Spring 2005 Exam #3

advertisement

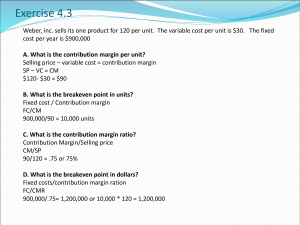

Cost Accounting Exam #3, Spring 2005 Name_____________________________ 1. At the breakeven point, fixed cost is always: A) Less than the contribution margin. B) Equal to the contribution margin. C) More than the contribution margin. D) More than the variable cost. 2. Calculating the margin of safety measure will help a firm answer which of the following questions? A) Will we break even? B) Are we using our debt wisely? C) How much will profits change if sales change? D) How much profit will we earn? E) How much sales can we lose before we drop below the breakeven point? 3. High operating leverage is a measure of the risk of change in profit a firm assumes when it has: A) high variable cost. B) high fixed cost. C) high sales. D) high turnover. E) high expectations. 4. The CVP model assumes that over the relevant range of activity: A) only revenues are linear. B) revenues and fixed costs are linear. C) revenues and variable costs are linear. D) revenues and total costs are linear. E) None of the above answers is correct. 5. The difference between unit sales price and unit variable cost is the: A) unit contribution margin. B) total contribution margin. C) contribution margin ratio. D) margin of safety. E) breakeven point. 6. The unit contribution margin multiplied by the number of units sold is the: A) segment margin. B) total contribution margin. C) contribution margin ratio. D) margin of safety. E) breakeven point. 7. Cost/volume/profit analysis is a technique available to management to understand better the interrelationships of several factors that affect a firm's profit. As with many such techniques, the accountant oversimplifies the real world by making assumptions. Which of the following is not a common assumption underlying CVP analysis? A) All costs incurred by a firm can be separated into their fixed and variable components. B) The product selling price per unit is constant at all volume levels. C) Operating efficiency and employee productivity are constant at all volume levels. D) The variable cost per unit varies over the relevant range of activity. E) Costs vary only with changes in volume. 1 Cost Accounting Exam #3, Spring 2005 8. A cost is not relevant if it: A) does not differ for each option available to the decision maker. B) changes from period to period. C) is a future cost. D) is not time-valued. E) is a fixed cost. 9. Fixed costs will often be irrelevant because they: A) are fixed in amount. B) are the same each time period. C) typically do not differ between options. D) are not committed. E) All of the above answers are correct. 10. Operating at or near full capacity will require a firm considering a special order to recognize the: A) opportunity cost arising from lost sales. B) value of full employment. C) time value of money. D) need for good management. E) value of saying "No." 11. Done on a regular basis, relevant cost pricing in special order decisions can erode normal pricing policies and lead to: A) overconfidence. B) a loss in the firm's profitability. C) conflicting personnel goals. D) instability. E) maximization of resources. 12. A useful device for solving production problems involving multiple products and limited resources is: A) gross sales per unit of product. B) contribution per unit of scarce resource. C) net profit per unit of product. D) total expense. E) total benefit. 13. When using relevant cost analysis, it is a common mistake for untrained managers to include in their analysis: A) sunk costs. B) allocated fixed costs. C) "unitized" fixed costs. D) All of the above are correct. 2 Cost Accounting Exam #3, Spring 2005 Problem 1 Due to the lazy economy (and lazy people) the Bi-Wheels Company has experienced some difficulty in selling its bicycles. The following data relates to 2004: Sales (9,000 units @ $100) Less variable costs (9,000 @ $60) Contribution margin Less fixed costs Net loss $900,000 540,000 $360,000 400,000 ($40,000 ) Required: 1. Compute Bi-Wheels' breakeven point in both units and dollars. Also, compute the contribution margin ratio. 2. The manager believes that a $40,000 increase in advertising would result in a $120,000 increase in annual sales. If the manager is right, what will be the effect on the company's net income or loss? 3. Refer to the original data. The vice-president in charge of sales is certain that a 10% reduction in price in combination with a $30,000 increase in advertising will cause unit sales to increases by 50%. What effect would this strategy have on net income (loss)? 