Natural Gas Pricing in Russia

advertisement

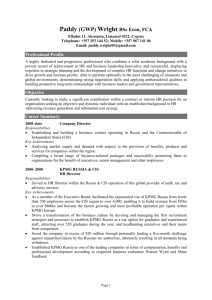

The Merits of Dual Pricing of Russian Natural Gas David Tarr and Peter Thomson The World Bank* Abstract: During the accession negotiations to enter the World Trade Organization, the question has arisen whether Russia should charge the same price for the exports of its natural gas as it charges in its home market. Our economic analysis suggests that pipelines allow Gazprom to segment the Russian market from the European (including Turkey) market and that Russia has market power in the European market. Based on this market power assumption, we develop and estimate a model in which we assume that Russia is optimizing the price and quantity that it sells in Europe—this was between $79 and $99 per thousand cubic meters (TCM) plus $27 transport costs in 2000 and 2001. We believe that the Russian market would be better served by competition, but while Gazprom retains a near monopoly, the analysis suggests that Russia should allow Gazprom to raise its domestic prices of natural gas from about $15 to $20 per TCM to the full long run marginal costs (about $35 to $40 per TCM). This would result in benefits to Russia of about $1.24 billion dollars per year. The analysis also reveals that, from Russia’s perspective, there is no economic rationale to unify the price of natural gas it sells domestically and abroad. If Russia were to sell its natural gas to Europe at only full long run marginal cost plus transportation costs, Russia would lose between $5 billion and $7.5 billion per year. On the other hand, consumers in Europe would gain even more (between $7.5 billion and $10 billion per year), as they would consume more gas at lower prices. If, instead, Russia were to raise its domestic prices to the prices it charges in Europe, Russian industry would incur very large adjustment costs as the gas cost increases would adversely impact on investment and unemployment in the short run. Absorbing the cost increases would induce Russian industry to switch to alternate fuels and produce less gas intensive products that cannot be justified on the basis of Russia’s comparative advantage. We estimate that the efficient world price would be achieved if Gazprom were to employ its optimal “two part tariff.” This means that Gazprom would sell gas to European gas companies at its long-run marginal cost plus transportation costs of about $67 per TCM, plus an access fee for the right to buy gas of between $12 to $15 billion per year. The optimal two part tariff would double Gazprom’s annual profits in Europe, but it involves significant long-term risks of lost market share. By identifying the stakes-- who gains and who loses— we hope that we will inform the debate on this important policy issue. * We thank Harry Broadman, Vladimir Drebentsov, Kevin Fletcher, Bernard Hoekman, Hiddo Houben, Jesper Jensen, Jeffrey Lewis, Johannes Linn, Charles McClure, Petros Mavroidis, Pradeep Mitra, Costas Michalopoulos, Alexander Morozov, Hossein Razavi, Christof Rühl, Thomas Rutherford, Julian Schweitzer, Richard Self, Clint Shiells, Nicholas Stern and Deborah Wetzel for helpful comments and discussions and Maria Kasilag for logistical support. The Merits of Dual Pricing of Russian Natural Gas David Tarr and Peter Thomson The World Bank July 19, 2003 I. Introduction Dual energy pricing (lower energy prices in Russia than on energy exports) has become a subject of some controversy. On the one hand, some WTO member countries claim that dual energy pricing is an export subsidy for Russian exporters whose products embody energy. On the other side, Russian officials argue that dual energy pricing is an export subsidy only if the energy embodied in exported goods is priced lower than domestic energy—which, they argue, is not the case in the present situation. In the context of Russia’s WTO accession, some members have sought a commitment by Russia to unify gas pricing. The request for unified energy pricing is perceived in Russia as imposing large economic costs in terms of lost profits on sales in Europe (including Turkey) because of the decrease in export prices, or increased unemployment and resource misallocation costs at home caused by the imposition of higher prices, or a combination of both.1 The objective of this note is to contribute to the discussion of dual energy pricing by examining the economics of natural gas pricing on Russia and its major consumers. We argue that the Russian market would be better served by the introduction of competition, but while Gazprom retains its near monopoly, the implication of the analysis is that Russia should raise the domestic prices of natural gas to full long run marginal costs, i.e., to approximately double present prices. We estimate that this would result in benefits to Russia of about $1.24 billion dollars per year. The analysis suggests however that it is not in Russia’s interest to introduce unified pricing of natural gas. If Gazprom2 were to sell its natural gas to Europe at its full long run marginal cost plus transportation costs, Gazprom would lose between $5 billion and $7.5 billion per year. However, in the first instance consumers in Europe would gain between $7.5 billion and $10 billion per 1 Russia maintains, moreover, that, as long as no specific industries are targeted for price discrimination, WTO rules do not prohibit it from charging different prices to domestic and foreign consumers (Inside U.S. Trade, April 26, 2002, p. 1). 2 Gazprom has a monopoly, or is close to one, in the production, transmission and distribution of natural gas in Russia. We discuss below our estimates of the government of Russia’s taxes of Gazprom in 2003 and the mechanisms available to increase the taxes on Gazprom as a result of an increase in domestic prices; but the government’s ability to tax Gazprom must be tempered by the need encourage investment for development of natural gas production capacity. 2 year because they could consume more gas at cheaper prices, partly from switching from other energy sources and partly from using more gas with existing technology. Unified pricing would therefore either transfer between $5 and $7.5 billion dollars annually from Gazprom to its gas customers in Europe and Turkey, or else impose very large costs on the Russian economy with few if any benefits. By clearly identifying the stakes involved -- who gains and who loses -- this analysis attempts to inform the discussion of this important economic policy topic. II. WTO Legal Issues—Is the Demand WTO-Plus? The Russian negotiators have noted that Article 2 of the WTO Agreement on Subsidies and Countervailing Measures states that to be considered a subsidy, the subsidy has to be specific to an enterprise or group of enterprises. For example, Russia's earlier system of pricing energy at lower prices to the fertilizer industry would be a subsidy to the fertilizer industry (that system was eliminated). However, since the price in Russia for energy products does not vary with the user, Russian negotiators argue that dual energy pricing does not meet the criteria for a subsidy under WTO rules. The following hypothetical example illustrates why the demand came to be labeled by the Russian negotiators as WTO-Plus, i.e. as a demand going beyond accession requirements. If fertilizer producers elsewhere believe that dual energy pricing is a subsidy to Russian fertilizer exporters, they are permitted to initiate a countervailing duty investigation against Russian fertilizer exporters. Then, if Russia