Offshoring and Transfer of Intellectual Property

U n d e r v a l l u e d I I n t t e l l l l e c t t u a l l P r o p e r t t y i i n O f f f f s s h o r i i n g

Gio Wiederhold

Computer Science Department

Gates Computer Science Bldg. 4A, room 436

Stanford University, Stanford CA 94305-9040

Tel: 1-650 725-8363; Fax: 1-650 725-2588

Email: wiederhold@cs.stanford.edu

Amar Gupta

Eller College of Management, University of Arizona

McClelland Hall, Room 202ETucson, AZ 85721 USA

Tel. 1-520-626-9842, Fax. 1-520-621-8105

Email: agupta@arizona.edu

David Branson Smith

Eller College of Management, University of Arizona

Tucson, AZ 85719 USA

Tel: 1-520-275-6111

Email: Smith.DavidBranson@gmail.com

September 24, 2008

Executive Summary

1

Businesses engaging in outsourcing of professional service activities to organizations in foreign countries have focused primarily on the issues of cost and the number of jobs affected, with less consideration of the issue of transfer of intellectual property (IP) that frequently accompanies such offshoring arrangements. We show that the importance of such IP is significant and important to understand risks of loss, obligations of taxation, and above all, its contribution to the profit-making potential of an enterprise. The IP involved in an offshore transfer should be valued according to the type of transfer transaction that is being considered. More specifically we focus on software, an important and often poorly valued component of such transfers.

The value of real and intangible assets to a business sense is due to these assets driving the profitability of a company. We do not provide here a legal view, nor an accounting view of value, but focus on business-oriented issues. While the importance of intangibles in knowledge-oriented businesses is well established, legal and accounting definitions have not kept pace. For instance, the book value of a company as presented formally virtually ignores IP, and hence provides little quantitative guidance to the stockholders who are concerned about the future profitability of the enterprise.

Transfers of IP occurs in some form in nearly every service-based offshoring arrangement, and as relationships with offshore entities grow, new IP is transferred is transferred in both directions: from the entity sponsoring the work to the entity performing the work, and vice versa. Such transfers have significant long-term effects on the balance of IP generation versus IP consumption. More complex scenarios are common: the IP is transferred to a third, hosting, locale, and users of the IP pay royalties for the use of that IP.

After a general introduction that directs the focus to the need to value IP, and technologybases IP in particular we introduce methods that can be used for valuing such IP.

Multiple competing valuation methodologies are highlighted.

The specific discussion addresses a commonly offshored service – software development

– as a proxy for many types of IP, focusing on some of the special attributes of software that makes it difficult to value. It presents the factors that determine software IP valuation, as well as the relationships of IP residing in software to the business models used for outsourcing.

Given that information , we the revisit the issue, why so many companies involved in the creation and use of software are unaware of the value they are exporting.

The value of the IP associated with these transfers should therefore be calculated just as in the case of any other long-term project– based on the future usefulness and the income-generating ability. However, the value of transferred IP that is rarely ascertained, especially in cases of intra-company transfers, due to:

1.

Confusing regulations and multiple legal jurisdictions with disparate objectives governing the offshoring of professional service activities;

2.

Underdeveloped/ambiguous IP valuation techniques promulgated by regulation;

3.

Nascent tax regulations governing professional service and IP transfer pricing; and

2

4.

Offshoring being traditionally perceived as a transfer of labor rather than as a transfer of IP

The cumulative effect of these factors is potentially unreliable estimates of the cost and risks of outsourcing. Since the amount of IP that is transferred abroad is large, its value should play a significant role in decisions related to offshoring. This problem is exacerbated with offshoring becoming a viable option for smaller companies and with the proliferation of global sourcing

1

.

This article explores a commonly offshored service – software development – as a proxy for many types of IP, focusing on some of the special attributes of software that makes it difficult to value. It presents the factors that determine software IP valuation, as well as the relationships of IP residing in software to the business models used for outsourcing.

Multiple competing valuation methodologies are highlighted.

1 Smith, H.A. and McKeen, J.D. (2006) “IT in 2010: The Next Frontier” Management Information Systems

Quarterly Executive (MISQE) , Vol. 5, No. 3, Sep. 2006.

3

Overview:

Intellectual Property In Modern Enterprises

Technology-Based IP – Software

Computing the Value of Software

Principles of IP Valuation

Assigning Value to Software

Valuation Methods

Post-Offshoring Diminution of Software Value

Diminution of Software IP Value in Offshoring Arrangements

Measuring Diminution

Basic Software Value Considerations

When is Software Property?

Why are IP Values Currently Underestimated?

Why Should Companies Consider IP Value?

Types of Intellectual Property Inherent to Offshoring Arrangements

Relationship between Offshoring and Software Transfer

Contracted Operations

Owned Operations

Location of the IP

Government Interest in Software Valuation: Taxation of IP Flows

Conclusions

Intellectual Property in Modern Enterprises

Intangibles of a business are all assets that are neither physical nor financial objects 2 . In modern, knowledge–based enterprises these intangibles are the primary business drivers.

Owners and stockholders recognize this fact. In 1982, intangibles contributed about 40% of firms’ value, but by 2002, 75% of the market value of all US firms is attributable directly to intangibles, while tangible assets accounted for only the remaining 25%

3

. Just like tangibles, intangibles must be continuously maintained and renewed, but at a rate that is roughly twice the rate of tangible assets

4

. Understanding, and hence management of intangibles is hindered by the lack of consistent metrics and the complexity of the paths from intangibles to profitability.

Intangibles are considered Intellectual Property (IP) when they are owned in some sense.

An important intangible that is excluded from IP assessments is the general knowledge that workers possess, but enterprise knowledge that is covered by Non-Disclosure

2 Lev, Baruch (2001): Intangibles – Management, Measurement, and Reporting; Brookings Institution

Press, Washington, D.C.

3 Kamiyama, S., Sheehan, J, and Martinez, C. (2006). “Valuation and Exploitation of Intellectual Property.”

STI Working Paper 2006/5. Statistical Analysis of Science, Technology and Industry. http://www.oecd.org/sti/working-papers

4 Nadiri, Ishaq M. and Ingmar R. Prucha: “Estimation of the Depreciation Rate of Physical and R&D

Capital in the U.S. Total Manufacturing Sector”; Economic Inquiry, Vol. XXXIV, January 1996, 43-56..