3 Cost Accounting Exam #3, Spring 2005 Problem 2 Oehler’s Hightech Company recently developed the technology necessary to produce a low, medium and high end computer memory chip for heart monitoring healthcare equipment. Budgeted fixed costs for the manufacture of all three products total $4,250,000. The budgeted sales by product and in total for the coming year are as follows: Sales Variable costs Contribution Economy Amount Percent Standard Amount Percent $1,750,000 $1,207,500 $542,500 $4,000,000 $1,000,000 $3,000,000 100% 69% 31% 100% 25% 75% High Amount Percent $2,500,000 $1,250,000 $1,250,000 100% 50% 50% Actual sales for the year were not as planned; the following lists sales by product: Economy Standard High $4,000,000 $2,250,000 $2,000,000 $8,250,000 Required 1. What are the breakeven sales if only the Standard product is sold? 2. What are the breakeven sales if only the Economy product is sold? 3. What are the breakeven sales if the product mix was as budgeted? 4. What would be the breakeven sales based on the actual sales mix? 5. The company president knows that total actual sales were $8,250,000 for the year, the same as budgeted. Because he had seen the budgeted income statement, he as expecting a nice profit from producing the memory chips. Explain to him what happened. 4 Cost Accounting Exam #3, Spring 2005 Problem 3 Galbraith Chocolate Factory makes three types chocolate candies; Lizzy’s, Stacy’s, and Marrisy’s. The three candies are manufactured on a common assembly line, which is limited to 1,000 machine-hours per week. Unit selling prices and costs for three product lines are as follows: Selling price per pound Direct materials Direct labor ($15.00/hr.) Variable Overhead Fixed overhead Machines minutes to produce one pound of chocolate Lizzy’s $35.00 10.00 8.00 4.00 5.00 Stacy’s $45.00 12.00 12.00 6.00 5.00 Marrisy’s $60.00 12.00 20.00 10.00 9.00 5 minutes 5 minutes 9 minutes Variable overhead is charged to products on the basis of direct labor dollars, fixed overhead is charged to products on the basis of machine hours. Total fixed costs are $200,000. REQUIRED: 1. If Galbraith Chocolate Factory has excess machine capacity and can add more labor as needed (neither machine capacity nor labor is a constraint), which product (or products) should Galbraith prefer to sell if the customer is buying 100 pounds of chocolate. 2. If Galbraith Chocolate Factory has excess machine capacity and can add more labor as needed (neither machine capacity nor labor is a constraint), which product (or products) should Galbraith prefer to sell if the customer is buying $10,000 of chocolate? 3. Due to an unexpectedly high demand for Galbraith’s chocolates, they can sell all the chocolate they can produce. If Galbraith Chocolate Factory has excess labor time but a limited amount of machine capacity, the production capacity should be devoted to producing which product or products? 4. Due to an unexpectedly high demand for Galbraith’s chocolates, they can sell all the chocolate they can produce. However, if Galbraith decides to produce a minimum of 1,000 pounds of each product, how many pounds of each product should be produced? 5. BONUS: What is the opportunity cost of producing a minimum of 1,000 pounds of each product (requirement 4), rather than producing the product (or products) that will maximize short-run profits? 5 Cost Accounting Exam #3, Spring 2005 Problem 4 Plainfield Company manufactures part G for use in its production cycle. The costs per unit for 10,000 units of part G are as follows: Direct materials Direct labor Variable overhead Fixed overhead $3 15 6 8 32 Verona Company has offered to sell Plainfield 10,000 units of part G for $30 per unit. If Plainfield accepts Verona's offer, the released facilities could be used to generate $40,000 in additional contribution margin. In addition, $50,000 of the fixed overhead applied to part G would be totally eliminated. Required: 1. Assuming the productions needs of 10,000 units is known with certainty, which alternative is more desirable and by what amount? 2. BONUS: Assuming the production needs are not know, at what volume would Plainfield Company be indifferent between buying part G for $30 per unit or continuing to manufacture the part? 6