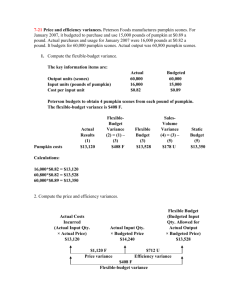

Chapter 14 Internet Exercise

advertisement