4

Agreements (NDAs) can be considered IP. Innovative results of employees work should increase the IP of a business. That IP becomes a mechanism for capturing market share, increasing revenue margins, and a bargaining chip for access to complementary technologies – which in turn supports the first two objectives

5

. IP is also leveraged in acquiring financing for new ventures. Strategic IP management – the ability to exploit a company’s IP to its fullest extent – is becoming increasingly important. Since IP is easy to replicate and transfer it must be protected. IP that covered by patents and copyright is at identifiable and easier to manage, but then also visible to competitors. To keep IP away from prying eyes, business and process documentation, as well as software is protected as trade secrets. Unless an obligation to publish code exists, trade secret protection is common for code. Open-source software is excluded from our definition of

IP, but its integration and exploitation within larger systems can add considerable value.

IP can be exploited by transfer to new settings, open up new international markets, and leveraged by its use in low labor cost countries

3.

Without transfer of IP many offshoring 6 projects would not be feasible; even a simple service project as a call center derives its value to a large extent to the IP that that is being provided 7 . In more complex arrangements, say cross-border development and licensing of software the need to manage a company’s IP becomes crucial. In those cases concerns about allocation, security, and taxation abound.

While offshoring of jobs now permeates the economies of developing countries, but the effect of providing IP created originally by offshoring sponsors to offshore service companies may greatly exceed the effect of job transfers to those offshore service companies 8.

However, IP can flow to any place where profits can be accumulated. If royalties for the use of IP are paid to the locales where the IP resides from the locales where the IP is used to create products, then issues become more complex. Preventing loss of IP must focus on the country where it IP is being used, but the eventual loss of profits is felt in the country where the IP formally resides. We expand on that issue later. For our discussion, the difference between nearshoring and global offshoring is of little concern, since the protection of IP remains a concern as soon as the IP has moved from the sponsor to sites where laws, regulations, taxation, and attitudes concerning intellectual property differ. The operational benefits of being close remain valuable.

As smaller companies gain access to offshoring practices, and as communications technology makes offshoring attractive for complex projects in large companies, IP is being transferred across borders more often than ever before in history. The issues surrounding IP are thus becoming a broader concern to business decision makers.

Recently, nearly 60% of companies stated that their primary criterion when opting to

5 Kaplan, R. S. and D. P. Norton (2004), Strategy Maps: Converting Intangible Assets into Tangible

Outcomes , Harvard Business School Press, Boston, Mass.

6 A good model that describes the different varieties of outsourcing is found in; Cronin, Bruce et al. 2004.

“Outsourcing and Offshoring.” CESifo Forum . Summer. 5(2). 17-21.

7 Walden, E. A. (2005). “Intellectual Property Rights and Cannibalization in Information Technology

Outsourcing Contracts”; MIS Quarterly , Volume 29 Number 4, December 2005, 699-720.

8 Economist (2007, February 2). Places in the Sun. The Economist .

5

forego outsourcing arrangements was related to IP issues; half of those companies stated that greater assurance of IP security would fundamentally alter their decision

9

.

Why Assign Value to IP?

While the overriding reason for being able to assign a value to corporate intellectual property is the need to understand one’s business in quantitative terms, there are also specific situations where valuations of IP are required. Assigning a value to IP is crucial when setting prices for IP, when determining royalty rates for shared IP, to obtain financing, and when attempting to optimize use and maintenance of IP to the firm’s utmost advantage. When offshoring, and thus exposing IP to an increased risk, the potential of loss cannot be quantified unless a value is attached to the IP being transferred. If the offshore entity operates at arms-length, then a transfer price must be established as well, since such a transfer is regarded as an export

10

. Figure 1 indicates the participants, the similarities, and the distinctions when exporting tangible versus intangible property.

Figure 1: Distinctions when exporting tangible versus intangible property

Companies are not the only organizations concerned with IP valuation; governments in many countries are losing billions of dollars of taxes due to inadequate transfer pricing estimates in offshore parent-subsidiary relationships. Pricing audits, based on the approval of new U.S.

Treasury transfer pricing regulations for services and IP, oblige business decision makers to properly value IP

11

.

The role of Technology-Based IP

For accounting purposes, the Financial Accounting Standards Board (FASB) defines technology-based IP as patented technology, trade secrets, databases, mask works, software, and unpatented technology. By focusing on technology we ignore the value of the reputation of a company, its general trademarks, and the management contribution, in part because these elements are even harder to allocate than technology that is being

9 Studt, T. (2007). “R&D Outsourcing Becomes More Strategic” R&D magazine, June 2007, pp.26-29, www.rdmag.com

10 Rosenberg, Joel B. Barbara N. McLennan: “Technology, Licensing, and Economic Issues in Transfer pricing”; Chapter B in Robert Feinschreiber: Transfer Pricing Handbook , 3rd edition; Transfer Pricing

Consortium, John Wiley Publishers, 2002 supplement.

11 Martinson, O.B., Englebrecht, T.D., and Mitchell, C. (1999). "How multinational firms can profit from sophisticated transfer pricing strategies"; Journal of Corporate Accounting & Finance , Vol. 10, No. 2, pp.

91-103.

6

transferred. We also ignore the value of existing customer loyalty. If the sales rights to foreign territories are included in an offshoring transfer customer loyalty can add significant value, which can be estimated from regional sales data.

Overall, despite massive levels of investment in software and information technology

(IT) assets, alignment of technology assets with business functions remains a notoriously difficult task

12

. The ubiquitous use of software IP and the extent to which it drives the profits of many of today’s corporations notwithstanding, the value-generating capabilities of software and other intangibles are easily overlooked, and attention is focused on expensing and thus minimizing these items

13

.

When the return-on-investment is used as a metric, the reduction of spending generating benefits on IP investments (the denominator) is easier to calculate than the benefits generated by IP investments (the numerator)

14

. The reason for this mismatch is that U.S. accounting regulations disallow the capitalization of costs related to internally-developed intangible assets, allowing only for capitalization of certain development costs related to software to be marketed. This effectively expenses any and all costs attributable to software to be used in house, and allows for the capitalization of the costs attributable to marketable software only during the period of time between when that software is deemed ’technologically feasible’ (i.e., the nature of the costs having moved from being purely research to development of a process for which a new product can be feasibly produced) and the release of the concerned software product to customers. The term

“technological feasibility” is ambiguous and depends on management’s philosophy and judgment. Therefore, it is relatively easy for maximization of expensing of software development costs to occur, contributing to the inability to view software as a valuecreating asset 15 .

