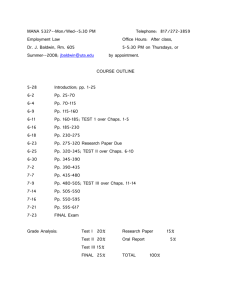

Debtor-Creditor Law: Usury, Jury Trials, and Defenses

advertisement