Comprehensive Exam Fall 2002

advertisement

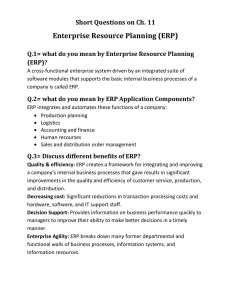

Fall 2008 – Comprehensive Exam Accounting Theory and Information Systems Part I Your comprehensive exam for Accounting Theory consists of two parts. First, you will answer any two (2) of the short-answer questions. Please keep your answers between one (1) and two (2) paragraphs. Your answers to the short-answer questions will be graded for content only, so please do not spend excessive time editing your writing. Second, you will answer any one (1) of the essay questions. Your answer should be long enough to cover the topic, but you will be penalized for including superfluous information. While demonstrating knowledge is a significant portion of your grade on this question, the quality of your writing and critical thinking will also be included, so you may wish to leave sufficient time for editing your answers. To aid in the grading process, please remember to include your test ID number and the page number in the upper right hand corner of each page. Also, make sure that you start each answer on a new page. Accounting Theory Questions Short Answer questions (answer any 2 of the following questions; please keep your answers to 1-2 paragraphs) 1. The 'ideal world' is based on a series of extreme assumptions. Please choose one of those assumptions and explain it to my grandma. Assume, correctly I might add, that my grandma doesn't really understand anything about accounting or formal economic theory. In order to receive full credit, you will need to keep your assigned audience in mind. 2. What is decision theory and how can it be useful for the accounting profession? Explain. 3. There are many incentives for managers to voluntarily disclose information instead of being forced to do so by regulation. List one of these motivations and briefly explain how it encourages managers to release accounting information. Essay questions (answer 1 of the following questions) 1. The U.S. is currently considering accepting IFRS instead of continuing with our current U.S. GAAP. Write a letter to the SEC chairman explaining why you feel this would (or would not) be a good idea. Support your position with at least four (4) strong arguments based on our in-class discussions of standard setting, earnings managements, academic research, and IFRS/U.S. GAAP differences. At least two (2) of your arguments must come from our readings. 1 2. What is the fundamental purpose of accounting? As a profession, is accounting currently fulfilling that purpose? Support your position (on both questions) with at least four (4) examples from our discussions of the history of accounting and other applicable topics, papers about our current status as a profession, academic articles and findings, etc. In addition to the examples from our class, you may also include examples of current accounting issues. Accounting Information Systems Question 1 – Everyone must answer Enterprise resource planning systems have been a leading concern of CIOs and CPAs over the last decade. Firms adopt ERP to increase their competitiveness in an increasingly demanding market place. Your boss just had lunch with a colleague who ‘s company recently installed an ERP system. He/She has asked you to prepare a report on ERP, its features and benefits, costs and risks. Demonstrate your understanding of ERP systems in a report to your boss. He/She will expect accurate content, critical thinking and professional writing style. Your answer should address the following issues at a minimum: What is ERP? How will it help our business? What are its costs (identify the types of costs, I’m not looking for a specific number)? What are its risks? What will be the impact on our organization and employees? What is ERP II (also called extended ERP) and how might it affect my business? Choose one: Q2 or Q3 (2-3 paragraphs max) Question 2 Identify the types of controls that should be present in most transaction processing systems. These controls are summarized in COSO and SAS 78. Question 3. Explain what REA means, why it is helpful to accountants, and how it can be used to assist in designing data bases. 2