Qantas Airways Ltd

advertisement

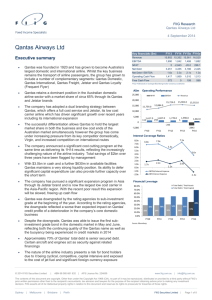

FIIG Research Qantas Airways Ltd 24 April 2014 Qantas Airways Ltd Executive summary Qantas was founded in 1920 and has grown to be Australia’s largest domestic and international airline Key financials ($m) HY to 31 December 2013 Whilst the key business remains the transport of airline passengers, the group has grown to include a number of complimentary segments: Qantas domestic, Qantas international,Qantas freight, Jetstar and Qantas frequent flyer Underlying EBITDA Qantas retains a dominant position in the Australian domestic airline sector with a market share of circa 65% through its Qantas and Jetstar brands The company has employed a duel branding strategy between Qantas, which offers a full cost service and Jetstar, its low cost carrier airline which has driven significant growth over recent years including its international expansion The successful differentiation allows the Group to hold the largest market share in both the business and low cost ends of the Australian market simultaneously however the group has come under increasing pressure from its key competitor domestically, Virgin, and increased competition on international routes The company announced a significant cost cutting program at the same time as delivering its half year 2014 results, reflecting the loss for the half. Total savings of $2bn over three years have been flagged by management With $2.4bn in cash and a further $630m in available facilities Qantas maintains a very strong liquidity position. Its ability to defer significant capital expenditure can also provide further capacity over the short term The company has pursued a significant expansion program in Asia through its Jetstar brand and is now the largest low cost carrier in the Asia-Pacific region. With the recent poor result this expansion will be slowed, freeing up some cash flow The nature of the airline industry presents a risk for bond holders due to it being cyclical, competitive, capital intensive and exposed to the cost of jet fuel and significant FX-risk exposure Investors in Qantas bonds enjoy stronger returns than bonds from similarly rated corporate. Their returns also show strong relative value to the company’s international peers. With a significant cost saving program, strong liquidity and a major asset base (a number of which would be attractive acquisitions should the company require further cash injections) there are a number of positives for Qantas, despite the recent results, which helps make Qantas bonds one of the best high-yielding buys in the Australian bond market. © 2014 FIIG Securities Limited | ABN 68 085 661 632 | AFS Licence No. 224659 Revenue 7,903 590 EBITDA margin 7.5% Net debt 3,226 Net Free cash flow (358) Key financials ($m) FY13 to 30 June 2013 Revenue 15,902 Underlying EBITDA 1,822 EBITDA margin 11.5% Net debt 3,226 www.fiig.com.au | info@fiig.com.au The contents of this document are copyright. Other than under the Copyright Act 1968 (Cth), no part of it may be reproduced, distributed or provided to a third party without FIIG’s prior written permission other than to the recipient’s accountants, tax advisors and lawyers for the purpose of the recipient obtaining advice prior to making any investment decision. FIIG asserts all of its intellectual property rights in relation to this document and reserves its rights to prosecute for breaches of those rights. This research report should be read in conjunction with the disclosures and disclaimer in this report. Important disclosures regarding companies that are subject of this report can be found at the end of this document. Sydney | Melbourne | Brisbane | Perth FIIG Securities Limited | Page 1 of 6 FIIG Research Qantas Airways Ltd 24 April 2014 Background Qantas was founded in 1920 and has grown to be Australia’s largest domestic and international airline. Whilst the key business remains the transport of airline passengers, the Group has grown to include a number of complementary businesses. The Qantas Group consists of five business segments: Qantas domestic – where the company is a market leader in both the business and leisure markets through its duel brand strategy (Qantas and Jetstar) with the Qantas premium brand maintaining its dominance in its home territory Qantas international –Qantas’ traditional international business including its new strategic alliance with Emirates Airways Qantas freight – air freight business including Australia Air Express Jetstar – the largest low cost carrier in the Asia-Pacific with targeted investments in key markets in the world’s fastest growing region Qantas frequent flyer – Australia’s leading customer loyalty program with more than 8 million members Operations At the same time as the release of the half year (loss) result, the company announced a three year operational review which would seek to deliver $2bn in cost savings. Drivers of this $2bn cost saving will include: Head count reduction of 1,000 within 12 months (including 300 already announced) CEO and board pay cuts No bonuses for executives and pay freeze Review of suppliers....expect Qantas to take a Woolworths/Coles approach to suppliers Network optimisation....already Qantas have announced reduced services to Darwin, and increases in Adelaide to better align fleet utilisation Other overheads International turnaround The turnaround of the international operations business includes the exiting of unprofitable routes, rationalisation of catering and engineering operations, more efficient capital allocation, reconfiguring the fleet to enhance profitability and building better alliances including the continued strengthening of the Qantas-Emirates alliance. For the 2014 half year, underlying EBIT for Qantas International was a $262m loss (compared to a $91m loss for the first half of 2013). A slower global economy has seen considerable passenger seat volume moved to Qantas’ key international routes as has the addition of significant low cost and government backed competitors. This additional passenger seat volume has had the effect of lowering yields across the