Can American Funds Sustain Its

Outperformance?

June 30, 2015

by Larry Swedroe

Among actively managed funds, American Funds has a reputation for providing investor-friendly, lowcost products with sustained records of outperformance. But has it outperformed comparable funds

from Vanguard and Dimensional Fund Advisors (DFA)? If so, should investors expect its funds to

maintain their edge?

I’ll answer those questions.

American Funds is the third largest mutual fund family (following Vanguard and Fidelity) in the United

States. According to Morningstar, as of May 31, 2015, American Funds had nearly $1.3 trillion in

assets under management across its lineup of mutual fund offerings.

The firm is an extremely popular choice among active investors and for some very good reasons. The

fees it charges are investor friendly, certainly so for an active manager. American Funds doesn’t rely

on “star managers” who can pick up and leave, taking their investment approach with them. Rather,

the firm relies on a team of managers. It avoids the style drift that causes investors to lose control over

the risk of their portfolios. And finally, the firm has become one of the market’s largest mutual fund

companies because its track record is good.

The firm’s website states: “We base our decisions on a long-term perspective, which we believe aligns

our goals with the interest of our clients. Our portfolio managers average 27 years of investment

experience, including 22 years at our company, reflecting a career commitment to our long-term

approach.”

American Funds describes its investment philosophy as “based on doing what…is right for clients.” It

claims to “reward long-term results” through investment professional compensation that’s “heavily

influenced by results over four- and eight-year periods” and to “invest alongside” its clients. Collectively,

the firm notes, its “associates are significant investors in the company’s investment offerings.”

Recognizing the long-term success achieved by the Capital Group (the firm that manages the

American Funds family of mutual funds), Charles Ellis wrote about them in his 2004 book, Capital:

The Story of Long-Term Investment Excellence.

Active versus passive

As is my practice, and given the firm’s assertions about its long-term investment approach, I’ll compare

the performance of American Funds’ actively managed equity funds to similar offerings from two

Page 1, ©2016 Advisor Perspectives, Inc. All rights reserved.

prominent providers of passively managed funds, DFA and Vanguard. (Full disclosure: My firm,

Buckingham, recommends DFA funds in constructing client portfolios.)

To keep the list to a manageable number of funds and to make sure I look at long-term results through

full economic cycles, I will analyze the 15-year period that ended June 12, 2015. Also, I’ll use the

lowest cost shares available when more than one class of fund is available for the full period.

Furthermore, in cases where American Funds has more than one fund in an asset class, I’ll use the

average return of those funds in my comparison.

The table below shows the performance of seven funds offered by American Funds in five asset

classes.

15 Years Ending June 12, 2015

Page 2, ©2016 Advisor Perspectives, Inc. All rights reserved.

Symbol

Annualized

Return (%)

Expense

Ratio (%)

Fundamental Investors

RFNFX

6.8

0.35

Investment Company of America

RICFX

6.1

0.35

6.5

0.35

Fund

U.S. Large Blend

American Funds Average

DFA U.S. Large Company

DFUSX

4.5

0.08

Vanguard Institutional Index

VINIX

4.5

0.04

AMCAP

RAFFX

6.9

0.41

Growth Fund of America

RGAFX

5.7

0.38

New Economy

RNGFX

5.3

0.52

6.0

0.44

VIGIX

3.7

0.08

American Mutual

RMFFX

7.6

0.36

Washington Mutual

RWMFX

6.8

0.35

7.2

0.36

U.S. Large Growth

American Funds Average

Vanguard Growth Index

U.S. Large Value

American Funds Average

DFA U.S. Large Cap Value

DFUVX

8.9

0.13

Vanguard Value Index

VIVIX

5.8

0.08

Page 3, ©2016 Advisor Perspectives, Inc. All rights reserved.

Foreign Large Growth

Europacific Growth

RERFX

5.3

0.54

Vanguard International Growth Admiral

VWILX

4.4

0.34

New World

RNWFX

8.1

0.69

DFA Emerging Markets

DFEMX

8.2

0.56

Vanguard Emerging Markets

VEIEX

8.1

0.33

Emerging Markets

Before reviewing our results, it’s important to note that the lower-cost R5 share class offered by

American Funds is only available to investors in retirement plans. Even though we’re also looking at

the lowest-cost version of funds from Vanguard and DFA, their fees don’t increase as drastically

across share classes as is the case with American Funds. Moreover, American Funds has a variety of

other share classes that it claims allows it “to compensate your financial professional for helping you

decide which funds are right.”

