Irish National Flood Forum Opening Statement

advertisement

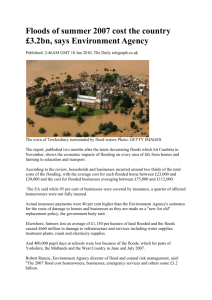

Irish National Flood Forum Ltd. Working for flooded communities in Ireland. Mr. Chairman, Committee Members, members of the Oireachtas, we thank you for inviting the Irish National Flood Forum here to Leinster House to brief you on OUR issues, as home-owners and Communities affected by flooding. The Irish National Flood Forum is a voluntary organisation made up of people and communities that have suffered from flooding and are at risk from flooding. In today’s presentation, I firstly intend to explain the situation as it is at present for homes across the country. Secondly, I discuss the question … are Insurance Providers in Ireland acting as a cartel to increase their profits from the Irish market at the expense of the Irish citizens. And finally, I will develop what we expect, you, our elected Oireachtas members to do for the citizens of Ireland. The Situation at Present. We know that people whose homes that have been flooded, are already suffering in that they cannot get insurance, and also, as their homes are no longer mortgageable, that the value of their houses have plummeted. Acknowledging this issue, the Revenue Commissioner, Ms. Josephine Feehily has confirmed to the Public Accounts Committee on Thursday 21st of February, that flooding will impact on Property Tax valuations. We hope that, with the Revenue Commissioners understanding the issue, it will enable the OPW to get further funding to speed up the Flood Relief programmes in Ireland. My colleagues will give many instances from Bandon, Clonmel, Cork, Dublin, Fermoy, Skibbereen where Irish Insurance providers are treating the Irish public badly. In a resent press release, the Irish Brokers Association, after analysing and collating data from insurers, the IIF (Irish Insurance Federation) and the IBA (Irish Brokers Association) own data from members all over the country, estimate that up-to 50,000 households have, or are at risk of no flood cover within the 26counties of the Republic of Ireland. The IBA observe the following in relation to the insurance provider’s use of Geo-coding:– “Geo-coding, although handy for insurance companies is not accurate and can leave vast swathes uninsurable, despite no history of flooding in the area. It can also ignore remedial works which have been put in place by the OPW and local authorities rendering the area far less prone to flooding” Even this committee understand, and are or the record stating that the practice of geo-coding of area’s by insurance companies must be reviewed. Furthermore, those who have a claim and lose or do not renew their cover, will never get cover again, under the current regime, as terms imposed by the previous insurer must be declared to all future insurers, plus a question on the proposal form asks – ‘are you in an area that has EVER flooded or if there is a history of flooding in the area’; and/or ‘is your house situated within 500metres of a river’. While we acknowledge the work of the OPW is flood prevention measures, which is, by it’s nature, slow, taking up-to 10years from inception to completion. We, the victims of flooding, CANNOT wait for the OPW. As Dr. Juliana MacLeod, a principal clinical physchologist with the HSE South has stated, the “long term issues/effects are influenced by both a sense of security (likelihood of the event happening again) and Insurance Issues ….. it is that important! It is as much a health issue as a financial issue. Are the Irish Insurance Providers (Companies) acting as a Cartel? WE ask, why do the Insurance Providers in Ireland, whose head offices are across Europe and America, threat the flooded public in Ireland differently from the public in their home countries? If you have a car crash of your home burns to the ground, are you excluded from ever having insurance cover? If your neighbour has a car crash or your neighbours home burns to the ground, are you excluded from ever having insurance cover? ….. this is the case with flood insurance cover in Ireland! If your neighbour has ever flooded, then the Irish Insurance providers will exclude you FOREVER from being able to obtain flood insurance. But was is more surprising, is all the Insurance Product Providers seem to be singing from the same hymn-sheet ….. in a competitive industry, they can all include the same exclusion safe in the knowledge that their competitors will also exclude the same. Just think, can you think of any other industry where every competitor a Product Provider have the same clause? What is another reason to believe that ALL the Insurance Providers are acting as a cartel is if you have made a claim. No provider will even quote you home insurance if you have made a claim in the previous five years ….. thus proving that there is NO COMPETITION in the provision of Insurance in Ireland. Can you think of any other business in Ireland where the public (who have mortgages) are required to buy Home Insurance but MUST buy