Sample Exam 2 Key

advertisement

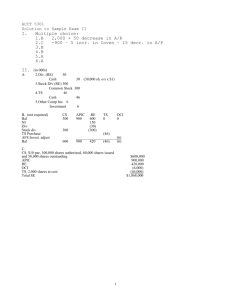

ACCT 5301 Solution to Sample Exam II I. Multiple choice: 1.E 2.B 3.B 4.B 5.A 6.A II. A. Invest. in Chicago 400,000 Cash 400,000 B. 1. Investment = 400,000 –32,000 + 40,000 = $408,000 2. Income = $40,000 Div. Receivable 32,000 Invest. in Chicago 32,000 Invest. in Chicago 40,000 Income from Chicago 40,000 III. 1. Invest. in Alpha 1,000 Cash 1,000 2. Invest. in Beta 2,000 Cash 2,000 3. Cash Cash 100 Div. Income 100 200 Div. Income 200 4. Alpha: $10 to $9 = $1 decrease x 100 shares = $100 unrealized loss Unrealized loss 100 Invest. in Alpha 100 Beta: $20 to $23 = $3 increase x 100 shares = $300 unrealized gain Invest. in Beta 300 Unrealized gain 300 5. Income statement of Chloe? Div. Inc. of 100 + Div. Inc. of 200 - Unrealized loss of $100 = net increase of $200 on I/S (the unrealized gain is on an AFS investment, and the effect is shown only in Other Comprehensive Income, as part of stockholders’ equity on the balance sheet.) IV. (in 000s) A. 2.Div. (RE) 30 Cash 30 (30,000 sh. o/s x $1) 3.Stock Div (RE) 300 Common Stock 300 4.TS 46 Cash 46 5.OCI 6 AFS Invest. 6 IV.B. CS, $10 par, 100,000 shares authorized, 60,000 shares issued and 58,000 shares outstanding $600,000 APIC 900,000 RE 420,000 OCI (6,000) TS, 2,000 shares at cost (46,000) Total SE $1,868,000 ($300,000 begin + 300 stock div.) (no change) Begin. 600 + NI 150 – Div 30 – Stock div 300_ Loss on AFS Invest Begin -0- + repurchase of 46 V. Pensions A. Pension expense: Service cost $ 30,000 Interest cost 20,000 Expected return -18,000 Amortization of PSC 2,000 Amortization of gain - 750 Total pension expense $ 33,250 B. C. Journal entry for 2008: Pension expense 33,250 Pension A/L (plug) Cash Adjustment to OCI and Pension A/L OCI 38,750 Pension A/L 13,250 20,000 for 2008 38,750 (see below) Pension A/L 25,000 13,250 Entry B 38,750 Entry C (to get to Liab. balance) ====== 27,000 Balance in OCI? Liab.: Beginning: Beginning: Change: Balance: + - 285,000 - 258,000 20,000 decrease (cost) 30,000 increase (benefit) 38,750 decrease (entry C) 28,750 Balance in Pension A/L: $27,000 Liability VI. Capital Lease A. PV of MLP = PV of Rent + PV of BPO Factors for PV: n = 5, i = 6% PVOA Adj.*to adjust to annuity due PVAD = 5,000 (4.21236)(1.06) = $22,326 PV1 + PV1 = 1,000 (.74726) = Total present value = B. 747 $23,073 1. Equipment 23,073 Lease Liability 23,073 2. Lease Liability Cash 5,000 Interest expense Lease liability Cash 1,084 3,916 3. 4. 5,000 18,073 x .06 plug 5,000 Depreciation expense 2,884 Accumulated Depr. 2,884 (Calc: (23,073 - 0)/8 = 2,884) VII. Operating lease PV,6% n=1 43 x .9434 n=2 28 x .89 n=3 22 x .83962 n=4 18 x .79209 n=5 16 x .74726 *n=6 16 x .70496 *n=7 16 x .66506 Total = $ 40.56 = 24.92 = 18.47 = 14.26 = 11.96 = 11.28 = 10.64 $ 132.8 million *since approx. 