While the gap between the expense ratios of the lowest-cost and highest-cost funds in share classes

from DFA and Vanguard can typically be measured by counting basis points on the fingers of your two

hands, the same gap between the American Funds share classes can be more than 1.2 percentage

points. And some of the share classes come with sales charges, deferred sales charges or hefty 12b-1

fees (up to 1%).

With this very important caveat in mind, the following is a summary of the data in the above table:

Of the three asset classes for which there are comparable DFA funds, offerings from American

Funds provided a higher return in one of them.

Of the five asset classes for which there are comparable Vanguard funds, offerings from

American Funds provided higher returns in four of them, and there was a tie in the fifth.

An American Funds portfolio equal-weighted in the three asset classes for which there are

comparable DFA funds returned 7.3% a year. The portfolio’s average expense ratio was 0.47%.

A DFA portfolio, equal-weighted in those same three asset classes, returned 7.2% a year,

Page 4, ©2016 Advisor Perspectives, Inc. All rights reserved.

underperforming its counterpart American Funds portfolio by 0.1 percentage point a year. The

portfolio’s average expense ratio was 0.26%.

An American Funds portfolio equal-weighted in the five asset classes for which there are

comparable Vanguard funds returned 6.6% a year. The portfolio’s average expense ratio was

0.48%. A Vanguard portfolio, equal-weighted in those same five asset classes, returned 5.3% a

year, underperforming its American Funds counterpart by 1.3 percentage points. The portfolio’s

average expense ratio was 0.17%.

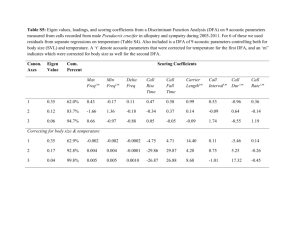

Factor analysis

We’ll now take another look at American Funds’ performance using the analytical tools and data

available at Portfolio Visualizer. The table below shows the results of a three-factor (beta, size and

value), four-factor (adding momentum) and six-factor (adding quality and low beta) analysis of the

firm’s domestic funds.

Factor analysis provides important insights, showing the sources of returns for each fund. For

example, Morningstar classifies each fund based on the fund’s holdings in each of its nine style boxes.

Thus, during periods when value outperforms growth, growth or blend funds could appear to be

generating alpha relative to a (pure) index fund in the same style box while actually generating negative

alpha based on its holdings (which include value stocks).

Data in the table below covers the period from June 2002 through February 2015. The t-stats are in

parentheses.

Page 5, ©2016 Advisor Perspectives, Inc. All rights reserved.

ThreeFactor

Annual

Alpha (%)

FourFactor

Annual

Alpha (%)

SixFactor

Annual

Alpha (%)

Fund

Symbol

Fundamental Investors R5

RFNFX

1.0

(1.1)

0.9

(1.0)

0.8

(0.9)

Investment Company of America

RICFX

0.4

(0.6)

0.5

(0.7)

0.1

(0.1)

AMCAP

RAFFX

0.4

(0.4)

0.6

(0.8)

0.8

(0.9)

Growth Fund of America

RGAFX

0.6

(0.8)

0.5

(0.6)

1.5

(1.9)

New Economy

RNGFX

0.7

(0.5)

0.9

(0.8)

2.7

(2.2)

American Mutual

RMFFX

0.9

(1.3)

1.0

(1.4)

0.0

(0.0)

Washington Mutual

RWMFX

0.3

(0.3)

0.5

(0.6)

-0.2

(-0.3)

0.6

0.7

0.8

Average

When we look at the three-factor analysis, we find that all seven of the American Funds offerings

generated annual alphas. However, none of those alphas were statistically significant at the 5% level.

The average annual alpha was 0.6%.

When we examine results from the four-factor analysis, we also find that all seven of the American

Funds offerings generated alpha. Again, none of that alpha was statistically significant at the 5% level.

The annual alpha was 0.7%.

When we include all six factors, we find that five generated annual alphas, one of which was

statistically significant at the 5% level. The average annual alpha was 0.8%.

At this point, I normally include a caveat warning readers that the returns data I have presented is all

Page 6, ©2016 Advisor Perspectives, Inc. All rights reserved.

pre-tax, and the higher turnover of actively managed funds generally creates a significantly higher

burden when it comes to taxes. However, using Morningstar data, we discover that the average

turnover of these seven American Funds offerings was an index-like 25%. While that remains higher

than the 6% average turnover rate of the five Vanguard funds we examined, it’s still pretty low. The

average turnover rate of the three funds from DFA that we evaluated was about 8%.

An enviable record

The American Funds family of mutual funds certainly has produced an enviable record, whether you’re

comparing performance to actively managed or passively managed funds. They outperformed similar

Vanguard funds by 1.3 percentage points a year and basically matched the performance of comparable

DFA funds (underperforming in two of the three asset classes, but outperforming by 0.1% from a

portfolio perspective).

