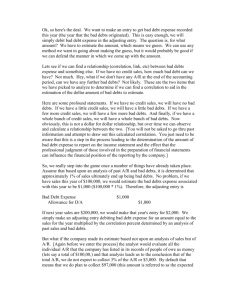

Receivables

• Setting credit policies

• Accounting for bad debt

• Computing interest

Setting credit policies

• Why sell on credit ???

– Increase sales ???

– To remain competitive

Setting credit policies

• Should I sell on credit to you?

– Credit department

• Approve credit sales

– Small businesses

• Generally prefer credit cards

– In effect, company’s credit department

– Credit scoring for individuals

• If denied credit, can get free copy of credit report

– Want stability

– Don’t apply for a lot of cards at the same time

• Credit reports can impact job, rental, life insurance

Bad Debts and Valuing A/R

• Bad debts: an expense of selling on credit

– It should be matched with sales period that

generate bad debts (matching principle)

– If no bad debts…

Methods of recording bad debt

expense

• Direct charge-off: record expense at the

time you find you won’t be paid

– Entry

• Bad Debts Expense

•

A/R

– Acceptable for income tax purposes

– Not acceptable for GAAP as violates matching

principle

Allowance Method

• Bad debt expense is matched against

sales in period the sales were recorded

– Losses must be estimated since companies

don’t know in the period of sale which

account will go bad

• Should take into account prior experience and

current economic conditions

• Must be realistic

• Subject to manipulation ???

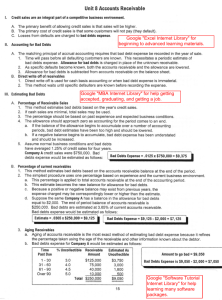

ADA

• On balance sheet

– Caterpillar

– A/R

– - ADA

5,611

- 376

Allowance Methods

•

•

•

•

Percent of sales method

Net sales x % bad debt

For example, $1 million x 5%

Then make this entry

– Bad debts expense

–

ADA

$50,000

$50,000

• Focus: income statement, not balance sheet

• Not concerned about ADA balance

Allowance Methods

• A/R aging method

• A/R is aged

– Further past due, likelihood of bad debts grows rapidly

•

•

•

•

• For example, 4% of < 30 days; 40% over 90 days

Multiply A/R x % bad debt for each time period

Calculate total balance needed in ADA

Assume need $50,000 and $20,000 already in ADA

Then make this entry

– Bad debts expense

–

ADA

$30,000

$30,000

• Focus: balance sheet, not income statement

• Not concerned about Bad Debts expense

Entry for write-off of A/R

• Already recorded expense when estimated bad

debts expense under one of allowance methods

– Entry:

• ADA

•

A/R

– Reduces ADA and A/R

– Net A/R remains the same

– If underestimate bad debts, ADA will have a debit

balance

Credit Cards

• VISA and MasterCard

– Credit card slips are similar to depositing

checks into company bank account

– Discount may range from 2-4%

– Entry

• Cash

• Credit card expense

•

Sales

98

2

100

Credit Cards

• Factoring

– Sale of receivables

– With recourse?

– Cost of funds?

Credit Cards

• Store credit card

– No discount fees

– Entry

• A/R

•

100

Sales

100

Gift Cards

• Store gift cards

– Stores love these

– Entry

• Cash

•

?????

– On expiration date

100

100

Notes Receivable

• Promissory note versus A/R

• A/R

– No interest

– Unsecured creditor

• N/R

– Interest

– Secured creditor

Calculating Interest

• Principal x Rate x Time

• Principal = amount loaned

• Make sure time and rate are expressed in

same units

• Interest on $1,000 for 30 days at 10%

– 360 day versus 365 day method

0

0