industry and placing significant negative pressure on pricing. Jetstar The Jetstar brand made an underlying loss of $16m for the half year compared to a $128m profit for the prior comparable period as the international Jetstar business was affected by the same supply/demand dynamics as the Qantas International business. All of Qantas’ business units were also affected negatively by unfavourable movements in fuel pricing and FX. In response, Qantas has slowed its growth program for Jetstar as it realigns its fleet with route demand. Jetstar’s domestic business remains profitable and is the largest low cost carrier in the Australian domestic market. © 2014 FIIG Securities Limited | ABN 68 085 661 632 | AFS Licence No. 224659 www.fiig.com.au | info@fiig.com.au The contents of this document are copyright. Other than under the Copyright Act 1968 (Cth), no part of it may be reproduced, distributed or provided to a third party without FIIG’s prior written permission other than to the recipient’s accountants, tax advisors and lawyers for the purpose of the recipient obtaining advice prior to making any investment decision. FIIG asserts all of its intellectual property rights in relation to this document and reserves its rights to prosecute for breaches of those rights. This research report should be read in conjunction with the disclosures and disclaimer in this report. Important disclosures regarding companies that are subject of this report can be found at the end of this document. Sydney | Melbourne | Brisbane | Perth FIIG Securities Limited | Page 2 of 6 FIIG Research Qantas Airways Ltd 24 April 2014 Qantas-Emirates The Qantas-Emirates tie up, a 10 year alliance, has a number of benefits to Qantas and its customers. For its customers, it provides one stop access to 33 European destinations (compared to five previously) and 31 one stop services to the Middle East and Northern Africa (none previously) as well as broader access for its frequent flyer program through a single partner. For the company, the benefits extend beyond the traditional code sharing model with commissions also available on nontrunk routes as well as providing a significant feeder for Qantas’ domestic business. The development of the alliance also allows Qantas to restructure its Asian business, an area of great potential growth, but also subject to increasing competition. This restructure will include fleet management (ensuring the most efficient aircraft for the route is utilised) and schedule management, with better timing of flights to suit customer requirements rather than designing flight schedules to meet end destination requirements in Europe. Trading results – Half year to 31 December 2013 Qantas Airways Limited (Qantas) announced a $254m loss for the first half. This loss was foreshadowed by CEO Alan Joyce in December when he provided a guidance update (guidance for the first half of a loss of between $250m to $300m). A number of industry fundamentals affected Qantas’ performance for the half (which also affected its competitor Virgin, which announced its own loss later in the week) including increased capacity in the domestic market placing pressure on pricing; uncompetitive cost base and work practices; high AUD and fuel costs and a distorted market place (that is Virgin’s foreign government ownership structure). In response Qantas announced it was accelerating its business transformation including staff cuts of up to 5,000 full time equivalents, adjusting its existing fleet including removal of older, less efficient aircraft and removal of unprofitable routes and a reduction in capital expenditure by delaying new aircraft acquisitions. The company is also exploring/undertaking a number of other options including the sale and lease back of terminal space. Revenue for the half was 4% down on the prior comparable period as continued competition and increased fleet capacity in the market led to subdued passenger yields for the half. Half year results $m 1H14 Net passenger revenue Net freight revenue Other revenue Total revenue Operating expenses Fuel Underlying EBIT Underlying profit (loss) 1H13 6,786 500 617 7,903 4,797 2,255 (156) (252) Variance % 7,042 475 725 8,242 4,770 2,181 307 220 -4% 5% -15% -4% -1% -3% - Source: FIIG Securities Liquidity Qantas maintains a strong liquidity positing with cash of $2.4bn and available facilities of $630m available at the end of the financial year. Further, the company has continued to adopt a proactive approach to refinancing ahead of schedule to maintain this liquid position as well as flexibility in its approach to capital expenditure (with capex reduced $400m for © 2014 FIIG Securities Limited | ABN 68 085 661 632 | AFS Licence No. 224659 www.fiig.com.au | info@fiig.com.au The contents of this document are copyright. Other than under the Copyright Act 1968 (Cth), no part of it may be reproduced, distributed or provided to a third party without FIIG’s prior written permission other than to the recipient’s accountants, tax advisors and lawyers for the purpose of the recipient obtaining advice prior to making any investment decision. FIIG asserts all of its intellectual property rights in relation to this document and reserves its rights to prosecute for breaches of those rights. This research report should be read in conjunction with the disclosures and disclaimer in this report. Important disclosures regarding companies that are subject of this report can be found at the end of this document. Sydney | Melbourne | Brisbane | Perth FIIG Securities Limited | Page 3 of 6 FIIG Research Qantas Airways Ltd 24 April 2014 FY13 and significantly higher capex reductions going forward in light of the recent half year loss), all of which are positives for credit investors. Net on balance sheet debt for the period increased to $3.83bn up from $3.23bn in the prior comparable period with gearing increasing similarly. The company has publically stated its intention to decrease its level of debt, a process which has been backed by recent actions, in particular the deployment of proceeds from the Groups asset swap with Australia Postal Corp (swapping Australian