were a member of the WTO, it would have the right to appeal any such decision by another WTO member country to a WTO Dispute Settlement Panel. The Dispute Settlement Panel would resolve the matter according to WTO rules. Thus, if dual pricing were a subsidy under WTO rules, there would be no need to require its elimination as part of the accession negotiation since it would be possible to apply countervailing duties against Russian exports. On the other hand, if dual energy pricing is not a subsidy, then the Dispute Settlement Panel will rule in favor of Russia and the countervailing duty margins will be declared illegal. Not withstanding these legal considerations, we focus on the economic aspects of dual energy pricing in this paper. III. The Economics of Dual Pricing of Natural Gas From Russia’s perspective, domestic prices of natural gas should be raised, but there is no rationale for unified pricing between gas sold domestically and exported gas. We believe that the Russian market would be better served if Russia were to introduce competition in production of natural gas along with the provision of pipeline access for new gas suppliers. Gazprom, however, is presently close to a monopoly in Russia’s 3 domestic market. Efficient pricing of monopolies requires that they price in the domestic market at levels that reflect the true alternate economic value of the commodity in question.3 We explain below that in Russia’s domestic market this corresponds to the long run marginal costs of natural gas. This implies that it will be necessary for Russia to raise the domestic price of natural gas to achieve this economically efficient price; otherwise the capital stock will deteriorate and supplies will not be forthcoming over time. Many market economies, in fact, regulate the maximum price of monopolies such as gas and electricity distribution to achieve this pricing objective.4 Russia has a market share of approximately 27 percent of natural gas sales in Europe, which implies Gazprom has some market power.5 In this situation, it is optimal for Gazprom to price above long run marginal cost to exploit this market power, i.e., it is optimal for Gazprom to sell natural gas in its export market at a price higher than in its domestic market.6 We now explain these conclusions. Russia’s Reserves and Exports. Russia is endowed with very significant natural gas resources. Its proved reserves of 47.6 trillion cubic meters represent over 30% of the world’s proved reserves. 7 Its 2001 production of 542 billion cubic meters (BCM) constituted 22% of world production and its reserves to production ratio is in excess of 80 years, higher than any other major producer. Russia is also by far the world’s largest exporter of natural gas. In 2001, it exported about 127 BCM to Europe and Turkey and about 40 BCM to CIS countries and the Baltics.8 Optimal Export Prices It is in Russia’s interest to try to maximize the overall revenues associated with export volumes. Given the need to ship natural gas from Russia to Europe through a pipeline, Gazprom is able to “segment” the European market from the Russian market. Given the significant role it plays in supplying the European market, Gazprom does have 3 This discussion is based on the current structure of the natural gas market in Russia. Of course, production of natural gas is not a natural monopoly and it would therefore be desirable to have additional producers. We discuss below that if alternate producers of natural gas were given access to the gas pipelines, there would be economic gains as well as environmental benefits. Nothing in the argument developed in this paper implies that the current structure of Russia’s gas market is efficient. 4 See, Scherer (1980, chapter 18) and Carlton and Perloff (2000, chapter 20). 5 In the year 2000, Russia was responsible for 66% of the imports of Europe (including Turkey). The other principal suppliers of gas to the European market are Algeria (through a pipeline across the Mediterranean), Norway, the Netherlands and the UK. See British Petroleum (2000). 6 If in the future, competition is introduced in the Russian market, competition among Russian firms would erode monopoly profits in Europe. In effect, unified pricing would be achieved through structural reform of the Russian market, rather than by regulation. In the absence of the Gazprom monopoly, if Russia is to extract the available monopoly profits on its exports of gas to Europe, it will be in Russia’s interest to impose export taxes on Russian gas exporters. 7 The source for the data in this paragraph is British Petroleum (2001). 8 Exports to Europe and Turkey include about 75 BCM to Western Europe, 40 BCM to Eastern Europe and 11 BCM to Turkey. 4 market power.9 The extent of the market power, however, is tempered by the existence of competing sources of gas. In addition, Gazprom wants to benefit from being perceived as a reliable supplier that can be trusted to continue to deliver gas (potentially in increasing quantities) at a fair price to European markets. In the long run, Gazprom faces risks that new competitors will erode its market share and those risks are greater the higher its markup over marginal costs.10 Volumes for the next several years are constrained by transportation facilities and long-term contracts. This limitation, of course, can be overcome and new entrants are likely to emerge. However, the longer-term constraint is the absorptive capacity of export markets. Russia’s proven reserves are sufficient to support a doubling, or even tripling, of its production capacity. In order to absorb this volume of gas, markets in Europe would have to increase dramatically. The key point here is that Gazprom cannot sell significantly more natural gas in Europe without impacting the price of gas there. To sell significantly more gas, Gazprom would have to accept a lower price, i.e., it faces a downward sloping demand curve. This means that there is no “world price” of gas that Russia faces. Rather, Gazprom must calculate an optimal price for its gas sales in Europe that reflects the tradeoff it faces between the additional revenue from additional sales of gas and the lost revenue from the reduction of price if it has to lower its price to sell additional gas. Gazprom’s optimal price of gas in Europe will have to change over time as the demand for gas in Europe changes, but it is in Gazprom’s interest to maximize its profits on exports. In the appendix we derive the optimal pricing formula for Gazprom’s exports of natural gas to Europe. At present, Russian gas is priced in three distinct tiers: Europe, Russia and the Commonwealth of Independent States (CIS). In Europe, given the large up front investments required for gas pipeline infrastructure, Russia, Algeria and Norway all secured long-term contracts. As a result of long standing competition with other fuels, formulae for the price of gas in these long-term contracts are linked to fuel alternatives primarily oil. However, given the competition, it appears reasonable to assume that Gazprom negotiated the best price it could in these long-term contracts. The European gas market is growing, but upper limits on piped gas prices will continue to be defined for some time by competition from alternative fuels (including Liquefied Natural Gas, LNG). 9 Based on data in the Europe market, in appendix 1 we present our calculations of the Lerner index of market power. We find that it is significant in comparison with estimates of the Lerner index for other industries. 