BlackRock Indexed Australian Bond Fund

advertisement

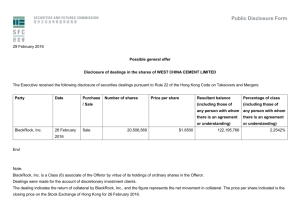

BLACKROCK INDEXED AUSTRALIAN BOND FUND FUND UPDATE 31 December 2015 Investment Performance (%) 1 Mth 3 Mths YTD 1 Yr 3 Yrs 5 Yrs Since Incep BlackRock Wholesale Indexed Australian Bond Fund (Gross of Fees) 0.33 -0.24 2.64 2.64 4.82 6.75 6.21 Bloomberg AusBond Composite IndexSM (Gross of Fees) 0.33 -0.25 2.59 2.59 4.73 6.62 6.12 Outperformance (Gross of Fees) 0.00 0.01 0.06 0.06 0.09 0.12 0.09 BlackRock Indexed Australian Bond Fund (Net of Fees) 0.32 -0.28 2.48 2.48 4.66 6.57 5.85 Bloomberg AusBond Composite IndexSM (Gross of Fees) 0.33 -0.25 2.59 2.59 4.73 6.62 5.98 -0.01 -0.04 -0.10 -0.10 -0.07 -0.06 -0.13 Outperformance (Net of Fees) *Fund inception: 02/07/1998. ^Fund inception: 14/11/2001 Past performance is not a reliable indicator of future performance. Performance for periods greater than one year is annualised. Performance is calculated in Australian dollars and assumes reinvestment of distributions. Gross performance is calculated gross of ongoing fees and expenses. Net performance is calculated on exit-to-exit price basis, e.g. net of ongoing fees and expenses. Fund Performance (Gross of Fees) to 31 December 2015 200% Fund Benchmark 150% 100% 50% 0% -50% Dec 1999 Dec 2001 Dec 2003 Dec 2005 Dec 2007 Dec 2009 Dec 2011 Dec 2013 Dec 2015 Performance Summary Market Review The primary focus of global bond markets was on the US Federal Reserve meeting on December 17 which resulted in a 25 basis point increase in the policy rate. Such a move was broadly anticipated by market participants. US treasury yields rose during the month while the curve flattened. The ECB, on the other hand, after indicating a disposition to further ease policy failed to follow through leading to increases in German bond yields. Corporate bond markets came under notable pressure as oil prices continued to decline sharply, which was further exacerbated by headlines around the liquidation of a sizeable US high yield mutual fund. Visit BlackRock.com.au for further information, including: • Market Insights & Commentary • Fund Performance • Unit Prices Domestically, despite reaffirming an easing bias at the RBA Board meeting on December 1, it appears that the RBA has no immediate plans to cut the policy rate. The maintenance of an easing bias in December appeared to reflect the recent weakness in inflation: “[RBA Board] members observed that the outlook for inflation may afford scope for further easing of policy, should that be appropriate to support demand”. At the same time, however, the RBA gave a more upbeat assessment of the economy: “the [RBA] Board again judged that the prospects for an improvement in economic conditions had firmed a little over recent months and leaving the cash rate unchanged was appropriate at this meeting”. The Australian 10 year bond yield increased very slightly during the month finishing at 2.88% or 2 basis points higher than at the end of November. The 3 year bond yield fell 8 basis points to 2.02%. Physical yields on 3 month bank bills increased 10 basis points to 2.375%. The Bloomberg AusBond Composite Bond Index returned 0.33% in December for a 12 month return of 2.59%. The fund matched the return of the benchmark in December. The benchmark added $6.3 billion (face value) in new issues and taps over the month but maturities and buy-backs left the market capitalisation of the benchmark marginally lower at $862 billion. Treasury issuance totaled $4.2 billion while semi-government issuance was minimal at $0.7 billion. The non-government sector added $1.3 billion to the benchmark. The funds largest active issuer exposure is 0.20% to KFW with the largest active underweight being -0.28% to BNG. The portfolio currently has 392 issues versus 534 in the benchmark. The funds index duplication ratio is 93%. Sector Exposure Govt 45.89 46.04 Semi-Govt 26.52 26.57 Supra/Sovereign 14.24 14.20 Corporates 12.98 12.97 MBS 0.29 0.21 Cash/Other 0.08 0.01 0.0% <3 30.29 30.03 3-5 23.75 24.08 5-7 14.58 14.65 7 - 10 19.23 19.12 >= 10 12.15 12.13 