the Insurance, at an inflated premium, off a single provider, because the providers “competitors” refuse to even quote for the business for a period of five years! A cartel is an explicit agreement among competing firms that agree to fix prices or production. Cartels usually occur in an industry where there is a small number of sellers. Cartel members may agree on such matters as price fixing, market shares, allocation of customers, allocation of territories, or combination of these. The aim of such collusion is to increase individual members' profits by reducing competition. We, also attach results of surveys which we have conducted in the various locations. An unusual statistic compiled the Irish Brokers Association, is that the majority of claimants who actually received a payment, were actually UNHAPPY with the level of support given by their Insurance company. Other statistics of note include that event though respondents have spent on average between €3,895 and €6,969 of their own money on flood mitigation measures, not one insurance provider asked, or took account of these mitigating measures when REFUSING flood insurance cover! During a flood event, the public come together to work for hours to protect property (mitigating any possible cost to Insurance companies), yet the Insurance companies it appears would prefer if you did nothing. We are encouraged that this Joint Oireachtas Committee understand this issue and have stated their objections, and I quote:“we have been told of instances where remedial work in tearms building or improved flood defences have been undertaken, and people in those areas still can’t get property insurance. This should not happen. This is not the forum to discuss the ‘aggressive position’ taken by Insurance Providers in relations to claims. Individual claimants being forced to employ ‘loss assessors or claims professionals’ to achieve realistic settlements, and then find that 30% to 35% of agreed sums are being retained. What we expect from our Elected Oireachtas Members! We ask you as legislators, to help the 50,000 homes, approximately 250,000 citizens of this state, who are being bullied by the insurance industry, who in this state are acting as a cartel, not price fixing, but agreeing to exclude 50,000 homes to increase their profits! We ask you as legislators, to show leadership, stand up for your constituents, and legislate for the insurance industry to abide by certain protocols, or a certification process to enable household to avail of private home insurance cover which includes flood cover! At present the Insurance providers in Ireland do not have to explain why they do not give cover, yet if your home is mortgaged, you are required to pay for insurance, which is weighted because of goeprofiling We need you as legislators to insist that if hydrologist calculate that an area has probable return period, then we want the Insurance Industry to be obliged to offer Flood Insurance cover. Low risk 1:150+ return period 100% cover. Moderate risk 1:75 – 1:150 return period. Individual. Significant risk Greater than 1:75 return period. No cover. This basic protocol would be transparent and helpful to the Insurance Industry, the OPW and the general public. We do not know where the current 5% Government levy on all general insurance policies is going. Prior to the extra 2% being added for the Quinn legacy in January 2013, all policies paid a 3% levy which went straight to Government for the past 15years. We are not asking for the Insurance Industry to subsidise the flood relief works of the OPW, even when it is obvious that the insurance industry would gain if they went into PPP on Flood Relief Schemes. We are asking for the Insurance Industry to take responsibility to explain to the public why they have not accepted the remedial works completed by the OPW that are helping resolve flood risk in many areas. We do not know where the current 5% Government levy on all general insurance policies is going. Prior to the extra 2% being added for the Quinn legacy in January 2013, all policies paid a 3% levy, which went straight to Government for the past 15years. What we are asking for, is could not a portion of this 5% Government levy be set aside for a flood disaster fund, similar to the proposal of Brendan Dempsey of the Saint Vincent de Paul for those flood victims, who want to purchase, but are excluded from, flood insurance cover. See attached proposal ‘A’ for how this pilot project maybe rolled out. Finally, I wish to introduce my collegues, Michael Thornhill – Skibbereen Floods Committee; Cllr Joe Leahy from Clonmel; Gillian Powell – Bandon Community Flood Group; I also wish to thank the following for their help in this proposal, namely Brendan Dempsey (Cork president of the Saint Vincent de Paul) who is present here, and his interesting colleagues! My colleagues, Skibbereen Floods Committee, and Anne Kelleher from the Dodder Flooding Group. Thank you for your time, and we now ask you for any questi ons, that you may have?