Accounting Cycle Closing Entries for Sole Proprietorships

advertisement

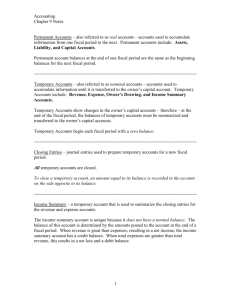

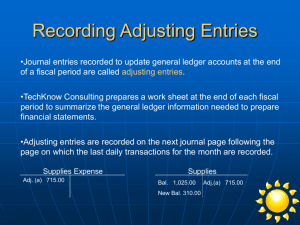

Completing the Accounting Cycle for a Sole Proprietorship Chapter 10 The Last Two Steps of the Accounting Cycle • Journalize and Post Closing Entries – Journal entries made to close, or reduce to zero, the balances in the temporary accounts and to transfer the net income or net loss for the period to the capital account • Prepare a Post-Closing Trial Balance – Trial Balance prepared after temporary accounts are brought to zero and capital has been adjusted accordingly Pg 250 The Process of Closing Entries Pg 251 1. Prior to the closing process, you know that the net income or net loss is calculated on the work sheet 2. The net income or net loss amount then appears on the income statement 3. On the statement of changes in owner’s equity, the ending balance of the capital account includes net income or net loss 4. The ending balance of the capital account then appears on the balance sheet 5. At this point, however, the balance of the capital account in the general ledger does not equal the amount on the balance sheet because the closing entries need to be journalized and posted Pg 252 Pg 252 The Income Summary Account • The Income Summary Account is used to accumulate and summarize the revenue and expenses for the period. – Expenses, which have debit balances, are transferred as debits to Income Summary – Revenues, which have credit balances, are transferred as credits to Income Summary – The balance in the account equals the net income or net loss for the fiscal period Pg 253 Income Summary T Account Income Summary Debit Credit Expenses Revenue If Revenue >Expenses If Revenue < Expenses Balance is net income Balance in net loss Pg 253 General Journal Closing Transactions Pg 254 - 256 Closing Income Summary to Capital • Once all transactions for Revenue and Expenses have been journalized, Income Summary has a balance. If there was a net income the Income Summary Account should have a credit balance. If there was a net loss, Income Summary should have a debit balance • The balance is then offset with the Capital account opposite to what the current Income Summary balance is. The idea is to bring the account to a zero balance. Pg 257 Pg 257 Closing Withdrawals to Capital • Withdrawal accounts usually have a debit balance so to close them you off set with a credit and debit to Capital Pg 258 General Journal of Closing Entries Pg 258 Posting the Closing Entries to the General Ledger Pg 260-261 Post-Closing Trial Balance Pg 262 • 9th & Final Step in the Accounting Cycle – Prepared to make sure total debits equal total credits after the closing entries are posted.