10 Since higher prices will accelerate the entry of new competitors, optimal dynamic pricing by Gazprom would result in a lower price to deter entry. See Gaskins (1971) for a derivation of the optimal dynamic pricing rules for a dominant firm facing the threat of entry from a competitive fringe. If in the future, supplies from new competitors increase faster than demand from Europe, the markup by Gazprom would fall. Moreover, elasticities of demand are greater in the long run than in the short run, since, for example, inter-fuel substitution is possible in the long run. Greater elasticities imply less market power and lower the optimal markup over marginal costs. We presume, however, that Gazprom has optimized its markup based on long run calculations. 5 The table below indicates the prices at the German border (at Waidhaus) for Russian gas over the 1999-2001 period. It also indicates the transportation costs for shipping gas from the Russian border to the German border and the price received by Gazprom net of (or after subtracting) the transportation costs. The latter price is called the netback price. Hypothetically, a $22/barrel crude oil price would result in a price at the Russian border of approximately $85/TCM. Table 1: European Border Gas Prices in dollars per Thousand Cubic Meters ($/TCM) 1999 2000 2001 German Border Price 70.95 105.90 126.37 Transportation Cost (26.90) (26.90) (26.90) Russian Border Netback Value 43.05 79.00 99.47 Source: Estimates by Gas Strategies of EconoMatters Ltd. for the World Bank Pipelines segment the CIS market from the markets of Europe and of Russia. In the CIS, prices are discounted relative to the price for gas sold into Europe. In 2000, the average netback value of the gas sold in the CIS and Baltic States was about $35/TCM. As a price discriminating monopolist or oligopolist in segmented markers, Gazprom would maximize profits in the CIS by charging a price where marginal revenue equals marginal cost. Clearly, the CIS 7 countries have considerably less income and ability to pay the prices the Europeans pay for natural gas. Given this lower income and demand, the optimal price in the CIS markets will be much lower than the price Gazprom charges in Europe. It is never profit maximizing to price less than marginal cost. However, at $35/TCM, prices in the CIS are at about Gazprom’s own estimate of the price it needs to cover full costs. Further explanations for the prices in the CIS are that prices are well above short run marginal costs, which allows Gazprom to make a short-term profit on these sales, without necessarily intending to meet this demand in the long run. In fact, Gazprom has allowed gas company Itera access to its transmission system to supply the CIS market with gas from Turkmenistan, suggesting no long-run commitment to this market. Sales to the CIS countries are also subject to bilateral negotiation that may reflect non-price considerations. Optimal Domestic Prices Prices in the domestic market are regulated and, while tariffs have been increased quite substantially over the last couple of years, prices are still only in the range of $15 to $20/TCM. Our analysis indicates that prices in the domestic market should be increased for both industrial and consumer uses of natural gas to about $40/TCM, but not raised higher. 6 The optimal price for domestic natural gas is the long run marginal cost (LRMC), where the LRMC includes environmental costs in addition to the full cost of doing business. This is a well- established principle of efficient market pricing.11 Many market economies regulate the prices of their monopolies with more or less this pricing objective. Application of the LRMC pricing rule is straightforward for industries with constant average costs. For natural monopolies with decreasing costs throughout, long run marginal cost pricing will result in losses for the monopolist. There are several solutions for the regulator that ensure average cost pricing. These include government subsidies of the losses, price discrimination, two part tariffs, or, quite commonly, average cost pricing. In addition, consumers (including industrial users) would have to pay VAT and applicable excise taxes, and these taxes would apply on top of this price.12 If the domestic price of natural gas is set above LRMC, there will be inefficiency from monopoly constriction of output. If the price is below LRMC the product will not be efficiently used and production levels will decline from lack of investment. In the case of Russia, prices of energy products have been priced below LRMC for a long time, which has led to an excessively energy intensive structure of industry and inadequate investment for production and distribution. Not withstanding the need to raise domestic energy prices, given that Russia is a cold climate country, a well-targeted safety net for poor consumers is needed to prevent severe hardship. LRMC is the efficient price for Gazprom, independent of proposals under consideration by the Russian government to tax energy to diversify the economy. A first crucial step in encouraging diversification away from energy intensive products would be to raise the price of energy to the LRMC. If the government wishes to encourage further diversification, it has available the VAT or other taxes that apply on top of the price received by Gazprom; but the domestic price excluding taxes has to cover LRMC. Despite the acknowledged corporate governance problems of Gazprom, Russia will obtain about $6.2 billion in calendar year 2003 from taxing Gazprom, which is about 9% of the planned federal budget.13 The principal taxes levied on Gazprom are the following: (1) an excise tax levied at the rate of 15% on the wholesale price for domestic sales and sales to the CIS and 30% on other exports based on the price at the Russian border; (2) a mineral extraction tax of 16.5% of the “wellhead” value of the gas (the price where the gas enters the pipeline); (3) an export tariff levied at the rate of 5% on the customs value of the exported gas; and (4) a corporate profits tax of 24%. Out of the $6.2 billion in forecasted taxes, only about $0.3 billion are estimated to come from the 11 See Scherer (1980) or Carlton and Perloff (2000). Due to the lack of competition, final user prices and pipeline tariffs are regulated. If, as we recommend, competition is introduced in the Russian gas market, final user prices for consumers not dependent on local distribution monopolies will no longer have to be regulated. Rather competition will result in prices moving toward LRMC of production and transmission. In part because of this, key trading partners of Russia are now placing the emphasis on competition in the production of Russian gas and nondiscriminatory access to the pipelines, with a secondary concern about prices. 