Price & Efficiency Variances: Cost Accounting Exercise

advertisement

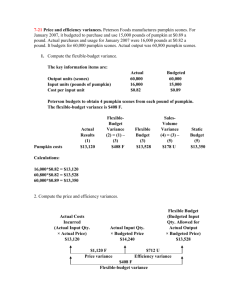

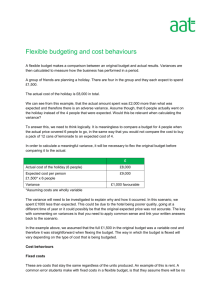

7-21 Price and efficiency variances. Peterson Foods manufactures pumpkin scones. For January 2007, it budgeted to purchase and use 15,000 pounds of pumpkin at $0.89 a pound. Actual purchases and usage for January 2007 were 16,000 pounds at $0.82 a pound. It budgets for 60,000 pumpkin scones. Actual output was 60,800 pumpkin scones. 1. Compute the flexible-budget variance. The key information items are: Actual 60,800 16,000 $0.82 Output units (scones) Input units (pounds of pumpkin) Cost per input unit Budgeted 60,000 15,000 $0.89 Peterson budgets to obtain 4 pumpkin scones from each pound of pumpkin. The flexible-budget variance is $408 F. Pumpkin costs Actual Results (1) $13,120 FlexibleBudget Variance (2) = (1) – (3) $408 F Flexible Budget (3) $13,528 SalesVolume Variance (4) = (3) – (5) $178 U Static Budget (5) $13,350 Calculations: 16,000*$0.82 = $13,120 60,800*$0.82 = $13,528 60,000*$0.89 = $13,350 2. Compute the price and efficiency variances. Actual Costs Incurred (Actual Input Qty. × Actual Price) $13,120 Actual Input Qty. × Budgeted Price $14,240 $1,120 F Price variance Flexible Budget (Budgeted Input Qty. Allowed for Actual Output × Budgeted Price) $13,528 $712 U Efficiency variance $408 F Flexible-budget variance 3. Comment on the results in requirements 1 and 2. The favorable flexible-budget variance of $408 has two offsetting components: (a) Favorable price variance of $1,120––reflects the $0.82 actual purchase cost being lower than the $0.89 budgeted purchase cost per pound. (b) Unfavorable efficiency variance of $712–-reflects the actual materials yield of 3.80 scones per pound of pumpkin (60,800 ÷ 16,000 = 3.80) being less than the budgeted yield of 4.00 (60,000 ÷ 15,000 = 4.00). (The company used more pumpkins (materials) to make the scones than was budgeted.) One explanation may be that Peterson purchased lower quality pumpkins at a lower cost per pound. Discussion Question 2 th • Resource: Cost Accounting (12 ed.) • Due Date: Day 4 [Main] forum • Complete Exercise 7-21 on p. 246. • Post your answers to the [Main] Forum as an attachment. • Answer the following question: How can determining the causes of these variances help the company improve? Determining the causes of variances would help the company improve as managers’ attention could be focused on problematic areas, if for example materials of higher quality are purchased at a higher price, such price increase should be taken into account when preparing the budget for the next period. If lower quality materials have been purchased, the purchasing manager should be advised not to use lower quality materials as this would result in a lower product quality. In the case of Quantity Variances could be a result from an unexpected machinery breakdowns, for example, hence managers would need to put a maintenance schedule for the machines to avoid such unpleasant problems. In the case of an Unfavorable Efficiency Variance which mostly result from hiring unskilled workers, management can start arranging training courses for such unskilled labor so as they achieve the company’s standards In short, all variances either favorable or unfavorable need to be investigated. A threshold may be fixed at say 5% and all variances above this should be investigated. The causes of the variances should be ascertained and the processes changed so as to ensure that the variances do no recur. If it is found that variances are due to incorrect standards in which case the standards themselves need to be changed.