Technology-Based IP in offshoring

While many types of IP are transferred across country borders in offshoring arrangements we focus now on technology-based IP. Since software is essentially codified knowledge, much technology-based IP falls within the broad definition of software. Examples for immediate use are: user guides; proprietary binary software for use in the host operation, embedded databases, documentation on problem resolution based on prior experience, trademark registration and patents for embedded concepts. If the software is to be the basis for further development more material is required: design specifications, source codes, process descriptions guiding further development; and instructions transmitted under confidence that provide an understanding not obvious from primary material. If the host also resells the products in the foreign geographical area, then the rights to use established trademarks, literature that describes the products for the customers, business

12 Kohli, R. and Devaraj, S. (2004) “Realizing the Business Value of Information Technology Investments:

An Organizational Process”; Management Information Systems Quarterly Executive (MISQE), Vol. 3, No.

1, March, 2004.

13 Kwan Yuk, P. and Stafford, P. (2007). “Study Urges IT Valuation Rethink”; The Financial Times , Nov.

4, 2007. Obtained from FT.com.

14 Peppard, J. and Daniel, E. (2007) “Managing the Realization of Business Benefits from IT Investments”

Management Information Systems Quarterly Executive (MISQE) ; Vol. 6, No. 1, March, 2007.

15 While an important discussion in its own right, this aspect of software IP will not be focused on here; the following paper accurately summarizes this accounting convention: Mulford, C. and Roberts, J. (2006).

“Capitalization of Software Development Costs: A Survey of Accounting Practices in the Software

Industry,” May, 2006.

7

methods that make sales of the product effective, and instructions on exploiting these business methods are all part of the software.

Offshored software IP is commonly used in applications such as: call centers, offshored production or operational settings, software maintenance

16

, software adaptation to international standards, software localization to specific languages and regions, software creation, and web services.

The contribution of software to IP

The role of IP is to generate income at a level that exceeds reimbursement from labor expended, use of commodity products, and the margins expected in routine business operations. Computer software can generate profit by being replicated and sold as products to external parties, and by leveraging internal business processes. Product software comprises operating systems, compilers, database systems, common desktop productivity tools, applications for creative artists, games, and a myriad of other applications. Internal-use software can be used to design products, manage inventory and supply chains, handle finances and payroll, support provide sales and call centers, and provide feedback from the field to correct and improve products

17

. Companies that develop and market software or products that embody software to external customers see the effects of their investment in IP directly, but it is hard to find an enterprise that does not have some proprietary items of software IP.

Principles of IP Valuation

Valuation is the process of establishing a fair price for a good or service. When tangible goods are transferred to a host for their use, a price for the good is usually already established, leading both parties and regulators to know about what value is being transferred. For software, off-the-shelf marketable packages have similar characteristics.

But a master software disk, containing software to be replicated, cannot be valued by a unit price. Its value will largely depend on the future sales of its contents. The contents represents IP to be valued.

Intangibles must be valued by its contribution to the income of a business. More specifically, the value of IP is estimated by a forecast of income from its future use. If a product has a marketing history, it ongoing sales in a foreign region can be estimated.

This applies to direct sales of software as well as to the software that is embedded in so many of our seemingly tangible products.

For internal use software the income from business operations has to be allocated to the software versus other costs of doing business. Assuming optimal allocation of software versus personnel resources the allocation of income can be made based on long-term expense ratios. (ref for a pareto argument)

16 Basili, V. (1990). Viewing Maintenance as Reuse-Oriented Software Development. IEEE Software, 7(1),

19-25.

17 Thornton, E.A. (2002). “Valuation of Software Intangible Assets.” ASA International Conference . San

Diego, CA. August.

8

Assigning Value to Software

Software can be used in two distinct ways: as a saleable product, the income generated from which depends on the sales or leasing (licensing) revenue; or, as an internal-use item, the benefits from which are derived from improved business processes (and are thus harder to directly measure).

To be fair, the valuation of software IP remains difficult and subjective. Software is easy to reproduce at a cost that is negligible; each incremental sale garners much more profit than is commensurate with the incremental cost of production. The value of IP is therefore very independent of any cost or effort expended to create it. Case in point: while a thousand lines of code that generate a report that nobody reads have little value, a few brilliant lines of code can drive most of the profitability of a company. Due to the difference in value that can be assigned to software, a distinction between which entity owns what part of an item of software IP in an offshoring arrangement must be made, and the value to each firm must be considered independent of the value of the finished product and of the benefit to each location. In situations involving IFCs, cannibalization

(reuse for contracts with different clients) of software IP can occur, and value can diminish for clients of a particular vendor; these clients would have benefited more had the IP been used specifically in their favor 18 . CFCs, on the other hand, have well defined marketing domains, typically mandated in geographic terms and therefore lessen the risk of separate assignment of value amongst a large number of firms or of IP cannibalization.

Additionally, any changes that occur in the case of CFCs are easily identified if the client and vendor are owned by the same parent. The value of such IP is generally determined when it is consumed, i.e., used to generate income

19

.

For a marketable software supplier employing the use of a CFC, some of the ongoing costs will be incurred at the sponsor site and some at the host. To compute the required cost-sharing payments for alternatives 2 and 3 of Figure 1, all the research and development costs applicable to the creation of the software are aggregated and then allocated according to revenues in the home and CFC geographical areas. Any costs exceeding the revenue apportionment are then reimbursed from the other side. This arrangement becomes complex when IP has been contributed by multiple entities, since

IP is also generated by brand and product marketing, which will have different life spans than those of the technological components. No amount of marketing can overcome poor quality, so we focus here solely on the software component.

Aside from marketable software, many businesses depend on internally generated software that is created in house or made to order by a vendor. The value of IP cannot be based upon its development cost, forcing companies to estimate income for valuation purposes. Due to the nature of software and its ubiquitous effect on many or all of the supporting processes of a company, and since contributions to income also derive from

18 Walden, E. A. (2005). “Intellectual Property Rights and Cannibalization in Information Technology

Outsourcing Contracts” MIS Quarterly , Volume 29 Number 4, December 2005, 699-720.

19 Smith, G., & Parr, R. (2000). Valuation of Intellectual Property and Intangible Assets (3rd ed.). Wiley.

9

investments in creative people and machinery, only a portion of a company's income can be attributed to internal use software. Howerver, income attributable to software can be fairly assigned based on the assumption that the management of a company is rational in the allocation of its resources

20

. If such optimality is assumed, corporate net income created by diverse expenses can be allocated according to the proportion of costs incurred. The fraction spent on software from year to year will vary, but such variations even out over the life of the software.

