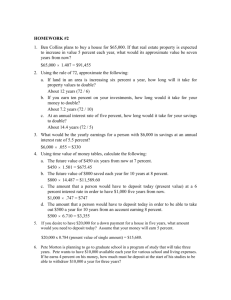

Deposit Interest Retention Tax

advertisement