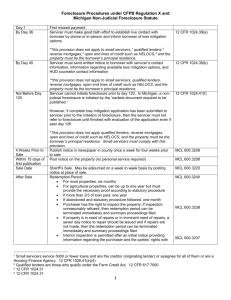

HOMEOWNER BILL OF RIGHTS

Ready for the January 1 Hangover?

Jonathan D. Jaffe

Laurence E. Platt

K&L Gates LLP

Copyright © 2012 by K&L Gates LLP. All rights reserved.

Prelude to Homeowner Bill of Rights

On February 9, 2012, five of the largest banks entered into a

$26 Billion National Mortgage Servicing Settlement Agreement

(“NMS”) with 49 state attorneys general (including California)

and a number of federal regulatory agencies

Less than 2 weeks later, Attorney General Kamala Harris and

some senior legislators announced the “California Homeowner

Bill of Rights,” designed to make permanent in California

many of the aspects of the NMS

The bills were moved from the regular legislative process to a

conference committee, resulting in a very expedited process

with limited input from the industry

2

Five Bills

The Foreclosure Reduction Act Of 2012 - AB

278 / SB 900

Blight Prevention - AB 2314

Tenant Protection - AB 2610

Enhancement Of Attorney General Enforcement

Act - AB 1950

Attorney General Special Grand Jury Act - SB

1474

3

The Foreclosure Reduction Act (“FRA”) –

General

SB 1137 - Amends and supplements 2008 emergency

legislation that implemented three categories of borrower and

tenant protections

Imposed mandatory notification, meeting and consultation

process that foreclosing lenders/servicers were required to

make available to borrowers prior to filing a notice of default

(“NOD”)

Also required REO owners to give tenants of foreclosed

residential property a minimum of 60 days’ written notice to

quit, before evicting them

Authorized local governments to impose civil fines of up to

$1,000 per day for failure of a lender or other purchaser in

foreclosure to maintain vacant residential property in good

condition and repair

4

The Foreclosure Reduction Act (“FRA”) –

General (cont’d)

Who’s Covered - Places burden of compliance on the

“mortgage servicer” - the person who directly services the loan

or is responsible for interacting with the borrower, managing

any escrow account, or enforcing the loan, either as the

current owner of the note or as the owner’s agent

Covers master servicers, owners/servicers, subservicers

Terminology in bills not always consistent - sometimes

“mortgage servicer,” sometimes “mortgagee, trustee,

beneficiary, or authorized agent,” and sometimes

combinations

Doesn’t cover trustees, or authorized agent of a trustee,

acting under “deed of trust” (“DOT”)

5

The Foreclosure Reduction Act (“FRA”) –

General (cont’d)

Large and Small Servicers - The FRA distinguishes between

(a) regulated/licensed lenders/servicers that conduct 175 or

fewer California residential mortgage foreclosures during

immediately preceding annual reporting period as established

by its primary regulator (“Smaller Servicers”), and (b) other

lenders/servicers (“Larger Servicers”)

Procedures applicable to Larger Servicers are much

more detailed

SB 900 limits application of following to Larger Servicers:

contacting the borrower prior to default, dual tracking,

single point of contact, and some private right of action

provisions

6

The Foreclosure Reduction Act (“FRA”) –

General (cont’d)

Loans Covered - First lien, consumer purpose residential

mortgage loans secured by a one-to-four family residence,

owner occupied, with borrow who is natural person and the

trustor (subject to very limited exceptions)

Unlike SB 1137, not limited to loans made between 20032007

7

The Foreclosure Reduction Act (“FRA”) –

General (cont’d)

Initiating Foreclosure – Only holder of a beneficial interest

under the DOT, the holder's designated agent, or the trustee

under the DOT may initiate nonjudicial foreclosure

No agent of the holder of the beneficial interest or trustee

may record an NOD or otherwise commence foreclosure

proceedings unless they are acting within the scope of

authority designated by the holder of the beneficial

interest

This requirement applies to all loans, not just residential

mortgage loans

8

The Foreclosure Reduction Act (“FRA”) –

General (cont’d)

Sunset – In numerous places HOBR contains

alternative sections

One version in effect from 1/1/2013 through

1/1/2018, and another on and after 1/1/2018

Where to Find – HOBR is found in 16 sections of

the Civil Code, with the same subject sometimes

addressed in multiple sections

9

The Foreclosure Reduction Act – Notices

Mortgage servicer, mortgagee, trustee, beneficiary

or authorized agent may not record an NOD until 30

days after:

Initial contact, following existing SB 1137 protocols e.g., assessing borrower’s financial situation and

exploring options for foreclosure avoidance, or

Servicer satisfies due diligence requirements to

attempt to locate borrower with no borrower

response, again following SB 1137 protocols

A new declaration of compliance must be attached to the

NOD

10

The Foreclosure Reduction Act – Notices

(cont’d)

Upon borrower request for foreclosure prevention alternative,

servicer must establish a single point of contact (“SPOC”) and

provide borrower with one or more direct means of

communication with the SPOC

Larger Servicers must also inform the borrower in a pre-NOD

outreach package:

Of any applicable protections provided under the SCRA

That borrower may request copies of the note, deed of

trust, assignments of the deed of trust, and a payment

history as of the date the borrower was last less than 60

days delinquent

11

The Foreclosure Reduction Act –

Loan Mods and Dual Tracking

Larger Servicers subject to loan mod provisions in Sections

2923.55, 2923.6, 2923.7, 2924.9, 2924.10 and 2924.11

There’s some overlap and internal inconsistencies

Restricts dual tracking (i.e., servicer forecloses while

application for a loan modification is pending)

In some places HOBR refers to “first lien loan

modifications,” while in others to “foreclosure prevention

alternatives” (defined in Section 2920.5(b) as a “first lien

loan modification or another available loss mitigation

option”)

Unclear whether the Legislature intended different

meanings

12

The Foreclosure Reduction Act –

Loan Mods and Dual Tracking (cont’d)

HOBR says no particular result required under loss mit

process

Keeps SB 1137 requirements, but requires more of servicer in

handling borrower loan mod requests, including appeal

process if denial

Unless borrower previously exhausted the loan mod process,

servicer that offers one or more foreclosure prevention

alternatives must, within 5 business days after recording an

NOD, send borrower written communication informing that

borrower may be evaluated for a foreclosure prevention

alternative and describing the application process

Upon borrower request for a foreclosure prevention

alternative, mortgage servicer must promptly establish an

SPOC

13

The Foreclosure Reduction Act –

Loan Mods and Dual Tracking (cont’d)

When borrower submits a “complete” first lien modification

application - or any document in connection with a first lien

modification application - mortgage servicer must: provide

written acknowledgment of receipt within 5 business days,

describe loan mod process, state any deadlines, and identify

any deficiencies in the documents submitted by the borrower.

Question whether this acknowledgement applies after receipt

of any document received after receipt of initial application.

14

The Foreclosure Reduction Act –

Loan Mods and Dual Tracking (cont’d)

Servicer may not record an NOD or Notice of Sale (“NOS”) or

conduct a trustee’s sale while the application is pending, or

until any of the following occurs: (1) servicer makes a written

determination that the borrower is not eligible for the mod, and

the applicable appeal period has expired; (2) the borrower

does not accept an offered mod within 14 days of the offer; or

(3) the borrower accepts an offered mod but breaches his

obligations under the mod

Application deemed “complete” when a borrower has supplied

servicer with all required documents within reasonable

timeframes specified by the servicer

15

The Foreclosure Reduction Act –

Loan Mods and Dual Tracking (cont’d)

Servicer must send borrower written notice of denial of loan

mod, including information on: (1) the reasons for denial; (2)

borrower’s appeal rights; and (3) if applicable, a description of

other foreclosure prevention alternatives “for which the

borrower may be eligible,” and steps borrower must take to be

considered for those options

Convoluted, unclear language that is likely to result in

questions as to how many times a servicer must

consider an application for a foreclosure prevention

alternative

16

The Foreclosure Reduction Act –

Loan Mods and Dual Tracking (cont’d)

If the borrower’s application is approved, the lender may not

record an NOD or NOS while the borrower is in compliance

with its terms

Servicer must record a rescission of an NOD or cancel a

pending trustee’s sale upon the borrower executing a

permanent foreclosure prevention alternative

If short sale, rescission/cancellation must occur when

sale has been approved by all parties and lender has

received proof of funds or financing

17

The Foreclosure Reduction Act –

Loan Mods and Dual Tracking (cont’d)

Servicer may not charge any application, processing, or

other fee for a first lien loan modification or other

foreclosure prevention alternative

While a foreclosure prevention alternative is being

considered, or denial is being appealed, servicer may not

collect late fees

Within 5 business days following a postponement of a

foreclosure sale for 10 or more business days, the

mortgagee must provide written notice to the borrower

regarding the new sale date and time

18

The Foreclosure Reduction Act –

Single Point of Contact

Mandates that Larger Servicers provide an SPOC for the

borrower if the borrower applies for a foreclosure prevention

alternative, and must provide borrower with one or more direct

means of communication with their SPOC

Likely that servicers will build this in at time of initial

contact and throughout default process

SPOC is satisfied by an individual or team of individuals,

provided each team member has knowledge of the

borrower’s status and remains with the borrower

throughout the pre-foreclosure process

19

The Foreclosure Reduction Act –

Robosigning

All documents filed in support of a foreclosure must

be verified for accuracy, complete, and supported by

competent and reliable evidence

Includes NODs, supporting declarations

(including declarations recorded pursuant to

Civil Code §§ 2923.5 or 2923.55), NOSs,

assignments of DOTs, and Substitutions of

Trustee recorded in connection with a

nonjudicial foreclosure, as well as declarations

filed in court with respect to any foreclosure

proceeding

20

The Foreclosure Reduction Act –

Robosigning (cont’d)