13 World Bank estimate. This $6.2billion was forecast under Russian government assumptions of $21.50 per barrel for Urals crude oil. 12 7 corporate profits tax, reflecting that Gazprom, as presently structured and under present pricing policies, is not a very profitable corporation. An increase in the domestic price of natural gas to LRMC should increase the profits of Gazprom, since it will avoid losses on its domestic sales, while it will still earn profits on its sales in the European market. As a result of the existing taxes, the government will automatically increase its tax take from Gazprom (most clearly from the 15% excise tax on domestic sales and the corporate profits tax). The existing tax structure offers several ways to further increase the government’s tax take on Gazprom. An export tax, for example, would not raise domestic gas prices above the efficient price of LRMC, whereas an excise tax would affect domestic prices. Any increase in taxation, however, would have to be weighed against the need to carry out the necessary investments.14 Exhaustible resource models argue for a “depletion cost” to be added to the appropriate LRMC. But the depletion premium is inversely related to the size of the reserves. Since more than 80 years of reserves remain and there are prospects for new discoveries, the depletion premium would be close to zero in the case of Russia.15 The appropriate long run marginal cost for Russia to consider in this calculation is therefore composed of the production and distribution costs for sales in Russia. Environmental costs and taxes should also be incorporated in any appropriate LRMC as part of an economy-wide effort to address environmental concerns, including global warming effects from fossil fuels. But the environmental costs of natural gas production are low relative to alternate fossil fuels, so the taxes would be relatively lower.16 One pollution issue related to natural gas results from the flaring of gas that is produced in association with oil. Gas flaring is a significant problem in Russia that results, in part, from Gazprom's reluctance to provide access to pipeline facilities to competing sources of gas production. Gazprom's gas is all non-associated and does not involve any gas flaring. Russian oil producers are now attempting to gain access to the pipeline network to try to secure some monetary return on gas that is now being flared as well as to open up opportunities for the development of non-associated gas reserves. Provision of such access to Russian oil producers should provide both economic and environmental gains to Russia. The volume of associated gas that could enter the market, however, is relatively small -- perhaps 20 BCM out of total production of 580 BCM. Associated gas is a low cost source of gas and it would produce an environmental benefit. 14 Domestic gas price increases would have widespread impacts on the budget, not all positive. For example the government may collect less profits tax due to decreased profits of sectors that use gas and an increase in expenditures on housing subsidies and purchases of gas by governmental entities. The World Bank and the Ministry of Finance of the Russian Federation are presently working on assessments of the fiscal implications of changes in the relative price of energy. 15 Moreover, empirical research has cast doubt on whether a depletion cost should be added to the LRMC, since it has shown that real prices of exhaustible resources (or the value of a unit of the remaining resource) have not persistently increased over the past 125 years. The empirical evidence has shown that new discoveries and technological progress have significantly mitigated the effects of finite availability of nonrenewable resources on their scarcity for production and consumption activities. See Krautkraemer (1998) for a summary of this literature. 16 Although all fossil fuels contribute to global warming, natural gas is far more environmentally friendly than the fuels it typically displaces e.g. lignite, coal and residual fuel oil (mazut). 8 Since Russia has a large share of the Western European market for natural gas, it does not face a “world price” at which it can sell all it would like. Incremental volumes of gas production cannot be assumed to generate additional export revenues, because to sell significant incremental volumes of gas production, Gazprom has to lower the export price.17 It is in Gazprom’s interest to set the price and quantity of its sales of gas on export markets such that it maximizes profits. When the optimal price and quantity on export markets has been set, the opportunity cost of selling additional gas in the domestic market will be zero. Similarly, any reduction in domestic consumption will not translate into additional exports since the optimal export level is predetermined. Instead, a reduction in domestic consumption will translate into reduced production – in effect, additional gas will be left in the ground. We estimate that the LRMC for natural gas is in the range of $35 to $40/TCM (see the Box below). Estimates of LRMC are subject to a margin of error, but this estimate is consistent with Gazprom’s own estimate that a domestic price equivalent to $35/TCM is required if existing production levels are to be maintained. With 2003 prices in the $15 to $20/TCM range, prices are too low to encourage the investment required to maintain and develop the necessary natural gas infrastructure network. In recent years there has been insufficient investment to maintain and develop gas producing capacity levels.18 On the other hand and equally important, low energy prices encourage inefficient and energy intensive modes of industrial production. The infrastructure of industrial production facilities is excessively geared toward energy use relative to other inputs; the relative price of energy does not properly reflect the costs to society of producing energy. It is important that decisions to invest in industrial production facilities be based on energy that is not priced below efficient levels. Prices of energy will inevitably have to rise to reflect the cost of gas production or else supply shortages will appear. Then industrial production investments based on low and inefficiently priced energy will become unprofitable. Moreover, the government of Russia has the intention to diversify the economy away from energy products. Inefficiently low priced energy products discourage efficient diversification of the economy away from energy products and products that are intensive in their use of energy. If Russia would like to create employment in sectors of the economy that are not energy dependent and diversify the exports of the economy away from energy intensive exports, a crucial first step that it can take is to raise the domestic price of energy to LRMC. If, hypothetically, Russia faced a “world price” for gas and could sell all it wanted at this given price, then the world price would equal the opportunity cost to Russia of selling gas domestically. In this case, the world price would equal the dollars that Russia would be giving up on export sales by selling domestically. Then, the appropriate long run marginal cost of the gas for Russia would be the world price, independent of the production costs in Russia. 18 According to World Bank staff estimates, without an additional $5-$6 billion annually in capital expenditures over the next few years (above the estimated $3.3 billion invested in 2002), gas production in Russia will decline by about 40 BCM per year (or about 7% of current production per year). 17 9 Table 2. Estimated Long Run Marginal Cost for Russian Natural Gas Three components make up the calculation of the undiscounted long run marginal cost of natural gas: 1. Upstream development costs. Given the existing proven reserves, no exploration component is required. Development costs are estimated in the range of $7 to $9/TCM 2. Transmission costs. The major gas fields, including the yet to be developed Yamal field, are located over 2,000 kilometers away from major domestic markets. The long run marginal cost associated with trunk transmission gas lines is estimated at about $1/TCM per 100 kilometers. 