Forecasting Chapter5

advertisement

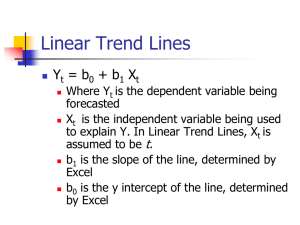

Chapter 5 Time Series and their Components What are seasonal effects? Trading day ; the number of working or trading days in a given month differs from year to year which will impact upon the level of activity in that month Moving holidays ; the timing of holidays such as Easter varies What is seasonality? Natural Conditions ; weather patterns Business and Administrative procedures ; school term Social and Cultural behavior ; Christmas Trading Day Effects ; the number of weeks in that month Moving Holiday Effects ; holidays whose exact timing shifts The Irregular (the residual) Short term fluctuations Neither systematic nor predictable Trend long term movement without calendar related and irregular effect the result of influences such as population growth, price inflation and general economic changes The Underling Models Used to Decompose the Observed Time Additive Decomposition Observed series = Trends+Seasonal+Irregular Seasonal adjusted series = Observed series-Seasonal = Trend+Irregular Multiplicative Decomposition Observed series = Trend*Seasonal*Irregular Seasonal Adjusted series = Observed/Seasonal = Trend*Irregular Pseudo-Additive Decomposition O = T + T * (S-1) + (I-1) = T * (S + I – 1) Adjusted ; SA = O – T * (S-1) = T * I How do I know which Decomposition Model to use? The magnitude of the seasonal component is relatively constant regardless of changes in the trend > Additive model It varies with changes in the trend > Multiplicative model The series contains values close to or equal to zero, and the magnitude of seasonal component appears to be independent upon the trend level > Pseudo-additive model Seasonal and Irregular (SI) Chart Determining whether short-term movements are caused by seasonal or irregular influences To identify Seasonal Breaks, Moving Holidays patterns, and Extreme Values in a time series Using Trend Projection in Forecasting 𝑇̂𝑡 = predicted value for the trend of the time series at time t T(t) = 𝑏0 + 𝑏1 𝑡 𝑏0 = intercept of the trend line = 𝑌𝑡 = 𝑏1 𝑡 𝑏1 = 𝑚 = (∑𝑡∑𝑌𝑡 ) 𝑛 (∑𝑡)2 2 ∑𝑡 − 𝑛 ∑𝑡𝑌𝑡 − 𝑌𝑡 = 𝑎𝑐𝑡𝑢𝑎𝑙 𝑣𝑎𝑙𝑢𝑒 𝑜𝑓 𝑡ℎ𝑒 𝑡𝑖𝑚𝑒 𝑠𝑒𝑟𝑖𝑒 𝑎𝑡 𝑝𝑒𝑟𝑖𝑜𝑑 𝑡 t = time which is a independent variable n = number of periods in time series SSE = ∑(𝑌𝑡 − 𝑇̂𝑡 )2 Quadratic Trend : 𝑇̂𝑡 = 𝑏0 + 𝑏1 𝑡 + 𝑏2 𝑡 2 Exponential Trend : 𝑇̂𝑡 = 𝑏0 𝑏1 𝑡 Minitab : (Stat > Time Series > Trend Analysis)