Mortgage servicers that engage in multiple and

repeated unverified signings of foreclosure

documents - “robosigning” – are subject to a $7,500

civil money penalty per DOT

May be levied by a government entity, including

the primary California regulator or licensing

agency

No private right of action

21

The Foreclosure Reduction Act –

Private Right of Action

Provides a private right of action (“PRA”) for “material”

violations, e.g., failing to provide a SPOC, processing a

dual-track foreclosure, etc.

PRA available against Smaller Servicers for material

violations of Sections 2923.5, 2924.17 or 2924.18, and

against Larger Servicers for material violations of

Sections 2923.55, 2923.6, 2923.7, 2924.9, 2924.10,

2924.11, or 2924.17

22

The Foreclosure Reduction Act –

Private Right of Action (cont’d)

If the property has not been sold, the borrower may sue

to enjoin the sale and seek attorney fees for material

violations

Servicer may seek to dissolve the injunction if it

corrects and remedies material violation

Servicer, mortgagee, trustee, beneficiary, or authorized

agent can avoid liability for any violation corrected and

remedied prior to recordation of a trustee's deed upon

sale

23

The Foreclosure Reduction Act –

Private Right of Action (cont’d)

If the property has been sold, the borrower may sue in civil

court for actual economic damages resulting from material

violation, plus attorney fees

If the violation was willful, intentional or reckless, the court

may award the borrower the higher of $50,000 or treble actual

damages

This is in addition to any other rights, remedies, or procedures

available under any other law

A violation is deemed a violation of the servicer’s charter or

license, so subject to agency administrative enforcement

In theory, could include loss of license

24

National Mortgage Settlement

National Servicing Standards

Foreclosure Information and Documentation

Third-Party Provider Oversight

Dual Track Foreclosures

Single Point of Contact

Online Loan Portal

Loan Mod Timelines

Independent Evaluation of Mod Denials

Transfer of Servicing

Protections for Military Personnel

Servicing Fees

25

National Mortgage Settlement (cont’d)

Loan Modification Requirements, Foreclosure

Information and Documentation

Consumer Relief Requirements

Principal Reduction

First-Lien Mods

Second-Lien Portfolio Mods

Actions by Subservicers

26

National Mortgage Settlement (cont’d)

Refinance and Other Loss Mitigation Requirements

Short Sales

Deficiency Waivers

Forbearance for Unemployed Borrowers

27

National Mortgage Settlement (cont’d)

Enforcement

Settlement Monitor

Internal Review Group

Quarterly Reports

Potential Violations and Right to Cure

Releases from Liability

Implementation by Servicers

28

Tenant Protection – AB 2610

Expands state law to protect tenants in a foreclosed

property from eviction for 90 days following a sale of

the home

Also requires purchasers of a rental property in a

foreclosure sale to honor tenant’s existing fixed

lease, unless the new owner plans to make the

property her principal residence or the tenant is the

original mortgagor

29

Blight Prevention - AB 2314

Removes the sunset provision from laws allowing

local governments to fine owners of blighted

property by up to $1,000 per day

The law also extends the grace period for owners to

correct the problem to 60 days for those who

purchased a foreclosed home after 2008

Also gives receivers the ability to seek a court order

ordering the blighted property’s owner to pay these

unrecovered costs

30

Enhancement Of Attorney General

Enforcement Act - AB 1950

Permanently prohibits businesses from charging an

up-front fee for mortgage renegotiation services

Also expands the state statute of limitations to three

years for the prosecution of these provisions

31

Attorney General Special Grand Jury Act –

SB 1474

Authorizes California AG to convene a special grand

jury to investigate and indict perpetrators of financial

crimes involving victims in multiple jurisdictions

32

Introducing our Blog

For news and developments related to

consumer financial products and services,

please visit our blog at

www.consumerfinancialserviceswatch.com

and subscribe to receive updates.

33

Thank you

Jonathan D. Jaffe

415 249-1023

jonathan.jaffe@klgates.com

Laurence Platt

202 778-9034

larry.platt@klgates.com

www.klgates.com

34