Introduction to accounting using Monopoly board

advertisement

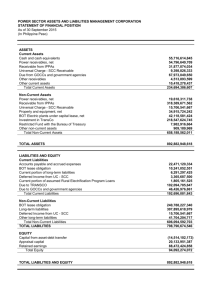

Introducing Students to Financial Accounting Using Monopoly© Board Game: A Teaching Note. Learning Outcomes Students should be able to: 1. distinguish between income, expenses, assets, liabilities and capital 2. record each transaction twice on formatted work sheets 3. transfer their workings to formatted financial statement sheets 4. appreciate the integrated nature of the financial statements 5. talk to at least 18 other students. Timing and Assessment The Monopoly© games extend over the first 6 weeks of first year. The last game carries a 10% continuous assessment weighting (level 7 degree, year 1 module, 10 credits). Materials Needed 1. Monopoly© game for every four students 2. formatted worksheets and financial statement sheets for each student (see Appendix 1 – I customise these sheets to the needs of each student cohort) 3. flat class room with tables and chairs 4. computer projector, board or flip chart. Typical Class 1. groups (of 4) are randomly selected each week 2. game starts 3. game generates the transactions which students have to record 4. lecturer helps students in difficulty 5. lecturer can generate transactions, using a computer projector, e.g. 'bank lends you €500’ 6. game lasts for c. 25 minutes. Students compare their cash and properties with their worksheets. Game is packed away. 7. 10 minute break 8. students total their worksheets and transfer information from their worksheets to their financial statements. 9. financial statements are totalled and hopefully balance. Benefits of Monopoly® 1. soft introduction to accounting. Many students perceive accounting as a boring / difficult subject. Use of this game can change this perception in some cases 2. attendance improves by approximately 10% compared to conventional classes 3. students enjoy the social nature of the game. Students tend to help one another to record the game. Some students are attracted by the competitive element of the game. 4. many students grasp the integrated nature of the financial statements which is a threshold concept for financial accounting 5. the degree of difficulty can be increased through the gradual introduction of transactions such as loans, depreciation etc 6. decision-making can be introduced by asking students to predict the eventual winner based on financial statements at the half-way point. Challenges 1. when the class size exceeds 32 (or 8 games), it can be difficult to help struggling students 2. scarcity of tables in class-rooms 3. significant advance preparation in the design and copying of work-sheets and financial statements to meet student needs 4. keeping student focus on the recording, as well as the playing of the game 5. linking of the formal classes to the student experience during the games. Conclusion I have found this approach to be an effective, flexible and sociable approach for students who are new to financial accounting. I am very grateful to Mr. Clayton (2003) for prompting me to try this approach. Please contact me, contact details below, if you have any questions. Source for this approach Clayton, G. (2003) Using Monopoly© as an introduction to financial accounting. In Kaye, R. & Hawkridge, D. (ed.) Learning & Teaching for Business. London : Kogan Page. __________________________________ Conor Heagney Senior Lecturer in Accountancy & Finance School of Business & Humanities Dun Laoghaire Institute of Art, Design & Technology Kill Avenue, Dun Laoghaire, Co. Dublin. Email: conor.heagney@iadt.ie Phone: 01 – 2394 753 June 2010. Appendix 1 Sample Worksheets & Financial Statements for Students Meanings of Some Accounting Words (aid to students during game): 1. Assets - something bought by the business where the benefit is in the future. Assets are further split into current assets where the benefit is soon and noncurrent assets where the benefit can be spread over a long time. An example of a current asset is cash. An example of a non-current asset is a hotel. 2. Capital – money that the business owes to the owner. 3. Liabilities – money that the business owes to everyone other than the owner. Liabilities are further split into current liabilities which should be paid soon and non-current liabilities which do not have to be paid for a good while. Accounting Equation: Assets = Capital plus Liabilities. 4. Balance Sheet – an accountant’s way of showing the accounting equation at one point in time. A balance sheet is often compared to a financial photo of a business. 5. Income – something that makes the business worth more to you (the owner). Examples are ‘pass go’ income and income from rent. 6. Expenses – something bought by the business where the benefit is now or in the past. Examples are rental expenses and tax. 7. Profit and Loss Account – a page showing the effects, over a period of time, of income and expenses on Capital. 8. Cash Flow Statement – a page showing where cash came from and where cash went, over a period of time. 9. Depreciation – part of the cost of non-current assets that is used up in making sales. Worksheet 1. Cash Movements of (enter student name) Cash In + Cash at start Income Liabilities (bank loan) Expenses Assets Cash at end (total of above rows) Cash at end (count) for the Game. Cash Out - End of Game 1,500 Worksheet 2. Profit & Loss Account of Income for the Game. Totals at end of Game ‘Pass Go’ income Rental income ‘Chance / Community Chest / Free Parking / Profit on sale of street/Other’ Income Less Expenses Rental expenses ‘Chance / Community Chest / Jail / Loss on sale of street/Other expenses Depreciation Interest expense Tax expense Worksheet 3. Balance Sheet of at the end of the Game. Assets Land (sites – enter street name) Buildings (enter street name - number of houses / hotel) Depreciation Cash (see bottom of worksheet 1) Less Liabilities Short-term loans to your business Totals at end of Game Final Financial Statements 1. Profit & Loss Account of Income for the Game. € € ‘Pass Go’ Rental ‘Chance / Community Chest / Free Parking’ Income Total income Less Expenses Rental ‘Chance / Community Chest / Jail / Other’ Expenses Depreciation Interest Total expenses Net profit before tax Less tax Net profit after tax Total income less total expenses Final Financial Statements 2. Balance Sheet of at the end of the Game. Non-current assets Land (street name and cost) Buildings (street - number of houses / hotel and cost) Land & buildings at cost Less depreciation Total non-current assets Current assets Cash Total assets (add non-current & current assets) Opening Capital (capital at beginning of game) Add net profit after tax (see profit & loss account) Closing capital (capital at end of game) Current liabilities Loans from bank Total capital and liabilities 1,500