Valuation Methods

Multiple IP valuation methods are available to practitioners. Of the methods listed below

(which represent only a fraction of the total number of methods available), one or more may be most appropriate for a given situation, and must be chosen given the facts and circumstances applicable to each case. In addition to the methods listed below, IT-based

IP performance can be conceptualized as being measured in terms of ‘for efficiency’ or

‘for knowledge management’, each of which have different payoffs and thus suggest different valuation techniques

21 . Listed below are some of the ‘best practice’ techniques that may be employed:

Assessment of Future Income: The determination of future income requires estimating the income accruing to the IP in each of all future years over its useful life, i.e., the amount sold and the net income per unit after routine sales costs are deducted. The estimation of the IP value of software requires estimates of the current sale price, future version frequencies, maintenance cost expectations, and sales volumes over its life. If the

IP is used internally, then the savings accrued by owning the IP can be similarly estimated. Within this ‘income method’, a variety of inputs and calculation differences exist, allowing it to adapt to many intangible assets that can stand alone and generate cash flows. Assets such as brand name, which provide value to an entire product line, however, remain difficult to segregate and value independently. Usually, the future income profile of truly novel software is uncertain, and hard to quantify

22

. While the future market is hard to assess for novel products, it works well for mature, established ones. Since all forecasts are discounted to net present value, less mature products will be subject to a higher discount rate than products or internal use software that is well established. Mature software will have less risk associated with offshoring, as it will be time-tested; these risks will be reflected in the cost of funds needed for the import. Risks are still present, however, and discount rates as high as 15% may be appropriate for such investments. This cost should be included in the business models.

Research and Development (R&D) Spill-Over: This valuation method relies on three key parameters: the investment in R&D, the period that such an investment will contribute to future income, and its benefit ratio. Spill-over can complement the output code metrics used to determine life by assessing the resource consumption of the code generation process. Economic benefits of R&D investments have been cited, but vary greatly. Assigning a multiplier of income to specific R&D adds another layer of

20 Samuelson, P.A. (1983). Foundations of Economic Analysis : Harvard University Press, 1947.

21 Kwon, D. and Watts, S. (2006), “IT Valuation in Turbulent Times.” The Journal of Strategic Information

Systems . Vol. 15, Issue 4 pp 327-354.

22 Laurie, R. (2004). “IP Valuation: Magic or Myth?” Intellectual Property Issues in M&A Transactions .

April.

10

difficulty

23

. Determining the start and end of life of R&D benefits is also difficult. Early, high risk R&D should have a longer life than investments in short-range product alterations. R&D life values of about seven years have been cited, but these are based on an unanalyzed mix of R&D

24

. The R&D spillover approach also falls short in that current accounting practice allows for software development and maintenance costs to be lumped together as R&D costs 25 . If maintenance costs, which comprise between 60 and 80% of software companies’ R&D expenses, would be logged as Cost of Goods Sold (COGS), a better understanding of the effect of R&D could emerge

26

. Until that time, valuation based on R&D spillover method is unreliable.

Real Options (RO) Valuation : For less mature software and other intangibles that have future income generating ability, which are currently yielding zero or negative returns, real options (RO) valuation is an alternative. Based on the Black-Sholes stock option valuation methodology, RO views investment in IP as an option to develop the current asset depending on the facts and circumstances at option dates (most likely key development milestones). A DCF-based future income input is the foundation for the underlying value of the IP, with the added option value tacking on and growing as a direct function of the amount of R&D cost associated with development

27

. A drawback is the myriad of variables inherent in options pricing, leading to heightened risk of improper valuation and pricing audits, especially for options not in the public view and marketplace. Divulging information regarding options for future expansion or cancellation of projects should be very unattractive to management

28

.

Market Capitalization

: Subtracting a company’s book value from its total market capitalization gives a ‘market worth’ of the company’s intangible assets based on the stockholders assessment of future income, already discounted for risk. If the items to be valued are only part of the companies’ products, then an allocation by sales volume can be made. Such an allocation becomes invalid when the products being assessed differ substantially in type and market from the items being excluded from the transfer.

Nevertheless, this top-down approach implies that shareholders have a better understanding about future income than analysts who aggregate corporate IP values bottom up. To what extent options known to management are valued by stock analysts and shareholders is also uncertain 29 . The relative value of options in the overall financial picture of a corporation is hard to assess in a company with a mix of activities.

Post-Offshoring Diminution of Software Value

One of the most often overlooked aspects of software – and a key aspect to its proper valuation – is the nature in which it depreciates. Any income-based valuation method

23 Leonard, Gregory and Lauren Stiroh (editors), (2005): Economic Approaches to Intellectual Property

Policy, Litigation, and Managemen t; National Economic Research Associates (NERA), White Plains, NY.

24 Grilliches, Z. (1984): R&D, Patents, and Productivity ; Univ. of Chicago Press.

25 Lev, B., (2001). Intangibles, Management, Measurement and Reporting ; Brookings Institution Press.

26 Wiederhold, G. (2006). “What is Your Software Worth?” Communications of the ACM , 49 (9), 65-75.

27 Damodaran, A. (2006). Dealing with Intangibles: Valuing Brand Names, Flexibility and Patents

Working Paper. Stern School of Business Reports. Jan., 2006.

28 Damodaran, A. (No date). The Promise and Peril of Real Options Working Paper. Stern School of

Business Reports. No date. Retrieved on May 31, 2007 from: http://pages.stern.nyu.edu/~adamodar/

29 Quick, Perry D., Timothy L. Day, Brian J. Cody, and Susan R. Fickling (2005). Using the Market

Capitalization Method To Value Buy-Ins: Beware of ‘Thing Three’, Transfer Pricing Report , Vol.14 No.

02 July 2005.

11

must consider the refreshment of IP through maintenance that software alone enjoys (new editions of books exhibit a similar renewal, however). This makes software slithery ; a product version bought today differs significantly from that of a few years ago, but the IP used to create the initial product is still employed in the current version. While maintenance refreshes value, it is costly, over a long life exceeding the original cost by a factor of 2 to 7, and there is an opportunity costs associated with these maintenance expenses. Maintenance costs can be estimated by tabulating development cost and maintenance expenses over the life of the software. Unfortunately, however, the importance of maintenance is still underestimated, as its contributory element to software value is still in the nascent stage of widespread recognition. As an example, the significance of maintenance is barely covered in software engineering curricula

30

.

