Module 2

INTEREST & MONEY – TIME

RELATIONSHIPS

Engr. Gerard Ang

School of EECE

Simple Interest

Interest – is the return on capital

or cost of using capital. It is the

amount of money paid for the

use of borrowed capital or the

income produced by money,

which has been loaned.

Simple Interest – is calculated

using the principal only, ignoring

any interest that had been

accrued in preceding period.

𝐈 = 𝐏𝐢𝐧

𝐅=𝐏+𝐈

𝐅 = 𝐏(𝟏 + 𝐢𝐧)

Where:

I = interest

i = rate of interest

n = number of interest period

P = principal or present worth

F = accumulated amount or future worth

Types of Simple Interest

1.

Ordinary Simple Interest – simple interest in which it is

assumed that each month contains 30 days and

consequently each year has 360 days.

1 month = 30 days

1 year = 360 days (banker’s year)

2.

Exact Simple Interest – simple interest in which the

exact number of days per month is used.

1 ordinary year = 365 days

1 leap year = 366 days

Sample Problems on

Simple Interest

1.

2.

3.

4.

5.

A loan of Php50,000 is made for a period of 13 months, from

April 1 to April 30 of the following year, at a simple interest rate

of 20%. What future amount is due at the end of the loan

period?

What is the principal amount if the amount of interest at the

end of 2 ½ years is Php450 for a simple interest rate of 6% per

annum?

Determine the exact simple interest of Php25,000 for the

period of December 27, 2002 to March 23, 2003, if the rate of

interest is 10%.

What is the interest due on a Php1,500 loan for 4 years and

three months if it bears 12% ordinary simple interest?

Determine the exact simple interest of Php4,000 for the period

of Feb. 14, 1984 to November 30, 1984, if the rate of interest

is 18%.

Compound Interest

Compound Interest – the

interest for an interest

period is calculate on the

principal plus total amount

of interest accumulated in

the

previous

period.

Compound interest means

“the interest on top of

interest.”

𝐅 = 𝐏(𝟏

+ 𝐢)𝐧

𝐏 = 𝐅(𝟏 + 𝐢)−𝐧

𝐫

𝐢=

𝐦

𝐧=𝐦×𝐭

Where:

I = interest

i = rate of interest

n = number of interest periods

m = number of compounding periods

t = time

P = present worth

F = future worth

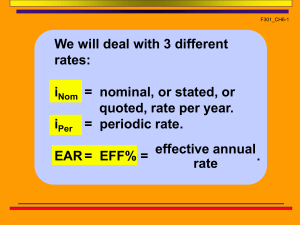

Rates of Interest

Rate of Interest – it is the cost of borrowing money.

Nominal Rate of Interest – it specifies the rate of interest and a

number of interest periods in one year.

Where:

i = interest rate per interest period

r = nominal interest rate

m = number of compounding periods

𝐫

𝐢=

𝐦

Effective Rate of Interest – it is the actual or exact rate of

interest on the principal during one year.

𝐄𝐑 = (𝟏 + 𝐢)𝐦 −𝟏

𝐫

𝐄𝐑 = 𝟏 +

𝐦

𝐦

−𝟏

Where:

ER = effective rate

i = interest rate per interest period

r = nominal interest rate

m = number of compounding periods

Values of “m”

m = 1 for compounded annually (every 12 months)

m = 2 for compounded semi-annually (every 6 months)

m = 4 for compounded quarterly (every 3 months)

m = 6 for compounded bi-monthly (every 2 months)

m = 8 for compounded semi-quarterly (every 1 1/2 months)

m = 12 for compounded monthly (every month)

m = 24 for compounded semi-monthly (every 1/2 month)

F/P and P/F Factors:

Notation and Equations

Find/Given

Standard

Notation

Equation

Equation

with Factor

Formula

Excel

Functions

(F/P,i,n)

Singlepayment

compound

amount

F/P

F = P(F/P,i,n)

F = P(1 + i)n

FV(i%,n,,P)

(P/F,i,n)

Singlepayment

present

worth

P/F

P = F(P/F,i,n)

P = F(1 + i)-n

PV(i%,n,,F)

Factor

Notation

Factor

Name

Sample Problems on

Compound Interest

1.

2.

3.

4.

5.

What rate of interest compounded annually must be received if

an investment of Php5,400 made now will result in a receipt of

Php7,200 5 years hence?

What amount will be accumulated by Php4,100 in 10 years at 6%

compounded annually?

