Supplementary Guidance on Interest Rate Notification (4.4)

advertisement

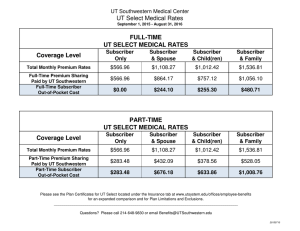

")

AMENDMENTS TO THE GUIDANCE ON SECTION 4.4 OF THE BANKING CODE, PUBLISHED 6 JULY 2006 Changes in interest rates 4.4 We will keep you informed of changes in the interest rates on your accounts and will tell you about the ways we will do this. The requirement to “keep you informed of changes in the interest rates on your accounts” will be fulfilled by either: telling customers personally within thirty days of the change (subject to the provisions for Savings Accounts below); or within three working days of the change, putting notices of our new rates in our branches, on our website and in the newspapers we usually use. To help customers compare rates more easily, our newspaper notices will show clearly the old and new rates. Interest Variations on Savings Accounts If a customer has a variable-rate savings account including a fixed rate account that has become variable after the fixed rate has expired (including accounts that are no longer available) with £500 or more in it and the interest rate falls by more than 0.25 percentage points on a rate change compared with the Bank of England base rate (a ‘relevant rate change’), a subscriber will personally notify the customer within a reasonable period of time. The effective date for the £500 cut-off should be the same across the account range. It relates to a point–in-time balance, not an average balance. The £500 limit is a cost-benefit measure that takes account of the cost of personal notification to customers. Bonuses and tiers Bonuses offered for a fixed period of time, to either new or existing customers, should not be considered when deciding whether there has been a relevant rate change. This is subject to the caveat that the terms of the bonus must be clearly communicated to customers. There will be a relevant rate change on accounts, with more than one tier of interest rates where there has been a relevant rate change on any one of the tiers. Relevant rate change The interest rate on a variable rate account is considered to have fallen relative to Base Rate in each of the following four circumstances when the interest rate; 1 is reduced by more than the reduction in Base Rate; is increased by less than the increase in Base Rate; has been decreased but there has been no reduction in Base Rate; has not been increased following an increase in Base Rate. This requirement applies irrespective of the channel for delivery of the account e.g. branch, postal, telephone, Internet etc. Where it is necessary to contact customers after a relevant rate change, this should be in an appropriate form (e.g. letter, statement, e-mail etc), and not be subordinate to other material e.g. marketing messages. Reasonable period Subscribers have up to 30 days1, from a change in Base Rate to make a decision regarding the interest payable on accounts. The ‘reasonable period’ of time for subscribers to notify customers of a relevant rate change should not be more than 30 days from the date the subscriber’s decision is made about the interest rate that would trigger a relevant rate change notification. It would not be ‘reasonable’ for a subscriber routinely to implement reductions almost immediately in relation to Base Rate reductions and delay for nearly 30 days increases following rises in Base Rate. Exceptions where the Interest Variations on Savings Accounts requirements do not apply are: current accounts, and transactional accounts (inc. accounts with the usual current account features, except a personal cheque book); if the interest rate tier relates to balances below the minimum operating balance for the account and the minimum balance requirements have been communicated clearly to the customer (e.g. in terms and conditions); or the customer has been told that the interest rate payable to them will be fixed or nominal (i.e. 0.5 per cent or less) whilst their balance remains below the minimum balance requirement for the account or at the level of a low-balance tier to which a fixed or nominal rate applies; or tracker accounts or fixed rate accounts [Guidance continues as currently drafted from the top of page 19 onwards of the printed Guidance for Subscribers] This may be extended to take account of the decision of the following month’s meeting of the Monetary Policy Committee, provided any personal notification is sent within 60 days of the change in the Base Rate 1 2