Diminution of Software IP Value in Offshoring Arrangements

Entering into an offshoring arrangement has no distinct effect on the obsolescence of the software IP transferred. Conversely, key losses of economic value are attributable to technological (outdated or inefficient programming language or hardware), functional

(utility compromised due to market standards), and/or economic (market conditions or competition) obsolescence. The structure of offshoring contracts, however, has an effect on the amount of rework needed within the development cycle; this can add to or detract from future software maintenance needs: for example, fixed fee contracts tend to result in less rework

31

.

IP diminution is the relative reduction of initially created IP by the effort expended to subsequently maintain the full value of an item of software. Therefore, if maintenance costs come to equal the original cost of development, the IP is said to have ‘diminished’ by 50%. As some software embodies original concepts that have an indefinite useful life,

IP life is best limited to the time when the original contents becomes less than 10% of current contents (indicated in Figure 2).

The extent to which software IP has diminished will have an effect on future income and thus IP valuation. Income projections should thus assume that maintenance will be performed, leading to diminution of the original IP. A new metric is now borne: when the cost of maintenance exceeds the income attributable to the software, the effective life of software, as well as its contribution to IP value, ends 32 . Maintenance costs can be used to determine the horizon for the income projections.

Measuring Diminution

Software maintenance can be measured in several ways, however the well-documented, functional metric of lines-of-code (LoC), is the simplest and easiest to use

33

.Old code provided the essential functionality for initial purchasers, but also becomes well known and easily replicated; new code adds new value and keeps competitors at bay. Since

30 Wiederhold, G. (2006). “What is Your Software Worth?” Communications of the ACM , 49 (9), 65-75.

31 Gopal, A., Mukhopadhyay, T., Krishnan, M.S. and Goldenson, D. (2002). “The Role of Communication and Processes in Offshore Software Development” Communications of the ACM , Vol. 45, No.4, pp. 193-

200. April 2002.

32 Spolsky, J. (2004). Joel on Software . Apress.

33 Jones, C.T. (1998). Estimating Software Costs ; McGraw-Hill.

12

maintenance costs are often poorly accounted for, the LoC valuation method is the best approach available to indicate diminution, with the results having been validated

34

.

Figure 2: Diminution of the value of the original IP contribution in software.

34 Wiederhold, G. (2006). “What is Your Software Worth?” Communications of the ACM , 49 (9), 65-75.

13

When software is maintained, the total code grows steadily. The unit price for software products tends to be stable. Maintenance income can thus exceed sales income in due time 35 . Figure 3 shows income flows from inception for a single product having an

Erlang 12 sales projection, and appropriately demonstrates the phenomenon of maintenance costs superseding income flows

36

.

Combining the relative growth and constant price allows for an assessment of the value remaining of the original investment and the delineation of appropriate royalty rates. A typical life span for a successful software product is about 15 years. Over that life, there may be 7 significant version releases, more initially, fewer later in its life. Software that has significant dependencies to external conditions will require more frequent updates, and hence a higher level of royalties or cost-sharing. Transfer of mature software (three or more versions deep) will experience less future diminution than novel software. The mature scenario is actually typical for offshoring, since during initial development software creators have traditionally given little thought to outsourcing or offshoring possibilities. It is only when software is successful and call center and maintenance demands subsequently grow, that outsourcing be considered. Note, however, that concurrent development of original software using globally distributed teams has recently become more popular

37

.

Figure 3: Income for a software company that charges maintenance fees.

; however, IP consumed at a CFC when software is exported for development, package replication, and resale is ignored. Internal-use software suffers the same fate.

The location of IP and the structure of contracts to which it is bound have an impact on the type of valuation methodology employed; for instance, valuation tied to royalty rates may be more useful in accurately modeling the future cash flows of a particular item of

IP if royalties are being paid for the use of this IP. Regardless of the method of transferring IP that is used, however, valuation should be applied consistently.

35 Michael A. Cusumano: The Business of Software; Free Press, 2004

36 C. Chatfield and G.J. Goodhardt: A Consumer Purchasing Model with Erlang Interpurchase times;

Journal of the American Statistical Association, Dec 1973, Vol. 68, pages 828-835.

37 Gupta, A. and Seshasai, S. (2007). “24-Hour Knowledge Factory: Using Internet Technology to

Leverage Spatial and Temporal Separations.” ACM Transaction on Internet Technology (TOIT).

Vol. 7,

No. 3, 2007.

14

Why Should Companies Consider Software IP Value?

Let us consider a software company whose entire value depends on the IP incorporated in its products. Market capitalization – the number of shares outstanding multiplied by the prevailing value of each share (in a publicly traded company) – is a good estimate of a software company’s value, since the value of the intangible assets not yet valued and placed on the balance sheet is contained within this measure. But market capitalization tends to fluctuate. Almost all other economic sectors, from financials to manufacturing, depend to some extent, if not substantially, on software to supplement revenue generation. Any business that distinguishes itself from others by IP embedded in software is inherently at risk of loss, and valuation can better allow for protection against loss. The excess of market capitalization over a company’s book value can be greater than 6 times the value of its net assets; it is over two-thirds of the $7 trillion cumulative market value of all public companies put together. For businesses operating in knowledge-intensive industries, intangibles can account for over 97% of all assets

38

. An informed investor can potentially lead to better overall stock price valuation.

There are at least seven reasons for valuing software IP:

Transactional reasons: establishing a purchase price, royalty rate, and transfer price;

Financing reasons: assessing collateral value, and value as part of a solvency opinion;

Management information reasons: identifying, quantifying and subsequently managing the value of IP (IAM).

39

Risk assessment when entering into contracts;

Taxation reasons: export income, purchase price amortization, charitable contribution, and assessment value for ad valorem property taxation;

Bankruptcy reasons: assessing solvency of software owner, identification of licensing and spin-off opportunities;

Litigation reasons: quantifying copyright and trade secret infringements or contract breach damages, and;

Offshoring adds a new dimension, as it can lead to an increase in the risk of loss.

Computing the Value of Software

Almost all valuation methods – not just those pertaining to intangible assets like software

– carry the risk associated with subjectivity, as they rely heavily upon assumptive factors such as discount rates, growth rates, and future cash flow amounts and directions.

Software valuation relies upon these subjectivities, and adds additional confounding

38 Ibid.

39 Thornton, E.A. (2002). “Valuation of Software Intangible Assets.” ASA International Conference . San

Diego, CA. August.

