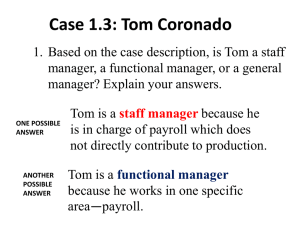

System Map

advertisement

FINANCIAL MANAGEMENT SYSTEM Risk Disclosures Stock Management decisions and policy choices Claims/Warranty Sales Payroll Purchases Balance sheet Profit and loss Assets Cash Borrowings Taxation Sales • Controls over – Orders in: separated from stores staff and debt collection staff or else documented in a log, sequence checks, agreed to stock movement records and debtor info ) – Sales prices: quoted from authorised list, any variance in accordance with authorised limits, weighted average price reviewed at regular intervals – – Delivery: sequential delivery notes raised with receiving signatures required and agreed to stock movement records Invoicing: sequence checks, restricted use of Cash Sales accounts, raised promptly from delivery notes, un-invoiced delivery notes reviewed – – – – Credit notes: within authorisation limits, only raised in relation to specific invoice number Debtors ledger: segregated from sales staff, no general journals to control account, reconciled to GL Credit control: authorised credit limits, regular review of balances to ensure within limits Debt collection: regular reporting of age of balances, prompt follow up Stock • Controls over – – – – – – – – Perpetual stock ledger: on-going reconciliation of balance on hand, movements matched to purchases and sales Standard costing: updated costing to ensure value of stock, and therefore cost of goods sold, correct, variances reviewed regularly Pick lists: record of what is to be dispatched, when and to whom, created from order logs Goods Received Notes: record of purchases in to be matched to supplier invoices, un-matched notes investigated Stock levels: authorised levels of stock to be held and to prompt re-ordering Stock counts: regular counts to confirm amounts held and value which will affect profit Stock variances: need explanation and analysis Stock obsolescence: must be identified to recognise true cost of sales Purchases • Controls over – – – – – Purchase orders: only raised by authorised staff, sequence checks, matched to supplier invoices Pricing: invoices checked and approved for contract rates, significant variances investigated Classification: classified as stock, consumables by knowledgeable staff Creditor ledger: : segregated from purchasing staff, no general journals to control account, reconciled to GL Reconciliations: creditor balances to monthly statements Cash • Controls over – – – – – – – – – Cash flow: develop projections as a control to match actual to expected and to prepare for any tightening No. of accounts: minimise to reduce volume over which controls required Signatories: multiple signatories to reduce risk of fraud Authorisation process: all payment requisitions supported by invoices or suitable documentation Cancellation of documents: documents initialled once payment authorised to ensure not paid twice Opening of mail: segregated from staff responsible for bank, debtor and creditor reconciliation Receipt allocation: at time of banking unless unidentifiable Banking: segregated from staff responsible for bank, debtor and creditor reconciliation Reconciliation process: segregated from staff opening mail and banking, or detail reviewed and approved Assets: Property, Plant & Equipment • Controls over – – – – – – – Asset register: lists all assets for control, security and insurance Purchase authorisation: authorised limits Asset identification: for control and security Depreciation: consider residual value and period of useful life to correctly estimate annual cost Impairment: review assets annually for changes to depreciation assumptions as this will affect P&L Insurance: ensure assets insured to minimise risk of loss Security: review security of assets to minimise risk of loss Payroll • Controls over – Hiring: by authorised staff only and after clear due diligence process – – – – – – – – – – Employee files: include all records for compliance with employment legislation Timesheets: authorised to ensure payment for work performed Pay rates: authorised and reviewed regularly Deduction authorities: authorised and retained to minimise risk of disputes Salary/wage payments: segregated from staff preparing pay Payroll authorisation: evidence of review for reasonableness, segregated from staff preparing pay Payroll reconciliations: control over expense, payments and other payroll obligations Superannuation: reconciled and controlled to reduce risk of non-compliance Workcover: reconciled and controlled to reduce risk of non-compliance Leave records: reconciled to ensure correct record of entitlement and reduce risk of dispute Taxation • Controls over – – – – Goods and Services Tax: accounts correctly set up to account for GST, BAS reconciled to GST accounts Fringe Benefit Tax: ensure adequate information collected to allow compliance Payroll Tax: payments reconciled to payroll monthly, expense reconciled to payments Income Tax: : ensure adequate information collected to allow compliance, reconcile amount owing to GL Borrowings • Controls over – – – – – – Applications: retain for control over maturity dates and costs charged Borrowing covenants: measure limits against actual results regularly Interest cost: measure accurately to control and review cost of funding Repayment schedules: calculate to ensure correct liability reflected in balance sheet Security: document security given to ensure no legal issues from future sale of assets etc Guarantees: document to ensure acknowledged

![[Product Name]](http://s2.studylib.net/store/data/005238235_1-ad193c18a3c3c1520cb3a408c054adb7-300x300.png)