2 payments at $16 each, just do 2 more PV1 calculations. Alt: PVOA of 2 pmts back to time 0: 2 pmts back to time 0 16(PVOA, 6%, 2)(PV1, 6%,5) = 16 x (1.83339) x (.74726) = $21.92 VIII. 1. D 2. B 3. B 4. A 5. C Classification Part IX Schedule Pretax financial income (loss) Future Deductible: Warranties Subscription Revenues Future Taxable: Depreciation Excess equity method income Taxable (deductible) amount Tax rate Income tax payable DIT - liab (asset) 2008 IT Pay 100,000 DIT 8,000 15,000 (8,000) (15,000) (800) (13,000) 109,200 30% 800 13,000 (9,200) 30% 32,760 (2,760) DIT 0 2,760 2,760 Journal entry: Income tax expense (plug) DIT Income tax payable 0 30,000 2,760 32,760 X. Statement of Cash Flows (analysis in red) Given the following income statement and comparative balance sheets for North (all amounts are in thousands). Note that earliest year is presented first. Cash Accounts receivable Inventory Land Equip Less: Accumulated depr. Investment. Total assets Comparative Balance Sheets 12/31/06 12/31/07 $ 15 -6 $ 9 17 23 +6 SUBTRACT(OP) 7 14 +7 SUBTRACT (OP) 38 28 50 73 ( 18) ( 24) 37 37 $ 146 $ 160 Accounts payable Unearned Revenues Notes payable (long-term) Bonds payable (long-term) Add: Premium Common stock Retained earnings Total Liab. & Eq. Income Statement for 2006 Sales revenue Service revenue Gain on sale of land Cost of goods sold Depreciation expense - equipment Interest expense Other operating expenses (all cash) Income tax expense Net income $ 13 7 18 50 8 34 16 146 $ 15 +2 ADD (OP) 5 -2 SUBTRACT (OP) 10 50 5 –3 OP 55 20 160 $ 120 30 3 –3 OP (82) ( 6)+6 OP ( 6) (11) (13) $ 35 TOP LINE OP Additional information for 2006: FOR INVESTING AND FINANCING 1. The only activities in retained earnings were for income and dividends. BRE + NI – DIV = ERE 16+35-DIV=20 DIV=31 –31 FINANCING 2. Equip. was purchased for $8 cash. –8 INVEST 3. Equip. was purchased with a N/P of $15. SUPP SCHEDULE 4. Land with a cost of $10 was sold at a gain of $3 . +13 INVEST 5. Payment made on N/P for $23. –23 FINANCING 6. The change in common stock was due to the issue of stock for cash. +21 FIN Required: On the next page, prepare the Statement of Cash Flows, including Indirect method fo Operating Section. Cash Flow from Operating Activity Net Income Add Depreciation Subtract Premium amort. Subtract gain Less increase in A/R Less increase in Inventory Add increase in A/Pay Less decrease in U. Rev $35 6 (3) (3) ( 6) (7) 2 (2) Net cash from operating activity $ 22 Cash Flow from Investing Activity Cash paid for equip Cash received from land $(8) 13 Net cash from investing 5 Cash Flow from Financing Activity Cash paid for dividends Cash paid on N/P Cash received from stock $ (31) (23) 21 Net cash used for financing (33) Net decrease in cash $(6) (Confirm: cash from $15 to $9) ________________________________________________ Supplementary schedule of non-cash activities: Equip purchased with N/P $15 Part 2: Operating section using direct method Sales revenue Service income Gain on sale of land COGS Depr exp Other Interest exp Income tax expense Cash from operations $120 30 3 -82 -6 -11 - 6 -13 - 6 = $ -2 = - 3 = -7 +2 = +6 = -3 = = 114 28 0 (87) 0 (11) ( 9) adjust out prem. amort (13) $22 (same as indirect method)