government in a market economy

advertisement

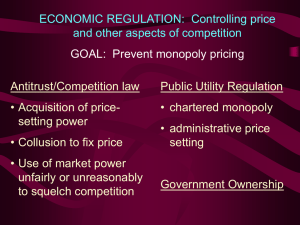

GOVERNMENT’S ROLE IN A 21ST CENTURY MARKET ECONOMY John Kwoka Finnegan Distinguished Professor of Economics Northeastern University November 30, 2011 OVERVIEW U.S. is fundamentally a market economy 1-2% of GDP from government enterprises post office municipal services 3-4% substantially regulated industries 95% private, but still subject to antitrust laws environmental and safety regulation Much less government ownership, regulation than other economies Much less than in the past in the U.S. TYPES OF INVOLVEMENT Three broad types of government involvement in industries Conventional industry regulation Competition/antitrust policy Industries in crises (1) INDUSTRY REGULATION Conventional industry regulation where “free market” would mean monopoly power Classic scenario involves “natural monopoly” (1) INDUSTRY REGULATION Conventional industry regulation where “free market” would mean monopoly power Classic scenario involves “natural monopoly” REGULATORY POLICY Regulated natural monopoly industries: local telecom (but not long distance) electricity distribution (but not generation) pipelines Nature and degree of regulation change over time Regulation now more flexible (“light handed”) Degree of regulation varies with needs of time size of natural monopoly sectors emergence of competition (2) ANTITRUST POLICY Antitrust enforces rules of competitive game It is reactive to specific types of problems Examples Conspiracies to raise price Cartel of flat panel display manufacturers Use of monopoly power to deter entry “Reverse payments” by drug companies Control over mergers for market power AT&T - T-Mobile (3) CRISIS POLICY Other need for government involvement derives from companies and sectors in crisis Excesses and imbalances Transformations and dislocations Examples of such industries S&Ls in 1980s Airlines after 9/11 Auto industry after 2008 Banking and financial institutions REGULATORY CYCLE S IN HISTORY Regulation has significantly increased at certain times Then tends to recede until new cycle starts Late 1800s saw rise of railroads and national markets Prompted concern over monopoly abuses by large railroads Let to increased oversight and involvement Interstate Commerce Commission Also, Sherman Antitrust Act Over time, as problems eased and more competition emerged, some retreat of regulation THE CYCLE REPEATS Retreat tends to unleash forces that cause next round of excesses, imbalances Thus cycle repeats itself Thus, stock market crash, Great Depression on 1920s-1930s Those crises predictably led to greater involvement by government Utility abuses led to Federal Power Commission Telecom monopolies prompted Federal Communications Commission Securities abuses led to Securities and Exchange Commission High water mark of regulatory involvement during 1960s-70s 10-12% U.S. economy either public or heavily regulated PUSHBACK AGAINST REGULATION Extensive regulation prompted free market critique in 1960s-70s Spearheaded by laissez-faire economics of Chicago School Argument was that market can discipline itself Led to successive rounds of deregulation First round began in 1970s-80s with “easy” cases Airlines, trucking, natural gas In 1980s-90s moved on to more challenging cases Telecom, railroads, depository institutions Considerable benefits from much of this deregulation Generally lower costs and prices, greater choice Some problems (e.g., railroads, S&Ls) THE LATEST CYCLE Deregulation movement of 1990s-2000s focused on new industries Electricity Banking and financial institutions These were hardest cases due to tricky underlying circumstances Electricity required on-going coordination and interconnection Banking and finance required good information, correct incentives, good governance Early warning signs of trouble Electricity crisis in California Accounting abuses at Enron, WorldCom, Tyco Collapse of Long-Term Capital Management Then collapse of major financial institutions in 2008 GOVERNMENT IN CRISIS ECONOMY Financial crisis of 2008, followed by Great Recession swept up several sectors: Banking and financial institutions, of course Also autos, housing, and others Result was again massive government intervention Provides opportunity to reflect on government’s role Also to see how this fits into regulatory/deregulatory cycle TALE OF TWO BAILOUTS Consider U.S. auto industry Problems pre-date financial crisis Root cause was lack of competition among domestic “Big 3" Results were progressive losses of jobs, retirement protections Also market shares, profits, shareholder value And then the credit crisis and recession of 2008 hit Sales dropped by 50-55% Clearly unsustainable AUTO INDUSTRY BAILOUT Auto industry prompted vigorous political argument Free market advocates contended companies should be allowed to fail Pragmatists contended that economic and social consequences huge Bush Administration authorized interim loans in 2008 Obama Administration announced its plan in March 2009 Involved several assistance programs Supplier Support Program Warranty Commitment Program Director of Auto Recovery Total cost about $35 B STRINGS ATTACHED Government forced both GM and Chrysler into bankruptcy Took equity position in both companies, providing capital But companies were forced to make fundamental changes Plants had to be closed, products eliminated Chrysler told it had to find partner–and it found Fiat GM told it would have to cut divisions–and it did UAW told it would lose jobs, take pay cuts–and they did Dealers told that many would close–and many were Bondholders and stockholders lost money Executives responsible for condition of companies removed CEOs of GM, Chrysler fired Long-time passive board members replaced AUTOS: THE “HARD” BAILOUT GM and Chrysler have now recovered in marketplace And at same time, government funds largely repaid By any reasonable definition, auto bailout successful Important lessons of this bailout: (1) Take firm control of companies (2) Hold people responsible (3) Transform companies (4) Get out ASAP Save the institutions (if worth saving), but ensure that the responsible individuals do not benefit or get to repeat BANKS: THE “SOFT”BAILOUT Crisis of 2008 prompted need for massive government intervention and bailout of banks, financial institutions Sector had been turned loose by deregulation Result was to unleash incentives without oversight or penalty Included largest mortgage company in country Also, largest insurer in country And some of largest banks in country WHAT DID AND DID NOT HAPPEN Might expect government to step in and rescue companies Then control bad behavior via regulation, restructuring, removal Government did step in with massive amounts of taxpayer money But there was no substantial regulation, restructuring, removal No substantial re-regulation Dodd-Frank being compromised No restoration of Glass-Steagall Volcker rule inadequate No systematic holding of companies accountable Overturning of SEC deal with Citigroup is notable exception No breakup of major banks Now larger than before No systematic removal of bad actors Executives never changed RESULT OF BAILOUT Banks now even larger, more concentrated Top 10 banks now have 58% total banking assets Up from 44% in 2000, 24% in 1995 Top 6 banks have assets totaling 63% of GDP Up from just 17% in 1995 No economic evidence largest banks need to be so big But clear evidence of their potential dangers: “systemic risk” Individuals not held fully accountable Head of Countrywide cashed out 100s of millions in stock Paid $67M to settle SEC charges without admitting guilt Head of AIG who earned $150M over six years Settled SEC charges for $15M without admitting guilt Head of Goldman Sachs earned $54M in 2007 Still there BANKS VS. AUTOS Incentives for bad bank behavior have not been controlled Structure, incentives, even some personnel remain in place Predictable that banks, financial institutions will do this again Early evidence from MF Global Contrast autos, where companies, products, executives changed Scarcely recognizable compared to pre-bailout This is the fundamental flaw of a Soft Bailout Institutions have been saved, but behavior unchanged Regulatory cycle where tough regulation follows excessive deregulation has not happened PROPER ROLE OF GOVERNMENT IN 21ST CENTURY PROPER ROLE OF GOVERNMENT IN 21ST CENTURY Man Controlling Trade