What effective annual interest rate corresponds to the following

situations?

a.nominal interest rate of 10% compounded semi-annually

b.nominal interest rate of 6% compounded monthly

c.nominal interest rate of 8% compounded quarterly

How much should Engr. Cruz deposit now, if after 10 years, this

will amount to Php100,000. Interest rate is 12% compounded

semiannually?

If Php1,000 becomes Php5,734 after 15 years, when invested at

an unknown rate of interest compounded semi-annually,

determine the unknown nominal rate and corresponding effective

rate.

Cash Flow Diagram

Cash Flow Diagram – depicts the timing and

amount of expenses (negative, downward) and

revenues (positive, upward) for engineering

projects.

Receipt (positive cash

flow or cash inflow

Disbursement (negative

cash flow or cash outflow

Types of Cash Flow Diagrams

P-Pattern

F-Pattern

A-Pattern

G-Pattern

“present”

1

2

3

n

“future”

1

2

3

n

“annual”

1

2

3

n

“gradient”

1

2

3

n

Equation of Value

An equation of value is obtained by setting

the sum of the values on a certain

comparison or local date (or focal date) of

one set of obligations equal to the sum of

the values on the same date of another set

of obligations.

Sample Problems on

Equation of Value

1.

2.

Jay wishes his son, Jason, to receive

Php1,000,000 twenty years from now. What

amount should he invest now, if it will earn interest

of 12% compounded annually during the first five

years and 10% compounded monthly for the

remaining years.

Find the present worth of a future payment of

Php300,000 to be made in 10 years with an

interest rate of 10% compounded annually. What

will be the amount if it will be paid 5 years later (on

the 15th year)?

Discrete Payments

The solution of discrete payments or number of

transactions occurring at different periods is taking each

transaction to the base year and equating each value.

Steps in Solving Discrete Payments:

1. Draw the cash flow diagram.

2. Select any convenient focal date.

3. Years on the left of the focal date have a positive sign

while years on the right of the focal date have a

negative sign.

4. Use the principle: Cash Inflow = Cash Outflow

Sample Problems on

Discrete Payments

1.

2.

3.

Acosta Holdings borrowed Php9,000 from Smith Corporation on

January 1, 1998 and Php12,000 on January 1, 2000. Acosta

Holdings made a partial payment of Php7,000 on January 1,

2001. It was agreed that the balance of the loan would be

amortized by two payments, one on January 1, 2002 and one

on January 1, 2003, the second being 50% larger than the first.

If the interest rate is 12%, what is the amount of each payment?

A contract has been signed to lease a restaurant at Php20,000

per year with annual increase of Php1,500 for 8 years.

Payments are to be made at the end of each year, starting one

year from now. The prevailing rate is 7%. What lump sum paid

today would be equivalent to the 8 year lease program?

Mr. Cruz buys a second hand car worth Php150,000 if paid in

cash. On installment basis, he pays Php50,000 downpayment,

Php30,000 at the end of one year, Php40,000 at the end of two

years and a final payment at the end of four years. Find the final

payment if interest is 14%.

Continuous

Compounding Interest

The solution for interest compounded continuously

can be derived thru differential equations and can be

found as:

𝐝𝐏

= 𝐢𝐏

𝐝𝐭

Where:

i = interest rate compounded continuously

P = present worth

t = time

Sample Problems on

Continuous Compounding Interest

1.

2.

Philip invested $100 on a bank. The bank offers

5% interest compounded continuously in a

savings account. Determine (a) how long will it

require for him to earn $5 (b) the equivalent

simple interest rate for 1 year of the bank.

Which is more advisable to invest Php5,000 for

five (5) years, to bank A that offers 5%

compounded continuously or to bank B that

offers 10% simple interest?

Banker’s Discount

Certain banks lend money in such a way that they

deduct the interest on the money. They actually don’t

lend you money you asked for. This type of computing

money is called banker’s discount. The money received

by the borrower after the discount has been deducted is

called proceeds.

𝟏 − (𝟏 + 𝐧𝐢)−𝐧

𝐝=

𝐧

Where:

i = rate of interest

d = rate of discount

n = number of interest period

Sample Problems on

Banker’s Discount

1.

Ms. Glydel Marquez borrowed money from a bank.

She received from the bank Php1,342 and

promised to repay Php1,500 at the end of 9

months. Determine the following: (a) simple

interest rate (b) discount rate or often referred as

Banker’s discount.

0

0