Fixed Income Securities - Open University of Mauritius

advertisement

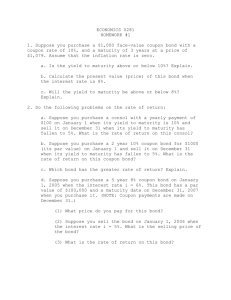

Fixed Income Securities Open University of Mauritius Bond features • Type of issuer (government & corporate) • Term to maturity • Principal Principal = face value, redemption value, maturity value, par value • Coupon rate Coupon rate = regular payment • Yield rate Open University of Mauritius Risks of investing in bonds • • • • • • • Interest rate risk Reinvestment risk Credit risk Inflation risk Exchange rate risk Liquidity risk Volatility risk Open University of Mauritius Example • Example of a simple interest based security: Bank-Bill FV P i n 1 100 365 – n = days to bill maturity – i = quoted yield (nominal % pa) for simple interest calculation – Apply 365 day year convention Open University of Mauritius Example • What is the price of a $100,000 90 day bank-bill with yield of 5.5%. Use simple interest for this security. 100000 P $98,661.98 5.5 90 1 100 365 Open University of Mauritius Longer term securities pricing of bonds • Generally pay regular coupon payments (c) with payment of the face value (FV) at maturity (T compounding periods hence) • Generally two 6-month compounding periods per year with coupons (c) paid at the end of each compounding period. • Coupon rate is a nominal rate pa. (5% pa. bond pays a 6 month periodic rate of 2.5% – or c = 2.5% x face value Open University of Mauritius Longer term securities pricing of bonds • If zero coupon bond then no coupons are paid and face value is received at maturity • The yield used to discount cash flows (yield or i) is quoted nominal rate pa. (i=6% pa gives a rate of 3% per compounding period) Open University of Mauritius Longer term securities and bond pricing • Securities are broadly classed as “long term” securities if term to maturity is longer than 12 months. • How do we price a bond at the beginning of the first coupon period? Open University of Mauritius Fixed interest bond • Price equals the present value of the: – face value of the bond paid at maturity (FV) – annuity of coupon payments (c) – Given yield (i) and time to maturity (T) c 1 1 i P i T FV T 1 i Open University of Mauritius Fixed interest bond • Example • 7%pa 3 year $100 bond with market yield of 8%pa 3.51 1 4 100 P 4 100 $97.379 per $100 6 100 6 1 4 100 Open University of Mauritius Zero coupon bond • Pricing a zero coupon bond at the beginning of a coupon period • Generally one payment at maturity and 6 monthly compounding FV P T 1 i Open University of Mauritius Zero coupon bond • 3 year zero coupon bond with yield 8% pa and 6 month compounding periods 100 P $79.031 per $100 6 1 4 100 Open University of Mauritius Price-coupon-yield • Par value $100, yield 4.5%pa, valued at beginning of coupon period, three bond types 5%pa coupon, 4.5%pa coupon, 3%pa coupon – Where c > i then P > FV – Where c = i then P = FV – Where c < i then P < FV Open University of Mauritius