15

problems of its own. Categorizing software as IP is complex, because a single item of software can embody multiple manifestations of IP, both physical and conceptual. How to properly allocate value to the multiple distinct manifestations of IP in specific software products and across product lines is complex, and involves significant subjectivity, especially when the IP in question is combined with other, overarching competitive advantages 40 .

Take a brand name that has brought value to an entire software product line for a period of years. Assume that the concerned company develops a new software product that addresses an unmet demand in the market. To what extent are the revenues – and thus the value – of this new product attributable to the brand name, rather than to its functional use? Would a different company with a less known brand name be able to realize the same level of sales? Questions like these complicate the discussion and lead to the need for subjective valuation decisions, and the ability to combine the contributions via an allocation of future income based on the IP embodied in software.

A complicating aspect of software is that it is slithery ; that is, it is always changing via maintenance efforts. In order to ensure its continued usefulness and applicability, software must be periodically updated so that it remains current. This results in a continuous change in the value of said software, and these variations must be reflected in the concerned valuation models

41

.

Due to lax regulation and characteristics inherently specific to software, little guidance exists for its valuation. When the topic was originally addressed, it was left to lawyers, vendors, and promoters to quantify software’s benefits; the resulting guidelines were more inconsistent than helpful 42 . Currently, the most thorough valuation occurs during mergers and acquisitions (M&A) when entire software companies must be valued.

Market capitalization provides a base for the aggregated value of all IP. However, the value of some items of software is not specifically determined. The need for proper valuation is growing as software is offshored in cross-border outsourcing arrangements.

Contract structuring in offshoring arrangements has a major impact on valuation, as we will show in this article. Currently, preexisting physical property rights are inapplicably applied to software, leading to inefficient contracts being drafted

43

. This misapplication occurs at the overall level, and also when analyzing facilities management, integration, and implementation contracts. Because excludability and usability can be separated, ownership rights and excludability rights need to be bifurcated and valued separately in order to accurately assign value to software and other items of IP.

40 Damodaran, A. (2006). Dealing with Intangibles: Valuing Brand Names, Flexibility and Patents

Working Paper. Stern School of Business Reports. Jan., 2006.

41 Wiederhold, G. (2006). “What is Your Software Worth?” Communications of the ACM , 49 (9), 65-75.

42 Lev, B., (2001). Intangibles, Management, Measurement and Reporting ; Brookings Institution Press.

43 Walden, E. A. (2005). “Intellectual Property Rights and Cannibalization in Information Technology

Outsourcing Contracts” MIS Quarterly , Volume 29 Number 4, December 2005, 699-720.

16

Basic Software Value Considerations

This section covers issues relevant to the estimation of the value of offshored software.

We explain why the cost of an offshoring arrangement is frequently underestimated and why the value of IP is not properly computed.

When is Software Property?

As many in the computer science community have argued, software should be a free,

‘emancipated’ asset, citing that some of the world's most successful and widely used software is free (GNU/Linux)

44

. Many academics have a bias against applying the term

‘property’ to any manifestation of knowledge; however, in 2002 alone, the software industry (SIC 7372) of exceeded $32 billion in total sales in the US alone. Today, total annual commercial software costs are estimated to be about $250 billion. Due to the unique profit generating ability that this manifestation of knowledge possesses, it is highly unlikely that all software will be free in the future

45

. Another element of software that implies that it can be property is the need to protect it from loss, a topic that has and is being debated

46

. This cost of protection and the risk of loss should play a role in the estimation of value of software. As distribution of software content can now occur over the web at no cost, our discussion focuses on the intangible representation of software rather than the disks or file storage space used.

Why are SW IP Values Currently Underestimated?

Software is termed as the "last remaining hidden corporate asset." Even though billions of dollars are spent on it every year, few managers truly understand the value that hardware and software contribute to their businesses. A study, performed in 2007, by Micro Focus and INSEAD highlights the current state of affairs: of the 250 chief information officers

(CIOs) and chief finance officers (CFOs) surveyed from companies in the US, UK,

France, Germany and Italy, less than 50% had even attempted to value their IT assets, and over 60% did not assess the value of their software 47 .

The motivation for proper valuation of IP is diminished by two factors: underdeveloped regulatory (accounting) regime; and the desire to minimize taxes. As was stated earlier, current US accounting practices disallow capitalization of software costs, except in the case of an acquisition, and stipulated accounting objectives – mainly measurability, relevance, and reliability – are the cause for many intangible assets to be disallowed from financial statement recognition. Even when recognized (currently only allowed in the case of purchased IP), a ‘fair-value’ approach is used. This value is insensitive to context, where the ‘value-in-use’ can be significantly more or significantly less. In practice, intangibles should be valued at the greater of their value-in-use or their fair market value

48

.

44 Gay, J. (Ed.) (2002). Free Software, Free Society: Selected essays of Richard M. Stallman : GNU Press.

45 Compustat (2004). Financial Results of Companies in SIC code 7211 and 723.

46 Branscomb, L. (chair) et al. (1991). Intellectual Property Issues in Software; Computer Science and

Telecommunications Board , National Research Council, National Academy Press, from: http://books.nap.edu/books/0309043441/html/

47 Kwan Yuk, P. and Stafford, P. (2007). “Study Urges IT Valuation Rethink,” The Financial Times , Nov.

4, 2007. Obtained from FT.com.

48 Laurie, R. (2004). “IP Valuation: Magic or Myth?” Intellectual Property Issues in M&A Transactions .

April.

17

U.S. Treasury regulations stipulate that companies must deal with each other ‘at arm’s length;’ i.e., that assets be bought and sold between controlled divisions at prevailing market rates, thus leading to proper taxation being levied upon the entities where the products were produced. Temporary regulations on transfer prices pertaining to IP transfers to and from controlled foreign operations have been issued, as discussed later.

This is a point of required valuation for transfers of IP to offshore entities; until recently, lax regulations allowed for very low IP valuations as companies attempted to ‘dumbdown’ the value added at high tax locations – and thus the taxes payable at those locations and vice versa. Companies had a strong disincentive to adopt true valuation methodologies.

Alternative Hosting Arrangements

When a sponsor company outsources work to a service organization, the host requires access to IP from the sponsor, in essence becoming a consumer of IP. We consider only cases where the host and user of the IP are foreign relative to the sponsor. Two distinct approaches are common:

1.

Outsourcing to an independent foreign host. Such a host is termed an Independent

Foreign Company (IFC);

2.

Outsourcing to an exclusive host, owned by the sponsor. The host in this case is termed a Controlled Foreign Corporation (CFC).

This distinction is important from the viewpoint of protection of intellectual property, as will be discussed later.

