Allais`s gambles

advertisement

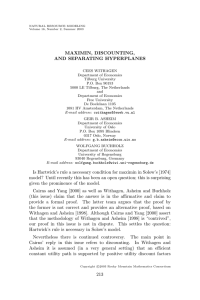

Allais’s gambles probability matrix 2500000 0 0.1 0 0.1 A B C D 500000 1 0.89 0.11 0 0 0 0.01 0.89 0.9 desirability matrix 2500000 2500000 2500000 2500000 2500000 A B C D A B C D 500000 500000 500000 500000 500000 0 0 0 0 0 0 2500000 + 1 500000 + 0 0 = 500,000 0.1 2500000 + 0.89 500000 + 0.01 0 = 695,000 0.11 500000 + 0.89 0 = 55,000 0.1 2500000 + 0.9 0 = 250,000 According to the expected utility principle, it is irrational to choose A and D. Proof: 2500000 x x x x A B C D A B 500000 y y y y 0x+1y+0z=y 0.1 x + 0.89 y + 0.01 z = ... 0 z z z z C D 0.11 y + 0.89 z = ... 0.1 x + 0.9 z = ... y > 0.1x + 0.89y + 0.01z 0.11y +0.89 z < 0.1x + 0.9z 0.1x – 0.11y + 0.01z < 0 0.1x – 0.11y + 0.01z > 0 Ellsberg paradox Option 1 Option 2 Red 100 0 Black 0 100 Yellow 0 0 Option 3 Option 4 Red 100 0 Black 0 100 Yellow 100 100 Option 1 Option 2 Option 3 Option 4 Red 1/3 1/3 1/3 1/3 Black x x x x Yellow y y y y According to the expected utility principle, it is irrational to choose 1 and 4. Proof: 12 43 0 x 2/3 0 y 2/3 x + y = 2/3 1: 2: 3: 4: 100 1/3 100x 100 1/3 + 100y 100 1/3 + 100x 100 1/3 > 100x 100 1/3 + 100x > 100 1/3 + 100y x < 1/3 x>y y < 1/3 Both x and y are less than 1/3, but their sum is 2/3. This is inconsistent. Where do the probabilities come from? Expected utility has two components: probabilities and utilities. 1. Utility measures to some extent the value that an agent assigns to a given outcome. We take utility to be subjective, in the sense that there is no right or wrong utility to be assigned to a given outcome. (Hume said: “It is rational to prefer the destruction of world to the scratching of one’s finger.”) 2. The standard theory of subjective expected utility also takes an agent’s probability assignments to be subjective. Subjective probabilities 1. Is it irrational to play in the state lottery? Suppose I believe that my chance of winning $1,000,000 is 50%. Clearly I should spend the $1 to buy the ticket then. According to what we said so far, there is nothing irrational about that. 2. Intuitively, what is wrong in the above example is that my subjective ideas of how likely I am to win in the lottery don’t match the real chances of my winning. 3. So often philosophers add a principle to maximizing expected utility called the direct inference principle: If you know that the objective chance of an event is p, your subjective probability of the event should be p also. Another example is insurance. When an insurance company estimates how much you should pay for car insurance, you don’t want them to go by the insurance agent’s personal estimate of how likely you are to have an accident. You want them to estimate the actual chance of having an accident by looking at other people in your age group, driving record, etc. Uncertainty and the maximin principle 1. Consider the question of whether we should build a nuclear power plant in our neighborhood or not. Use matrices to represent the decision problem. Sometimes proponents of nuclear power say that opponents are ‘irrational’. One thing they might mean is that opponents give too much weight to unlikely worst-case scenarios. We could suspect that the opponents use the maximin principle rather than the ‘rational’ principle of maximizing expected utility. 2. Some philosophers and decision theorists have made a good case that the maximin principle should be used when There is a lot of uncertainty about what the real chances are. There is a lot at sake (death, nuclear contamination). 3. An appealing variant of the expected utility theory is this: First, rule out options whose worst case is below a minimum acceptable level called the security level (e.g. I don’t take a risk on dying). Second, use expected utility to choose among the remaining options. On this account of rational choice it is rational to decide against nuclear power. 4. Apply this theory to the Ellsberg paradox. Games in Matrix Form