In recent years there have been more and more indications

advertisement

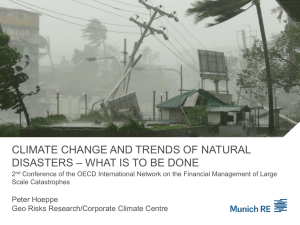

Adaptation to Climate Change: Climate Insurance Solutions for Developing Countries Peter Hoeppe Geo Risks Research, Munich Re, Munich In recent years there have been more and more indications that climatic change is already influencing the frequency and intensity of natural catastrophes. According to the World Meteorological Organisation (WMO), the last six years (2001 to 2006) were among the seven warmest recorded worldwide since 1861. A study performed by MIT and published by K. Emanuel shows that, since the 1970s, major tropical storms both in the Atlantic and the Pacific region have increased in duration and intensity by about 50 percent.1 Due to anthropogenic global warming the sea surface temperatures have increased already in all major ocean basins by 0.5°C 2. The year 2005 set a record for hurricanes in the North Atlantic: never before since records have been kept (1850) have so many named tropical storms 27 (old record 21) and hurricanes 15 (old record 12) developed in one season. In just one season the strongest (Wilma), fourth strongest (Rita) and sixth strongest (Katrina) hurricane have been recorded. From the NatCatSERVICE database of Munich Re with more than 25,000 natural disasters documented, we learn that the frequencies of world wide large natural catastrophes have tripled since 1950. Currently the frequency of all natural loss events has increased just during the last 25 years by a factor of 2.5 for floods, a factor of 2 for windstorms and a factor of 4 for other weather related events like heat waves, droughts, and forest fires. In contrast the frequency of loss events from geophysically caused perils like earthquakes, tsunamis and volcano eruptions has risen only slightly. The latter small increases most probably are due to socio-economic factors like more people living in risk prone areas. The difference between the increases in loss event originating in the atmosphere versus such originating in the earth points to changes in the hazard conditions in respect to extreme weather and thus to changes in the atmosphere. Global warming is the most dominant atmospheric change. There is also more and more evidence from scientific studies that there is a causal link between global warming and increasing extreme weather events. If the scientific global climate models are correct, the present problems will be magnified in the near future. These models suggest that we should expect: increase in the frequency and severity of heat waves, droughts, bush fires, tropical and extra tropical cyclones, tornados, hailstorms, floods and storm surges in many parts of the world new exposures (like hurricanes in the South Atlantic or Northeast Atlantic) more extensive damage, economic, social, and environmental impacts from weather-related disasters The 4th assessment report of IPCC published recently backs such projections. Insurance-related mechanisms can be an effective part of adaptation strategies as already indicated in article 4.8 of the framework convention and article 3.14 of the Kyoto Protocol. They can reduce the financial risks of an increasing number of natural catastrophes. As the frequency and scope of losses due to major weather related natural catastrophes will continue to increase, there is a growing need to explore options for managing and transferring risks associated with it. The mounting and highly unpredictable losses from natural disasters make traditional disaster funding approaches obsolete creating problems to finance economic recovery from the budget revenues or special government disaster funds of the countries affected. This is particularly the case in developing countries where limited tax bases, high indebtedness prevent them from relying on debt financing of reconstruction efforts. Hurricane Ivan in 2004 e.g. has caused losses in Grenada as high as 200% of the country’s annual GDP. Statistics of OECD and the World Bank show that despite a common belief, disaster-related external donor aid to developing countries accounts for only a small fraction of the total economic loss, caused by catastrophic events. Developing countries are most vulnerable to climate change effects, but have not contributed to the causes of global warming as they do not emit relevant amounts of greenhouse gases and have not dome so in the past. In other words, they are exposed to an increasing risk others have caused. 1 2 EMANUEL, K. (2005): Increasing destructiveness of tropical cyclones over the past 30 years. Nature 436, 686-688. (Barnett et al., Science 2005; Santer et al., PNAS, Sept. 2006) Another problem for developing countries besides not having enough revenue to cope with material losses, is the lack of a functioning insurance market to transfer at least part of the risk and in many places also a lack of an insurance tradition and understanding of the mechanisms. However, even if there were an insurance market the people in these countries would not have the money to pay for risk adequate insurance premium. This has been the motivation to found the Munich Climate Insurance Initiative (MCII) in 2005 in Munich as a joint initiative of representatives from IIASA, Germanwatch, Munich Re, Munich Re Foundation, Potsdam Institute for Climate Impact Research (PIK), UNFCCC, United Nations University Institute for Environment and Human Security (UNU-EHS), World Bank, and independent experts. We think that there is a responsibility of the industrialized countries to support insurance related systems for the increasing damages and losses in developing countries. MCII strives to fulfil four objectives: 1. Develop insurance-related solutions to help manage the impacts of climate change, seeking to combine the resources and expertise of the public and private sectors. 2. Conduct and support pilot projects for the application of insurance-related solutions in partnerships and through existing organisations and programmes. Identify success stories and disseminate information on the factors that are necessary to design and implement effective climate insurance-related mechanisms. These activities will focus on developing countries but at the same time will involve evaluating insurance solutions that have been used in developing countries. 3. Promote insurance-related approaches in cooperation with other organisations and initiatives within existing frameworks such as the United Nations system, international financial institutions, international donors, and the private sector. 4. Identify and promote loss reduction measures in connection with climate-related events. Insurance in its classical sense only can cover unforeseeable sudden events, like landfalls of hurricanes or floods caused by heavy precipitation events, but not foreseeable long term changes like sea level rise. For the latter other compensation mechanisms must be set in place. As the developing countries cannot afford to pay premium for such an insurance themselves, and in respect to the aspect of causality they also should not have to do so, one solution could be that the industrialized countries pay at least part of these premiums by contributing money into a pool according to their current or accumulated CO2-emissions. Precondition of the development of a climate change insurance system for developing countries is the quantification of the increases in weather related hazards on a regional basis and the respective proportion of the attribution to global warming. The latter currently still is an almost unsolvable task, probabilistic approaches could help to get at least some rough estimates. Probably the attribution assessment has to be based on a consensus between the premium payers and the insurance beneficiaries. Pricing and definition of indemnification plans of such a climate insurance system could be elaborated by re-insurance experts. In order to keep a pure climate change insurance system manageable, it should only cover large loss events (threshold to be defined), but both sovereign as well as individual losses should be included. Being based on a compensatory scheme, the system cannot cover the whole amount of losses due to weather related disasters as only part (currently certainly relatively small, but probably increasing) can be attributed to global warming. There are two ways to limit indemnification to these additional losses: - to indemnify all losses but only of real extreme events (beyond a certain percentile of the historic distribution) or - to only indemnify a certain percentage (representing the average global warming contribution) of the losses Indemnification should be linked to prior implementation of adaptation measures having been defined by the authority managing the climate insurance pool. A certain percentage, e.g up to one third, of the money out of the insurance pool should be assigned to such measures. Recent scientific results show, that every dollar invested in prevention pays back many fold in loss reductions.