3. Distribution costs. These are estimated in the range of $5 to $10/TCM. The total undiscounted cost may be summarized as follows: $/TCM 8 22 5 -10 35 – 40 Development cost Transmission Cost Distribution Cost Undiscounted LRMC Source: World Bank staff estimates. Based on our estimates of LRMC, it would be efficient for Russia to raise domestic prices to about $35-$40/TCM, but not higher. At present rates of consumption (about 375 BCM) increasing domestic prices by about $20/TCM would increase the overall cost to consumers by about $7.5 billion per year with unchanged quantities. Consumption of natural gas (for both intermediate and consumer use), however, would be reduced and more efficiently allocated. The amount of the decline in Russian consumption of natural gas depends on the elasticity of demand. Based on the assumption of a market elasticity of –0.5, this would generate a welfare gain to the economy of $1.24 billion per year. Consumption would decline by about 124 BCM relative to the level without a change in the gas price. (See the appendix, especially figure 1, for the details of the calculation.) Implications of Alternatives For Gazprom to supply Europe at its LRMC level, i.e., to apply uniform prices, it would have to reduce the prices it charges its European clients by about $50/TCM ($39 in 2000 and $59 in 2001). This would translate into a reduction of between $5 and $7.5 billion per year in the economic rent that Gazprom is able to extract from its gas sector on 10 its export market. From Russia’s perspective, this would be economically very inefficient. At the same time, European consumers would, potentially, receive a benefit of between $7.5 and $10 billion from a reduction in the cost of the energy they consume, i.e., European consumers would gain about $2.5 billion per year more than Russia would lose.19 European consumers would receive the benefit of paying $5 to $7.5 billion less per year on their present purchases, plus the lower gas prices would allow them to expand consumption. (See appendix B for the details of the calculations). Given that Europeans lose more dollars than Russia gains from dual pricing, a natural question is whether there is a cooperative solution that makes both Europe and Russia better off. A cooperative solution would involve Russia selling gas to Europe at LRMC plus transportation costs and Russia receiving compensation in return. Such compensation could take the form of any aspect of the relationship between European countries and Russia, and need not be tied directly to gas prices. But for such an arrangement to be in Russia’s interest, the compensation would have to be substantial, valued by Russia at not less than $5 to $ 7.5 billion per year. Alternatively, one can pose the question noncooperatively: can Gazprom develop a pricing strategy that would allow it to increase its profits? Monopolists often employ “two-part tariffs” as a method to extract the maximum profits.20 If European buyers were offered gas at a lower per unit usage price, but had to pay a fee to access the gas each year, this would be in effect, a two part tariff. For Gazprom, the optimal two part tariff requires pricing gas at LRMC plus transportation costs, and charging an access fee equal to the entire value of the gas to European consumers above LRMC plus transportation costs (the entire consumers’ surplus). In principle, Gazprom’s profits could increase by not only the $2.5 billion in inefficiency losses from prices exceeding marginal costs in Europe, but by an additional $4.8 billion due the additional value it can extract from consumers with high demand (the triangle DD’J in the figure). Gazprom’s failure to maximize short run profits through optimum two-part tariffs, likely reflects its perceived risks of losing profits in the long run to substitutes. Presently gas prices in Europe are based on a formula linked to oil. In principle, that formula could be adjusted when long-term contracts are renegotiated. We estimate in the appendix that profits could potentially double for Gazprom, if it could implement optimal Despite the fact that Europeans lose more than Gazprom gains from Gazprom’s pricing in Europe, an evaluation of global welfare requires a relative valuation of a marginal dollar of income in Russia versus Europe. Development aid implicitly values a dollar of income in rich countries (like most European countries) less highly than a dollar of income in a poor country (like Russia). If, in this world welfare calculation, the weight on Russian income were greater than 4/3 and were equal to unity on European income, then the transfer of income due to Gazprom’s natural gas pricing in Europe, where Europe gives up $10 billion and Russia receives $7.5 billion, would increase world welfare. 19 20 Oi (1971) has showm that a monopolist will maximize profits if it charges a lump sum fee equal to the consumer’s surplus and a per unit price equal to marginal costs. Such arrangements are common in industries such as telecommunications (fixed fee for a hookup plus charges for actual calls), the rate structures of electricity utilities (block discounts), rental of mainframe comptures and copying machines and country club fees and numerous other examples. See Ramirez and Rosellon (2002) for a discussion in the context of natural gas pricing in Mexico and Sherman and Visscher (1982) and Phlips (1981) for discussions of the other indusdries mentioned. 11 two part tariffs, but this would require combined access fees of about $12 to $15 billion per year. Thus, although a cooperative solution potentially allows a maximum of $2.5 billion additional profits for Gazprom, optimal noncooperative two part tariffs could yield $7.2 billion additional profits for Gazprom. Despite the fact that optimal two part tariffs would involve a larger transfer of dollars to Gazprom than the present pricing arrangements or a cooperative solution, two part tariffs would be efficient in the sense that world welfare would be maximized in dollar terms. But, as mentioned above, the greater the short run extraction of profits by Gazprom, the greater the risks that its market position will be eroded by new competitors in the long run. Conversely, if Russian domestic prices were to be raised to export parity levels, the price in Russia would have to be quadrupled from less than $20 TCM to almost $80 TCM. The additional costs of this gas would amount to $22 billion per year--equivalent to about 6% of GDP. This price level would force a dramatic contraction in the use of natural gas in Russia. Given its cold climate, poor consumers would have to be protected from such dramatic price increases.21 Russian industry would be faced with a number of options: (i) shifting to other almost certainly less environmentally friendly energy sources and/or producing alternate outputs that are not intensive in the use of natural gas; (ii) absorbing these very large cost increases with consequent impact on reinvestment potential; or (iii) going out of business. None of these are attractive or efficient outcomes. In a situation where prices were unified, there is the probability that Russia would also seek to increase prices for gas sold to the CIS countries to European levels. This would have a significant adverse impact on several of the poorest CIS countries – notably, Armenia, Azerbaijan, Georgia and Moldova – and would create additional payment problems for these countries. The impact of unified energy pricing, as far as it means raising domestic prices in Russia, would likely be negative for the poor CIS countries. IV. Conclusion Gazprom has monopoly power domestically and some market power in export markets. We believe that the Russian market would be better served on both economic and environmental grounds if Russia were to introduce competition in production of natural gas along with nondiscriminatory access to pipelines for new gas suppliers.22 In the near term, however, Gazprom is a monopoly in the Russian domestic market and there is an offsetting consumer interest that suggests that appropriate government policy should prevent Gazprom from exploiting its monopoly power by limiting its price to 21 WTO negotiators have not required that gas prices be raised to residential consumers. Different prices to different users would induce consumption distortions and thus appear ill advised. But, ignoring efficiency costs of price discrimination within Russia, it will be difficult to prevent gas price increases to industry from being transmitted to consumers. For example, electric utility users would have to pass on the price of gas increases to their residential consumers. 