Chapter 9 t/f and m/c

advertisement

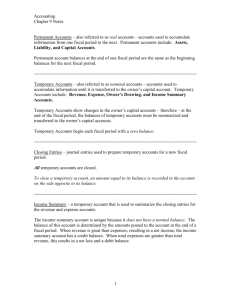

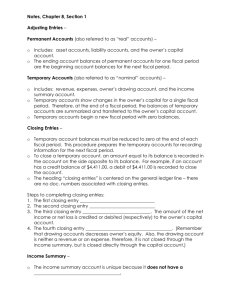

Chapter 9 ACCOUNTING Name ___________________________ 1. The income summary account balance must be reduced to zero to prepare the account for the next fiscal period. 2. The ending account balances of permanent accounts for one fiscal period are the beginning account balances for the next fiscal period. 3. All accounts in a general ledger are listed on a post-closing trial balance. 4. At the end of a fiscal period, the balances of temporary accounts are summarized and transferred to the owner’s capital account. 5. Permanent accounts are also referred to as temporary accounts. 6. The capital account’s new balance after all closing entries are posted is verified by checking it with the amount of capital shown on the balance sheet at the end of the fiscal period. 7. Adjusting entries are recorded on the next journal page following the page on which the last daily transactions for the month are recorded. 8. Preparing a worksheet at the end of each fiscal period to summarize the general ledger information needed to prepare financial statements is an application of the accounting concept Accounting Period Cycle. 9. A source document is prepared for closing entries. 10. To close a temporary account, an amount equal to its balance is recorded in the account on the side opposite to its balance. 11. Temporary accounts must start each fiscal period with a zero balance. 12. Permanent accounts must start each fiscal period with a zero balance. 13. Journal entries used to prepare temporary accounts for a new fiscal period are closing entries. What was the main purpose of Chapter 9’s instructions on Closing Accounts? Please explain using full sentences. Have enough information for 3 points (that’s about 3 sentences.) 1. __________ 2. __________ 3. __________ 4. __________ 5. __________ 6. __________ 7. __________ 8. __________ 9. __________ 10. _________ 11. _________ 12. _________ 13. _________ Chapter 9 ACCOUNTING Name ___________________________ 1. The journal entry to close the expense accounts is: a. Debit Income Summary; credit owner’s capital b. Debit Income Summary for the total expenses; credit each expense account. c. Debit each expense account; credit Income Summary. d. None of these. 2. The last step in the accounting cycle is to: a. Analyze transactions and journalize and post them. b. Journalize and post the closing entries. c. Prepare a worksheet and financial statements. d. None of these. 3. Adjustments are analyzed and planned: a. On a work sheet b. On the financial statements c. In the ledgers d. None of these 4. Temporary accounts begin each new fiscal period with a a. Zero balance b. Credit balance c. Debit balance d. Balance equal to the net income 5. The journal entry to adjust Prepaid Insurance is: a. Debit Insurance Expense; credit Income Summary b. Debit Prepaid Insurance; credit Insurance Expense c. Debit Insurance Expense; credit Prepaid Insurance d. Debit Income Summary; credit Prepaid Insurance. 6. Which accounting concept applies when expenses are reported in the same fiscal period that they are used to produce revenue? a. Adequate Disclosure b. Matching Expenses with Revenue c. Going Concern d. Business Entity 7. Adjustments are analyzed and planned a. On a worksheet b. On the financial statements c. In the ledgers d. None of these 8. After the adjusting entry for Supplies has been posted, Supplies Expense has an up-to-date balance, which is the a. Value of supplies bought during the fiscal period b. Same as the ending balance for supplies c. Value of supplies used during the fiscal period d. Same as the beginning balance for Supplies 9. When the total expenses are greater than the total revenue: a. Debits equal credits b. The income summary account has a debit balance c. The income summary account has a credit balance d. None of these 1. __________ 2. __________ 3. __________ 4. __________ 5. __________ 6. __________ 7. __________ 8. __________ 9. __________ Chapter 9 ACCOUNTING Name ___________________________