There’s a lot about the firm to admire. It keeps expense and turnover ratios relatively low. And, like I

mentioned previously, it doesn’t rely on star managers that can leave the firm. What’s more, its

managers make significant investments in the funds they run. In addition, factor analysis demonstrates

that they tend to avoid the “style drift” which can cause investors in actively managed funds to lose

control over their asset allocations and, as a result, the risk of their portfolio.

If one had to choose an actively managed fund family, this would be a good choice.

A problem for American Funds, and an issue for their investors, is that the hurdles to achieving alpha

are growing. One large hurdle the firm faces is a direct result of its own success. They now have

almost $1.3 trillion in assets under management, up from less than $1 trillion only four years ago.

A growing asset base creates an ever-higher hurdle for active managers because either the cost of

trading can increase (market impact costs rise) or they are forced to diversify more (and become closet

indexers).

Academic research continues to convert what once was alpha into beta, the pool of victims that can be

exploited has collapsed, competition has gotten much tougher and the supply of capital chasing alpha

has exploded. Those four hurdles are the focus of my latest book, “The Incredible Shrinking Alpha,”

which I co-authored with Andrew Berkin, the director of research at Bridgeway Capital Management.

With that being said, to determine if there has been any deterioration in American Funds’ ability to

outperform, we can look back at the firm’s performance data over the last five years and then compare

it to the performance data for the full 15 years.

Five Years Ending June 12, 2015

Page 7, ©2016 Advisor Perspectives, Inc. All rights reserved.

Symbol

Annualized

Return (%)

Fundamental Investors

RFNFX

15.4

Investment Company of America

RICFX

15.2

Fund

U.S. Large Blend

American Funds Average

15.3

DFA U.S. Large Company

DFUSX

16.2

Vanguard Institutional Index

VINIX

16.3

AMCAP

RAFFX

17.3

Growth Fund of America

RGAFX

16.0

New Economy

RNGFX

18.3

U.S. Large Growth

American Funds Average

Vanguard Growth Index

17.2

VIGIX

17.5

American Mutual

RMFFX

14.5

Washington Mutual

RWMFX

16.0

U.S. Large Value

American Funds Average

15.3

DFA U.S. Large Cap Value

DFUVX

17.1

Vanguard Value Index

VIVIX

15.4

Page 8, ©2016 Advisor Perspectives, Inc. All rights reserved.

Foreign Large Growth

Europacific Growth

RERFX

9.9

Vanguard International Growth Admiral

VWILX

10.6

New World

RNWFX

6.9

DFA Emerging Markets

DFEMX

3.8

Vanguard Emerging Markets

VEIEX

3.8

Emerging Markets

The following is a summary of the data in the table above compared to the results of the full 15-year

period:

The results for DFA funds and the American Funds were identical. Comparable DFA funds

outperformed in two of the three asset classes, but the American Funds portfolio outperformed

by 0.1 percentage point.

Relative to the Vanguard funds, the American Funds’ results were quite different. For the 15-year

period, comparable Vanguard funds didn’t outperform in any of the five asset classes, although

there was one tie. But over the last five years, offerings from American Funds underperformed in

four. However, the American Funds portfolio still outperformed the Vanguard portfolio, though by

a much smaller amount (0.2% for the five-year period versus 1.3% for the 15-year period).

For taxable investors, even though the turnover of the American Funds offerings we’ve used in our

analysis is low for an active manager, it was still about 20% higher in this period than for the

comparable funds from DFA and Vanguard. Given the firm’s slight advantage in pre-tax

outperformance (0.1 percentage points versus DFA and 0.2 percentage points versus Vanguard), that

higher turnover easily could have resulted in lower after-tax returns.

The bottom line is that there was the slimmest margin of outperformance versus the DFA funds (while

underperforming in two of the three asset classes) in both periods, and the outperformance gap

relative to the Vanguard funds shrunk from 1.3 percentage points to a bare 0.2 percentage points

(while underperforming in four of the five asset classes).

Consistent with both the historical evidence on the ability of active managers to maintain

outperformance and the evidence that the hurdles to generating alpha are getting higher and higher for

Page 9, ©2016 Advisor Perspectives, Inc. All rights reserved.

the overall industry, the performance advantage maintained by American Funds has shrunk, and the

recent slim advantage could even turn negative for investors in share classes with higher expenses. It

remains to be seen whether the firm can continue to generate outperformance.

Larry Swedroe is director of research for the BAM Alliance, a community of more than 150

independent registered investment advisors throughout the country.

Page 10, ©2016 Advisor Perspectives, Inc. All rights reserved.