22 With competition among Russian firms, Russia would need to apply export taxes on exporters of gas to Europe in order to extract profits on these sales and exploit the market power of Russia as a whole. 12 LRMC. On the export market there is no offsetting consumer interest to Russia that would suggest why Russia should fail to exploit its market power. Unified pricing, if it means lowering export prices of energy, will result in a loss of export revenue of between $5 and $7.5 billion. If it means raising domestic prices to current export prices, it will result in a significant and inefficient restriction of output in Russia and would likely have an adverse knock on effect on other countries in the CIS that currently enjoy preferential pricing arrangements for gas supplied by Russia. Western European consumers would receive the benefit of paying $5 to $7.5 billion less per year less on their present purchases if Gazprom were to lower its export price. In the first instance, they could gain an additional $2.5 billion from the fact that the lower gas prices would allow to switch to more gas consumption. Thus, unified pricing would be expensive to Russia, while implying that European incomes would rise by more than Russia loses. For Russia to lower prices in this manner would require very substantial compensation, but could potentially improve world welfare. Alternately, world welfare could be improved and the efficient world price could be achieved in the European market if Gazprom priced its gas through a two part tariff (that is, lower the cost per TCM but charge high fees for the right to buy any gas). We estimate that the optimal two part tariff would double the profits of Gazprom in Europe. The fact that Gazprom does not employ a two part tariff in Europe implies that it is pricing its gas in Europe at prices considerably less than the pure short run profit maximizing price. This, likely derives from a long run view in which Gazprom must consider the risks of losing its market. 13 References Al-Sahlawi, Mohammed A. (1989), “The Demand for Natural Gas: A Survey of Price and Income Elasticities,” Energy Journal, 10 (1), January, 77-90. Beierlin, J., J. Dunn and J. McConnor, Jr. (1981), “The Demand for Electricity and Natural Gas in the Northeastern United States,” Review of Economics and Statistics, 64, 403-408. British Petroleum (2000; 2001), Statistical Review of World Petroleum, 2000, 2001. Available at: www.bp.com/centres/energy2002/ Bresnahan, Timothy (1989), « Studies of Industries with Market Power, » in Richard Sshmalansee and Robert Willig (eds.), The Handbook of Industrial Organization, Amsterdam: North-Holland. Carlton, Denis and Jeffrey Perloff (2000), Modern Industrial Organization, 3rd edition, Harper Collins. Chaudhary. Mohammad Ali et al. (1999), “Industrial Sector Input Demand Responsiveness and Policy Interventions,” Pakistan Development Review, 38 (4), Winter, 1083-1099. Estrada, Javier and Ole Fugleberg (1989), “Price Elasticities of Natural Gas Demand in France and West Germany,” Energy Journal, 10 (3), 77-90. Gaskins, Darius (1971), “Dynamic Limit Pricing: Optimal Pricing under Threat of Entry,” Journal of Economic Theory 3, September, 306-322. Hsing, Yu (1992), Interstate Differences in Price and Income Elasticities: The Case of Natural Gas, Review of Regional Studies, 22 (3), Winter: 251-59 Inside US Trade, April 26, 2002. Joskow, P. and M. Baughman (1976), The Future of the U.S. Nuclear Energy Industry,” Bell Journal of Economics, 7 (Spring), 3-32. Krautkraemer, Jeffrey (1998), “Nonrenewable Resource Cost,” Journal of Economic Literature, 36, December, 2065-2107. Liu, Ben-Chieh (1983), “Natural Gas Price Elasticities: Variations by Region and by Sector in the USA,” Energy Economics 10 (3), 195-201. Oi, Walter (1971), “A Disneyland Dilemma: Two-Part Tariffs for a Mickey Mouse Monopoly” Quarterly Journal of Economics, 85 (1), February: 77-96 Phlips, Louis (1981), The Economics of Price Discrimination, Cambridge: Cambridge University Press. Ramirez, Juan C. and Juan Rosellon (2002), “Pricing Natural Gas Distribution in Mexico,” Energy Economics, 24(3), May: 231-248. Scherer, F.M. (1980), Industrial Market Structure and Economic Performance, Chicago: Rand McNally Sherman, Roger and MichaelVisscher (1982), “Rate-of-Return Regulation and Two-Part Tariffs,” Quarterly Journal of Economics, 97(1), February: 27-42. Taylor, L.D. (1977), “The Demand for Energy: A Survey of Price and Income Elasticities,” in E.D. Nordhaus (ed.) , International Studies of the Demand for Energy, Amsterdam: North Holland. 14 APPENDIX A Derivation of the Optimal Pricing of Russian Natural Gas in Europe and in Russia by Gazprom Model We assume that the market for Russian natural gas is segmented between Russia and Europe. We assume Gazprom acts as a monopoly in Russia but faces rival oligopolistic competitors in the Europe market. Define the following notation: P Q p qE qi qR c t = = = = = = = Price in Russia Quantity in Russia price in Europe total quantity in Europe quantity supplied in Europe by supplier i quantity supplied in Europe by Russia costs of producing natural gas in Russia (assumed constant) = transport costs of natural gas from Russia to Europe (assumed constant) Then profits for Gazprom are: (1) P(Q)Q cQ p(qE )qR (c t )qR Assume that Gazprom and its rivals in the Europe market compete as noncooperative Cournot oligopolists. (A cooperative equilibrium would imply a markup over marginal costs that is higher than derived below with a noncooperative equilibrium.) Then the optimum prices and quantities in the two markets for Gazprom are obtained by solving (2) and (3): (2) P' (Q)Q P(Q) c 0 Q q (3) p' (q E ) E q R p(q E ) (c t ) 0 q R q R q E q Since under the Cournot assumption o i R, we have that E 1 . Then (2) and q R q R (3) may be written as: dP Q (4) P(Q) c dQ dp qR (5) p (q E ) (c t ) dq E Multiply the right hand side of (4) by P/P and divide both sides by P to obtain: 15 P(Q ) c 1 p (Q ) R where R = market elasticity of demand in Russia. (6) Equation (6) states that the optimal percentage markup over marginal costs that Gazprom desires is equal to the inverse of the market demand elasticity in Russia. This is the wellknown Lerner market power measure. For the Europe market, multiply the right hand side of (5) by pqE / pqE and divide both sides by p, then p ( q E ) (c t ) dp q E q R s (7) p(q E ) dq E p q E E dq p q market elasticity of demand in Europe and s R the market where E E dp q E qE share of Gazprom in Europe. Define the