Posts share of domestic freight company Australia Air Express for Qantas’ share of StarTrack) and the cash benefit from the late delivery of Boeing Dreamliners to reducing debt ($650m). The cost reduction program being undertaken by the group should provide some scope for Strengths Qantas retains a dominant position in the Australian domestic airline sector with a market share of circa 65% across both its Qantas and Jetstar brands. Qantas maintains its dominance in the lucrative business passenger segment and continues to grow its corporate account numbers The company has introduced a duel branding strategy through the differentiation between Qantas, which offers a full cost service and Jetstar, its successful low cost carrier airline which has driven significant growth over recent years including its international expansion. The successful differentiation allows the Group to hold the largest market share in both the business and low cost ends of the Australian market simultaneously With $2.4bn in cash and a further $630m in available facilities Qantas maintains a very strong liquidity position. Its ability to defer significant capital expenditure can also provide further capacity over the short term The company has pursued a significant expansion program in Asia through its Jetstar brand and are now the largest low cost carrier in the Asia-Pacific region. The Jetstar Group remains well placed with its corporate structure and alliance through local shareholder partners providing a lower cost platform than is able to be achieved through the premium Qantas brand Despite the recent negative result, Qantas remains an asset rich business, with a number of significant entities and opportunities to reduce debt levels through asset sales available to management including the highly lucrative Frequent Flyer business which is valued in excess of $2bn (based on market commentary) Risks The nature of the airline industry presents a risk for bond holders due to it being cyclical, capital intensive and exposed to the cost of jet fuel which fluctuates with movements in the underlying commodity. Offsetting this is the long history of Qantas’ operations, its diversity across its two brands as well as the continued ownership of the frequent flyer business (which is separated in a number of its peers) and most importantly its dominant position in its home market The airline industry remains highly competitive with competition increasing both on the company’s domestic and international routes. In particular Qantas’ international business faces strong competition from government backed, or significantly government owned competition. Despite this Qantas has maintained its position in the domestic market and in fact has seen off a long list of domestic competitors. The sector increasingly looks like a duopoly with Virgin and we would expect to see some easing on the domestic competition front (with sporadic outbursts of competitive activity) as both Qantas and Virgin suffered losses over the first half of the 2014 financial year, a position which is unsustainable in the longer term for both competitors. The expansion of the low cost carrier model into Asia and the alliance with Emirates should also help defend the Group against international rivals Qantas’ international business has underperformed financially in recent years due in large part to the increase in competition which has come with the deregulation of routes and has been a financial drain on the group as a whole. The company has undertaken a significant process of transformation in this business, delivering more than half the expected $300m in improvements to date. The Group will need to continue to deliver on this transformative program in order to return this division to profitability © 2014 FIIG Securities Limited | ABN 68 085 661 632 | AFS Licence No. 224659 www.fiig.com.au | info@fiig.com.au The contents of this document are copyright. Other than under the Copyright Act 1968 (Cth), no part of it may be reproduced, distributed or provided to a third party without FIIG’s prior written permission other than to the recipient’s accountants, tax advisors and lawyers for the purpose of the recipient obtaining advice prior to making any investment decision. FIIG asserts all of its intellectual property rights in relation to this document and reserves its rights to prosecute for breaches of those rights. This research report should be read in conjunction with the disclosures and disclaimer in this report. Important disclosures regarding companies that are subject of this report can be found at the end of this document. Sydney | Melbourne | Brisbane | Perth FIIG Securities Limited | Page 4 of 6 FIIG Research Qantas Airways Ltd 24 April 2014 Conclusion Qantas remains one of the strongest brands in Australia and one of our best known internationally. Notwithstanding the recent poor result the company retains a significant asset base and a market capitalisation (at time of writing) of over $2.7bn which provides comfort for investors in the company’s ability to meet its commitments. The Qantas bonds currently show strong relative value compared to its international airline peers and other Australian corporate issuers. © 2014 FIIG Securities Limited | ABN 68 085 661 632 | AFS Licence No. 224659 www.fiig.com.au | info@fiig.com.au The contents of this document are copyright. Other than under the Copyright Act 1968 (Cth), no part of it may be reproduced, distributed or provided to a third party without FIIG’s prior written permission other than to the recipient’s accountants, tax advisors and lawyers for the purpose of the recipient obtaining advice prior to making any investment decision. FIIG asserts all of its intellectual property rights in relation to this document and reserves its rights to prosecute for breaches of those rights. This research report should be read in conjunction with the disclosures and disclaimer in this report. Important disclosures regarding companies that are subject of this report can be found at the end of this document. Sydney | Melbourne | Brisbane | Perth FIIG Securities Limited | Page 5 of 6