0.0% 40.0% 50.0% Benchmark Market Value % 10.0% Market Value % 20.0% 30.0% 40.0% Benchmark Market Value % Quality Exposure AAA Rated AA Rated BBB Rated NR Rated This is against a backdrop of some residual uncertainties in Europe, uncertainties about the Chinese growth outlook and the likely policy response and some stresses in emerging markets. Yield As outlined above the RBA at the moment is of the view that current low inflation levels give them the scope to cut the policy rate if they arrive at a judgement that demand needs further support. However, in their view they are yet to arrive at the point where they think that demand needs that further support. However, in our view the housing sector, which has been the engine of private final domestic demand (either directly or indirectly through household spending) is in fragile balance. Building approvals appear to have peaked foreshadowing some future decline in residential construction. At the same time surveys indicate consumers are increasingly circumspect about whether it is a ‘good time to buy’ a house and there are signs that 30.0% Maturity Exposure Looking ahead, global financial markets continue to assess the prospect of divergent monetary policy in the key developed markets, with a particular focus on the pace of Fed tightening through 2016. Weakness in commodity markets, particularly oil, suggests that that in the near-term volatile markets are likely as we go into 2016. The challenge in Australia remains one of transitioning growth leadership from mining investment to other sources of activity growth. Capex expectations remain bleak. Mining investment looks like subtracting around 2 percentage points from GDP growth in the coming fiscal year while business investment elsewhere remains languid. There has been some growth over the past year in net export volumes and in household spending and residential construction (the former being largely motivated by the latter and “funded” by a decline in the savings rate given lacklustre wage growth). Encouragingly, labour market indicators have stabilised after a period of weakness perhaps reflecting some growth in the services areas most exposed to the decline in the $A. 20.0% Market Value% A Rated Market and Outlook Commentary 10.0% 73.49 73.44 18.31 19.13 5.21 4.79 2.91 2.59 0.00 0.05 0.0% 25.0% Market Value % Govt 2.47 2.46 Semi-Govt 2.64 2.65 Supra/Sovereign 2.83 2.84 Corporates 3.54 3.51 MBS 3.05 3.22 Unclassified 0.00 0.00 0.00 Yield 50.0% 75.0% Benchmark Market Value % 1.00 2.00 3.00 4.00 Benchmark Yield Top 10 Issuers Issuer Weight % AUSTRALIA (COMMONWEALTH OF) 45.4 QUEENSLAND TREASURY CORPORATION 9.9 NEW SOUTH WALES TREASURY CORPORATION 6.3 TREASURY CORPORATION OF VICTORIA 4.3 WESTERN AUSTRALIAN TREASURY CORPORATION 3.9 KFW 3.5 EUROPEAN INVESTMENT BANK 1.9 LANDWIRTSCHAFTLICHE RENTENBANK 1.4 INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT 1.3 ASIAN DEVELOPMENT BANK 1.2 house prices are decelerating. The regulators have also implemented a number of macro-prudential measures. These have resulted in ‘out of cycle’ mortgage rate increases from the banks which are likely to intensify headwinds to residential construction and household spending. Domestic markets are pricing some probability of a further cut in interest rates by the RBA with around a full 25bp reduction ‘priced’ out to the end of 2016. Given our concerns surrounding downside risks to activity growth and fragility in the housing sector we expect that the RBA does cut rates again in 2016. We judge the risks on the AUD to be weighted toward the downside. The AUD view reflects our assessment regarding headwinds to growth (particularly capex but potentially housing); the likely course of the terms of trade (reflecting declining prices for Australia’s commodity exports); a possible further RBA rate cut; and an expectation that the US Federal Reserve will raise the policy rate again in 2016. Industry Contribution to DxS Financials 0.02858 Consumer Discretionary 0.01089 Technology 0.00750 Materials 0.00433 Energy 0.00149 Industrials 0.00130 Consumer