perceived elasticity of demand by Gazprom in the Europe market as P . Then: p q R dp q E q R dp q E q R s 1/ p q R p dq E q R p dq E p q E E Thus, the right hand side of (7) is the absolute value of the inverse of the perceived elasticity of demand by Gazprom in the Europe market. Analogous to the monopoly condition in Russia, the optimum markup of price over marginal costs for Gazprom in Europe is equal to the inverse of its perceived elasticity of demand, where marginal costs includes transportation costs. It is evident from equation (7) that the optimal markup of Gazprom in the European market increases with the market share s and decreases as the absolute value of market elasticity of demand increases. The optimal price also increases as marginal costs c, or transportation costs t increase. The optimal price quantity combination is depicted in Figure 1. The Russian market is depicted to the right of the origin. The Europe market is to the left of the origin, where the quantity increases further to the left. In Europe, perceived marginal revenue equals marginal production plus transportation costs at point E, where Gazprom sells 126 billion cubic meters of natural gas. At this quantity, the market clears at point D, where price equaled $106 per thousand cubic meters (TCM) in 2000. Lerner Index of Market Power Using data available in the text, or figure 1, we calculate the Lerner index of market power in Europe; that is, we estimate equation (7); note that a perfectly competitive market would yield a value of zero for equation (7). 16 . Using LRMC, the Lerner index equals 0.37 based on prices in 2000 or 0.47 based on prices in 2001. With short run marginal costs (about $20 per TCM) the Lerner index would rise to 0.56 or 0.63, depending on the year. So the Lerner index for Gazprom in Europe ranges from 0.37 to 0.63, depending on the year or the measure of marginal costs. Bresnahan (1989, table 17.1) has surveyed the estimates in the literature of the Lerner index of market power in many industries. Bresnahan notes that the literature has focused on (U.S.) industries with high concentration ratios, that is, industries where we expect to find significant market power. There are several industries in which the Lerner index is higher than the value for Gazprom in Europe (e.g., tabacco, 0.65; aluminum between the two world wars, 0.59; banks before deregulation, 0.21-0.88). But most of the studies of market power in industries had estimates of market power lower than our measure for Gazprom in Europe (e.g., coffee roasting, 0.025-0.05; rubber, 0.05; textiles, 0.07; electrical machinery, 0.2; railroads, 0.4; retail gasoline, 0.1; automobiles, 0.1-0.34; banks after deregulation, 0.16-0.4). Thus, despite the fact that the sample of industries selected for study are those where the authors expected to find significant market power, our estimate for Gazprom is among those the estimates with a large amount of market power. 17 Appendix B Implied Welfare and (Relative) Quantity Effects of Changes in Russian Natural Gas Prices Welfare and Relative Quantity Effects of Natural Gas Pricing in Russia “Relative” Decline in Natural Gas Consumption in Russia. A crucial determinant of the demand for natural gas in Russia over time is the aggregate income of Russia. As the economy grows, Russia can be expected to increase its demand for natural gas in accordance with its income elasticity of demand for natural gas. The demand for natural gas is also responsive to price. In the analysis below, we focus on the price effects and estimate the impact of increases in the price of natural gas, and hold other variables like the income of Russia constant. In other words, the analysis employs the standard comparative static “ceterus paribus” assumption of economic analysis to evaluate the impact of a policy change. It is not a forecast of the change in demand for natural gas. One would expect that even with the price increases implied below, with enough time, the growth in Russian GDP will dominate the price impacts and the quantity demanded of natural gas will increase over time. With that understanding, we estimate the impact on the change quantity demanded and welfare as a result of price changes in Russia induced by pricing policies. To simplify the discussion, we refer to quantities and prices as of 2001, and measure changes in quantity demanded relative to the quantity demand in 2001, but actual quantities in the future will differ due to growth in demand and other factors. Price Elasticity of Demand for Natural Gas. The amount of the decline in Russian consumption of natural gas following a price decrease depends on the elasticity of demand. There have been estimates of the price and income elasticities of demand for natural gas by various authors, including Joskow and Baughman (1976) for 48 U.S. States, Beierlin, Dunn and McConnor (1981) for nine U.S. states, Estrada and Fugleberg (1989) for France and West Germany, Hsing (1992) for the states in the United States, Liu (1983) for regions and sectors of the United States, and Chaudry (1999) for Pakistan. These estimates and others have been surveyed by Al-Sahlawi (1989) and earlier by Taylor (1977). Regarding the price elasticities of demand, the studies typically find that short run price elasticities are inelastic but the long run elasticities are elastic. From the survey of Al-Sahlawi (1989, tables 1 and 2), the various studies of short run price elasticities of demand range from –0.07 to –0.63, with a modal estimate of about –0.25. Long run price elasticities of demand range from –0.56 to –4.6, with a modal estimate of about –2.3. In the analysis below, we shall assume a value for the price elasticity of demand in Russia of –0.5. This is in between a short and long run price elasticity. The larger the elasticity estimate, the larger the welfare effects from a price increase. From a long run 18 perspective, a value of –0.5 for the price estimate, clearly underestimates the welfare loss from price unification. Increase in the Price in Russia to LRMC. If the price of natural gas were increased to the LRMC (that is, from $20 to $40 per TCM), consumption of natural gas would be more efficiently allocated and would decline compared to the current level of 375 BCM. If we assume a market elasticity of –0.5, consumption would decline to 251 BCM. This would generate a welfare gain to the economy of $1.24 billion per year. Details of the calculations are as follows: P Q P *Q . Rearranging yields: Q R P P Q P $20 / TCM ; P $30 / TCM (at the midpoint) ; Q 375 BCM . 