Contracted Operations

When contracting business out to IFCs, the choices of how to structure IP transfers, transactions, and remunerations are of key importance, along with a host of other areas

49

In particular, clients must “make intellectual property issues transparent at the contract

. stage, and arrive at precise agreements about what is and is not allowable, at what price, and what penalties arise from non-compliance with agreements or misappropriation of knowledge

50 .” Licensing agreements – where payments are tied to the use of the transferred IP or where a commission in connection with sales or services is paid versus actual export of IP to an offshore site – are widely used, and no transfer of owned IP need be made.

In the overall international trade balance of IP (including both royalties and fees), licensing transactions between sponsors and IFCs now account for more than 40% of all international transactions between unrelated companies, double the extent of just five years prior 51 . Recent literature has focused on optimal structures of these contracts for

49 Ranganathan, C. and Balaji, S. (2007) “Critical Capabilities for Offshore Outsourcing of Information

Systems” Management Information Systems Quarterly Executive (MISQE) , Vol. 6, No. 3, Sep. 2007.

50 Oshri, I., Kotlarsky, J. and Willcocks L. (2007) “Managing Dispersed Expertise in IT Offshore

Outsourcing: Lessons for Tata Consultancy Services” Management Information Systems Quarterly

Executive (MISQE) , Vol. 6, No. 2, June 2007.

51 Kamiyama, S., Sheehan, J, and Martinez, C. (2006). “Valuation and Exploitation of Intellectual

Property.” STI Working Paper 2006/5. Statistical Analysis of Science, Technology and Industry. http://www.oecd.org/sti/working-papers

18

clients and vendors; for example, time-and-materials contracts, while not efficient when considering the information known during the contract structure phase of development, tend to bring in higher revenues for vendors rather than their client counterparts 52 .

As of 1998, IP infringement cost reached an estimated $1 billion per day

53

. Software in particular is easy to copy, and is at risk even if limited to internal use. It is interesting to note that the FBI estimates that 80% of all electronic design theft is attributable to sources inside the company that created the IP – leading CFCs to be as suspect as IFCs.

Offshoring IP to countries that have weak enforcement of IP protection laws increases the risk of IP theft. To combat this type of loss, contracts may be drafted differently depending on the risk of misappropriation that is typically believed to be associated with

IFCs. Many IFCs pride themselves on the secure manner with which they protect the owners' intellectual property, but IP providers still have some reasons to be concerned.

The employees of an IFC are likely to work on more than one contract. The loyalty of employees of an IFC will be primarily to their employer, rather than to the owners of the intellectual property. Even when documents are protected, it may be difficult to protect the underlying concepts. Software development methods in particular are difficult to strictly sequester in an IFC host setting, though a number of vendors claim that they are developing approaches to achieve such isolation.

Owned Operations

When the value of IP to be transferred (or the risk of loss that may occur) is deemed to be high, the preferred approach is to set up a captive entity to provide the service. This is done primarily through establishment of a 50%+ owned foreign subsidiary, commonly referred to as a CFC. Even though CFCs are subject to different laws and standards, the control provided by ownership and control over this entity’s operations is deemed to be preferable to that of a vendor-client relationship.

Work done at a CFC is easier to monitor, some unpleasant surprises might be avoided.

CFCs can provide a number of complementary benefits to a parent company: function as marketing and sales centers for particular geographic and language areas; garner feedback from local constituents; and adapt products and marketing techniques to local conventions. CFCs must keep their own books, and will transfer costs or profits to the parent as stipulated by legal conventions and contracts.

The CFC option comes with a high up-front capital requirement, and can lead the company to deviate from core competencies. Once a CFC is established, however, future contractual arrangements become easier. Licensing or repatriation of IP can be used as remuneration to the sponsor. Licensing in particular is becoming popular: in 2004 licensing receipts totaled $110 billion, up from just $10 billion in 1984

54

. When

52 Gopal, A., Mukhopadhyay, T., Krishnan, M .S., and Sivaramakrishnan, K. (2003). “Contracts in

Offshore Software Development: An Empirical Analysis”, Management Science , Vol. 49, 12. Pp. 1671-

1683. 2003.

53 Mackintosh, I. et al. (2000). “Intellectual Property Protection: Schemes, Alternatives and Discussion. VSI

Alliance Intellectual Property Protection Development Working Group

54 Arora, A. (2005), “Patents: Who Uses Them, for What and What Are They Worth?” presentation at

EPO-OECD-BMWA International Conference on Intellectual Property as an Economic Asset: Key Issues in Valuation and Exploitation, 30 June-1 July 2005, Berlin, www.oecd.org/sti/ipr.)

19

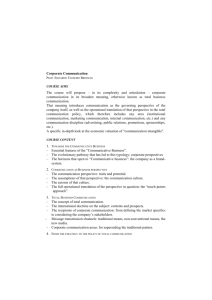

providing IP from a generating sponsor to a consuming CFC, three alternatives are possible, as shown in Figure 1.

Figure 1. Three alternatives for IP locations.

Location of the IP

When licensing, the formal ownership of the IP typically remains at the origin, and remuneration for use occurs in the form of royalties (the first alternative in Figure 1).

Royalties consist of payment for IP use and for house maintenance costs; product improvements are made at no extra charge. Usually, software is maintained at the parent company site; however, any offshore maintenance work can be reimbursed by the sponsor, which has the effect of keeping the IP wholly owned by the parent. Royalty rates ideally should match expected income flow from each item of IP being offshored.

A second alternative structure is an investment by the CFC in importing the software IP

(the middle diagram in Figure 1). Once this occurs, the amount of IP attributable to the

CFC can be based on relative sales percentage or some other metric. As an example: if

25% of the owner's products are sold via the CFC in question, the amount attributable is

25% of the total relevant IP involved in these sales efforts. In this case, maintenance costs will be shared between the CFC and the parent, and the CFC will receive reimbursement for any maintenance costs incurred.

The third alternative in Figure 1 involves three parties: the parent company, its CFC, and a controlled foreign holding (CFH) company. The end-consumer of the IP – the CFC – will continue to pay royalties to the newly interposed CFH. The CFH will then repatriate profits and losses to the parent, and will share maintenance costs as well. In this structure, a CFH can be strategically placed in a low or no tax locale, demand excessive royalty rates from the CFC, reducing taxes overall for the consolidated entity. The profitability of the CFC will be reduced and taxes commensurate with work performed will not be paid to the authorities in countries of both the parent company and the CFC.