Staples 0.00093 MBS -0.00107 Utilities -0.00321 Communications -0.00350 Government -0.02926 -0.04 -0.02 0.00 0.02 0.04 0.06 Active DxS Contribution (o) Risk Characteristics Fund Benchmark Difference Modified Duration (Years) 4.65 4.66 0.00 Duration x spread 1.34 1.33 0.01 Yield 2.71 2.70 0.00 Average Coupon (%) 4.76 4.75 Average Maturity (Years) 5.56 5.56 Issuer Contribution to DxS ANU 0.00777 WFC 0.00572 0.01 DEXUS 0.00549 0.00 AAPL 0.00518 AQUA 0.00511 Contribution to Modified Duration LLCAU 0.00494 Govt 2.55 2.55 RABOBK 0.00491 Semi-Govt 1.16 1.16 DUEAU 0.00483 Supra/Sovereign 0.52 0.53 SGPAU 0.00440 Corporates 0.42 0.42 CEUAU 0.00429 MBS 0.00 0.00 -0.00399 0.00 0.00 CAF Other WESAIR -0.00407 EIBKOR -0.00427 KBN -0.00483 DOWAU -0.00502 SAFA -0.00565 NTTC -0.00567 GS -0.00683 NEDWBK -0.00864 BNG -0.01264 0.00 Yield 1.00 Benchmark Yield 2.00 3.00 -0.015 -0.010 -0.005 0.000 0.005 0.010 0.015 0.020 Active DxS Contribution (o) Contribution to Duration x Spread Semi-Govt 0.40 0.40 Supra/Sovereign 0.34 0.34 Corporates 0.60 0.58 MBS 0.00 0.00 Unclassified 0.00 0.00 0.00 Yield 0.50 Benchmark Yield 1.00 About the Fund Investment Objective The Fund aims to match the performance of the Bloomberg AusBond Composite IndexSM before fees. Fund Strategy The strategy aims to track the benchmark by closely matching the distribution of the benchmark’s major risk and return factors. This is done using a methodology commonly referred to as stratified sampling, where the benchmark and the investment portfolio are broken down into “cells” of securities with similar risk and return factors. The major risk and return factors are interest-rate risk, sector risk and specific (individual security) risk. We select securities that match the overall characteristics of each cell in amounts consistent with the index weighting and modified duration of the cells they represent. By matching at the cell level, the overall risk and return characteristics of the portfolio will closely match those of the benchmark. Should be considered by investors who … Seek a broad exposure to Australian bonds. Seek a fund that uses a stratified-sampling approach so returns match those of the Australian bond market before fees. Have a long term investment horizon. Fund Details BlackRock Wholesale Indexed Australian Bond Fund APIR Fund Size Buy/Sell Spread Tracking Error (3 Years p.a.) BGL0008AU 2,122 mil 0.05%/0.07% 0.02% BlackRock Indexed Australian Bond Fund APIR Management Fee BGL0105AU 0.20% p.a. Issued by BlackRock Asset Management Australia Limited (AFS License No. 225398, ABN 33 001 804 566) (“BlackRock”). BlackRock is the responsible entity of the Fund(s) referred to in this document. An Offer Document for the Fund(s) is available from BlackRock. Potential investors should consider the Offer Document in deciding whether to acquire, or to continue to hold, units in the Fund(s). BlackRock, its officers, employees and agents believe that the information in this document is correct at the time of compilation, but no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors or omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This document contains general information only and is not intended to represent general or specific investment or professional advice. The information does not take into account an individual’s financial circumstances. An assessment should be made as to whether the information is appropriate in individual circumstances and consideration should be given to talking to a financial or other professional adviser before making an investment decision. No guarantee as to the capital value of investments in the Fund(s) nor future returns is made by BlackRock. If you have any queries relating to any of this information or to obtain a copy of the Offer Document for the Fund(s), please contact your relationship manager. Alternatively, if you have a query relating to the wholesale funds, please contact Institutional Client Services on ICS-Australia@blackrock.com, or please call Adviser Services on 1300 366 101 if you have a query relating to our retail fund range.