2 Q R * (375 BCM ) 3 If R 0.5, then Q 124 BCM . The elasticity of demand in Russia is R The welfare gain is equal to the value of the triangle AAB in figure 1. This is 0.5 * Q P 0.5 * (124 BCM ) * ($20 / TCM ) $1.24 billion. Increase in the Price in Russia to Export Parity Levels. If on the other hand, the price in Russia were increased to export parity levels, the price in Russia would have to increase to between $(106 – 27)= $79 per TCM and $(126 – 27) = $99 per TCM (data are from table 1). Given that the present price is less than $20 per TCM, this means that the price would have to at least a quadruple and the price increase would be at least $59 per TCM. At unchanged quantities, the increase in the cost of natural gas in Russia would be: $59 per TCM * 375 BCM = $22.1 billion The quantity demanded at these higher prices would depend on the elasticity of demand for natural gas in Russia. To estimate the implied decrease in natural gas consumption in Russia, suppose that the price increase is “only” $59 per TCM. Then the change in quantity would be as follows: 19 P Q P *Q . Rearranging yields: Q R P P Q P $59 / TCM ; P $39.5 / TCM (at the midpoint) ; Q 375 BCM . The elasticity of demand in Russia is R Q R *1.5 * (375 BCM ) If R 0.5, then Q 280 BCM . Then the new quantity demanded in Russia would be 95 BCM. That is, Russian quantity demanded would fall to roughly 25% of the original quantity demanded. For constant elasticity demand curves with elasticities greater than 0.65 in absolute value, we estimate that this price increase would induce a fall in the quantity demanded to zero. Thus demand must be rather inelastic in order for any significant natural gas market to remain in Russia following a price increase of this magnitude. Most likely, the elasticity is sufficiently small for key buyers that there would be some demand even at high prices, but this shows that the contraction in demand and shrinkage in production would be very large for Russia. The implication is that there would be very large adjustment costs for Russia from this policy. These adjustments would be inefficient since they are not based on comparative advantage. Welfare Economics for Russia in the Europe Market If Gazprom lowers the export price in the Europe market to LRMC plus transport costs, the new equilibrium is at point F in figure 1. At point F, Russia will earn zero rents, since price equals costs at this price-quantity combination. At the higher prices in Europe, however, Gazprom earns rents equal to the rectangle DD’E’E. Thus, the loss to Gazprom is the value of this rectangle. (It can be equivalently measured by the triangle EFG.) Note that the estimated loss to Gazprom from moving to marginal cost pricing in the Europe market is independent of the elasticity of demand. The losses are simply the rents Gazprom earns on its prior sales in Europe. Depending on prices in year 2000 or 2001, the price reduction is $39 per TCM or $59 per TCM. Then the value of the losses to Gazprom are between $5 billion and $7.5 billion per year. (126 BCM * $39/TCM = $5 billion) or (126 BCM * $59/TCM = $7.5 billion). Welfare Economics for Europe in the Europe Market If Gazprom lowers the export price in the Europe market to LRMC plus transport costs, the new equilibrium is at point F. European consumers would receive the benefit of paying $5 to $7.5 billion less per year less on their present purchases (the rectangle DD’E’E). In addition, at the lower natural gas prices, European consumers can expand consumption of Russian gas until price exceeds the lower marginal cost. Thus, they would also receive the benefit of the resource allocation gain equal to the triangle DEF. The Europeans obtain a rent transfer from Russia plus a triangle of resource allocation benefits. 20 The value of the triangle DEF depends on the perceived elasticity of demand of Gazprom. Since it is natural to assume that Gazprom optimizes on its sales in Europe, it follows that it charges a price where the perceived elasticity of demand exceeds unity in absolute value. (Otherwise marginal revenue is negative, i.e., it is operating in the portion of the demand curve to the left of point H, and it can increase profits by reducing sales.) We assume the elasticity is –1.5 in this calculation and we take a price decline of $50 per TCM, an average of the implied price decline in 2000 and 2001. Recall that the perceived elasticity of demand is the market elasticity of demand times the share of Gazprom in the European market, i.e., in absolute value the perceived elasticity is larger than the market elasticity of demand by a multiple of about (10/3). We calculate the value of the triangle as follows: The perceived elasticity of demand is: q p P E R . p R q E The quantity change, implied by a $50 price reduction is: p R q E P qE pR $50 126 BCM 103 BCM $92 where $92/TCM is the price midpoint. 1.5 * Then the value of the triangle DEF is: 0.5 * (103 BCM ) * $50 / TCM $2.6 billion. The gain to consumers in Europe is the sum of the rectangle DD’E’E plus the triangle DEF. This value is between $7.5 billion an $10 billion per year. Net Welfare Change in the Europe Market Since Europe gains the rectangle DD’E’E plus the triangle DEF, while Russia loses the rectangle DD’E’E, there is a net welfare gain equal to the triangle DEF associated with uniform pricing. This is a familiar triangle of distortion costs from monopoly pricing. Thus, Europe gains $2.5 billion per year more than Russia loses. Full Potential Value of Consumers surplus in European Market The full potential value of consumers surplus to Gazprom (potentially extractable through a two part tariff) includes the rectangle DD’EE’ (between $5 and $7.5 billion) plus the triangle DEF ($2.6 billion) plus the triangle DD’J. To calculate the value of the triangle above DD’J, we must estimate the price at which the demand curve intersects the vertical 21 axis. In the triangle DD’J, the quantity change is equal to the negative of the initial equilibrium quantity of 126 BCM. Thus, q E q E 126 BCM The initial price is $116 TCM, if we take the midpoint of the prices in 2000 and 2001. The change in price implied by the quantity change to zero, with a liner demand curve with perceived elasticity –1.5 is therefore: p R p R q E p $116 PR * $77 TCM P 1.5 qE Then the value of the triangle DD’J is: 0.5 * (126 BCM ) * $77 / TCM $4.8 billion. Consequently, the optimal two part tariff from Gazprom would extract between $12.2 and 14.7 billion [=(5-7.5) + 2.6 + 4.8] billion (DD’EE’+ DEF + DD’J). This is approximately double the rents that Gazprom extracts on their sales from the single price based on usage. 22 Figure 1: Optimal Pricing of Russian Natural Gas in Europe and in Russia $ per thousand cubic meters J PERCEIVED DEMAND IN EUROPE LRMC + TRANSPORT COSTS $106 D D' F $67 E DEMAND IN RUSSIA E' C LRMC LRMC B' PERCEIVED MARGINAL REVENUE IN EUROPE A' B $40 A $20 H G 126 billion cubic meters 0 Q Q* 375 billion cubic meters MR = Marginal Revenue in Russia MR Optimum in Europe Market. We assume Gazprom maximizes profits on the quantity of natural gas sales in Europe. This occurs at point E, where perceived marginal revenue equals marginal production plus transportation costs. At this quantity (126 billion cubic meters), the market clearing price is at point D ($106 per thousand cubic meters). For quantities greater than at point E, marginal revenue is less than marginal production plus transportation costs. Thus, expansion of sales to the point F, where the price ($67) equals marginal production plus transportation costs, will result in losses on Russia’s exports (relative to point D) equal to the value of the shaded triangle (EFG) (which is equal to the rectangle DD'E'E). For quantities greater than point H, additional sales will reduce the revenues received, and additional costs are also incurred. Russia Market Gazprom faces a controlled price at $20 per thousand cubic meters, leading to quantity demanded (and sold) of 375 billion cubic meters of sales in Russia. The social optimum for Russia is at point B where long run marginal cost equals price at $40. An increase in the price in Russia from $20 to $40 results in an increase in welfare in Russia equal to the triangle AA’B. Gazprom would maximize profits where marginal revenue equals marginal costs, leading to point C. Since the value to Russia exceeds the marginal costs of production for quantities less than at Q*, there is a triangle of losses equal to BB’C for an increase in the price resulting in a movement from B to C.