Government Interest in Software Valuation: Taxation of IP Flows

While the benefits of valuing software are becoming apparent to companies, governments have had a vested interest in taxing IP transferred between foreign entities for a very long time. As touched upon earlier, income from the sale of property to foreign entities (at

20

arm’s length) mirrors local taxation, but taxation on the sale of IP as non-marketable, internal-use software remains problematical. Between related parties, the onus is on the taxpayer who sells the IP, just as it is for tangible properties. The concept of an ‘arm’s length standard’ is used primarily to allay any suspicion that minimization of taxes plays a role in the valuations. However, the method in which a value is ascertained does not play into the fulfillment of this standard. The ensuing lack of standardized, useful IP valuation techniques has in fact precluded the application of the arm’s length standard, and has led to underestimation of offshoring costs and lessened government tax revenues.

If the host receiving the IP is a captive CFC or CFH, then the transfer of IP may not be visible on the sponsor’s books, since the books show only aggregate value, if anything 55

.

The extraction of profits via royalties tied to the IP using complex intermediary structures is common, and the amounts involved in these arrangements are massive 56 . Developing countries are commonly deprived of tax income to grow their respective infrastructures

57

.

Some countries are stepping up to combat this problem 58 . The EU is also seeing more stringent transfer pricing documentation requirements. Additionally, many countries

(such as Brazil) are beginning to impose special taxes on service or IP importation, and these must be taken into account while making strategic decisions related to offshoring of

IT tasks

59

. Finally, new U.S. Treasury transfer pricing regulations (see: IRC §§ 1.482-

1T(d), 1.482-4T(f), 1.482-8T) seek to allow the usage of profit-based transfer pricing methodologies that allocate income in a manner corresponding with the economic value added; more so, at least, than the previously stipulated market and cost-based methods.

More regulation leads to a greater incentive on the part of industry to properly value IP, as the potential tax cost of undervaluation when transferring IP offshore can be staggering. Unpaid ‘back’ taxes sought by the IRS can be compounded by penalties amounting to 40% of the underpayment. These types of cases will become more common in the near future; 80% of all multinational companies expect to face a tax authority

‘pricing audit’ soon. For example, Merck is currently under scrutiny for $1.87 billion with the Canada Revenue Agency

60

. Aggressive tax positions will be challenged more often, leading companies to push for more good-faith estimates of taxes payable on IP transfers, driven by justifiable valuations. Thankfully, many of the inputs into transfer price determination mirror those of IP valuation, enabling these two practices to complement one another, benefiting businesses and governments alike.

55 GOA (1995, April). International Taxation: Transfer Pricing and Information on Nonpayment of Tax.

U.S. Government, GOA/GDD report 99-39.

56 Economist (2000, January 27). Gimme Shelter. Survey, The Economist .

57 OECD (1998). Organization for Economic Cooperation and Development (OECD): Harmful Tax

Competition, An Emerging Global issue; OECD.

58 Ihlwan, M. (2006, December 4). Public Scorn for Private Equity. Business Week .

59 Bierce, W. (2006). “Biggest Outsourcing Legal Issues of 2006.” HRO Europe . Jan., 2006. Retrieved from http://www.outsourcing-law.com/articles/1023 _biggest_legal _issues_2006.htm

60 Drucker, J. (2007). “Lifting the Veil on Tax Risk: New Accounting Rule Lays Bare A Firm’s Liability if

Transaction is Later Disallowed by the IRS” The Wall Street Journal . 25, May, 2007. Retrieved June 22,

2007 from http://webreprints .djreprints.com/sampleWSJwr.html

21

Conclusions

As offshoring becomes more widespread, and as regulation begins to increasingly permeate these arrangements, consistent IP valuation is becoming an important issue for businesses. Internet and communications technology allows for IP and capital to be transferred rapidly and invisibly, and while this ability facilitates electronic commerce, businesses face greater challenges in controlling the flow of their IP assets. The strategic exploitation of IP is vital to sustainable profitability, and is becoming more important in complying with regulations that continue to grow in complexity.

IP is the distinguishing driver in modern commerce, and its effects need to be properly quantified in order to ensure efficient use. This need is exacerbated in offshoring arrangements. Unfortunately, software, both the greatest contributor to profits and the greatest cost item for many modern companies, is not recognized on these companies’ balance sheets, significantly hindering the equitable analysis of these businesses. Many confounding attributes of software lead to this inequitable valuation: maintenance costs are not listed as cost of goods sold, and the common use of CFHs in tax haven countries leads to financial metrics for software companies being distorted.

The transfer of both monetary and intellectual capital must be considered when analyzing offshoring arrangements in scenarios espousing establishment of a CFC because failing to value IP in this scenario can lead to improper estimation of costs and risks. This may later prove to be more costly than if a company had expended the initial effort and money to ascertain the value of the IP to be transferred. While transfer of jobs has a high emotional interest and visibility, the long-term effects of intellectual capital transfer may well be of greater importance. Valuation is essential to assess:

1. The necessary investment for an offshoring arrangement: Sharing proprietary software or other items of IP in an offshoring arrangement operation requires ongoing royalty payments (or an initial investment). Proper valuation is needed to determine either the stream of royalty payments to be received or the initial investment amount. Software maturity, interacting with maintenance costs, must be assessed to set an appropriate discount rate in making either of these decisions.

2. The risks inherent in offshoring arrangements: As globalization continues to spread, parent companies in developed countries are more likely to enter into offshoring arrangements to have their software developed in a lower cost country. The risks associated with offshoring are of vital importance when assessing the cost of an offshoring arrangement, and can have a pervasive effect on discount rates used.

3. Tax effects when entering into offshoring arrangements: If an offshoring arrangement is entered into and IP is transferred, the export of such IP has to be valued and becomes taxable income. Distortions will occur if the export is not valued correctly, leading to possible future consequences and higher risk.

This article attempts to stress to business decision makers the importance of IP valuation in offshoring arrangements. The valuation of software is not easy, and requires many assumptions. But it can be done. The cost-benefit and risk analyses required for outsourcing software and software production depend on such valuations. Without this,

22

decisions about alternatives will be based on obsolete assumptions and may lead to erroneous decisions. In the end, it is still murky to both academics and executives which method of IP valuation is appropriate. Moreover, the difficulties in assessing IP value are such that attempts to do so are often precluded or seen as incidental to the project at hand: offshoring arrangements tend to exacerbate these problems due to the focus of myriad other factors. But, it is within these offshoring arrangements where IP valuation is most important.

23