000 50,000 12,000 190,000 93,000 (50,000) (50,000) (5,000) (5,000) 38,000 20,000 $58,000 $70,000