CP ACCOUNTING

Introduction to Accounting

PERFORMANCE OBJECTIVES

1.

2.

3.

4.

Define accounting.

Explain the importance of accounting information.

Describe the various career opportunities in accounting.

Define ethics.

KEY POINTS

1. Accounting is the language of business.

2. The study of accounting gives a person the necessary background and understanding of the scope,

functions, and policies of an organization.

3. Ethics, as it relates to accounting, is the way keepers of financial information conduct the business of

accounting according to laws of the state and their own personal system of morality.

Introduction to Accounting Vocabulary (page 10):

Accountant

Accounting

Economic Unit

Ethics

Financial Accounting Standards Board

(FASB)

Generally Accepted Accounting

Principles (GAAP)

International Accounting Standards Board

(IASB)

International Financial Reporting

Standards (IFRS)

Paraprofessional Accountants

Sarbanes-Oxley Act

Securities & Exchange Commission

(SEC)

Transaction

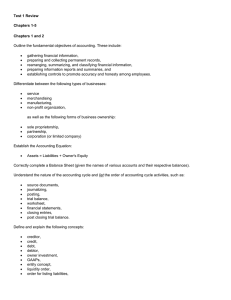

Chapter 1: Asset, Liability, Owner’s Equity, Revenue and Expense Accounts

PERFORMANCE OBJECTIVES

1. Define and identify asset, liability and owner’s equity accounts.

2. Record, in column form, a group of business transactions involving changes in assets, liabilities and

owner’s equity.

3. Define and identify revenue and expense accounts.

4. Record, in column form, a group of business transactions involving all five elements of the fundamental

accounting equation.

Introduction to Accounting/Chapter 1

olivo

CP ACCOUNTING

KEY POINTS

1. There are five classifications of accounts: assets, liabilities, owner’s equity, revenue and expenses.

2. After each transaction has been recorded, the total of one side of the fundamental accounting

equation must equal the total of the other side.

Chapter 1 Vocabulary (page 36)

Account Numbers

Accounts

Accounts Payable

Accounts Receivable

Assets

Business Entity

Capital

Chart of Accounts

Creditor

Double-entry Accounting

olivo

Equity

Expenses

Fair Market Value

Fundamental Accounting Equation

Liabilities

Owner’s Equity

Revenues

Separate Entity Concept

Sole Proprietorship

Withdrawal

04/10/13

0

0