Presentation - United Leasing, Inc.

advertisement

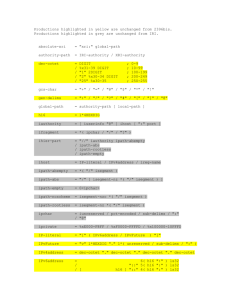

Romain Buick, Inc. 401(k) Plan Zach Hopkins Sr. Client Consultant (812) 456-3531 Zach.Hopkins@53.com TODAY’S AGENDA… Plan Highlights Asset Allocation and your Investment options Accessing your account Plan Highlights Eligibility Age 21 and 1,000 hours of service in 12 mos. Entry dates Calendar quarters (Jan.1, Apr.1, Jul.1, Oct.1) EE Contributions Employee pre-tax deferrals up to $17,500 (2013) Employees age 50+ (additional $5,500) Stop contributions anytime, increase or decrease deferrals quarterly ER Contributions Discretionary matching contribution on elective deferrals (50% match on first 4% deferred) Discretionary profit-sharing contributions (1,000 hours of service) Plan Highlights (cont.) Vesting On employer contributions 2 yrs. = 20% 3 yrs. = 50% 4 yrs. or more = 100% Investments Participants direct investment for all contributions. (default investment FMT/Touchstone Conservative Alloc. 35% stock, 65% bonds/cash) Withdrawals Normal retirement age (65), In-service at age 59 and ½, death, disability or termination of employment, hardships available ARE YOU LOOKING … for a tax break? Lower your taxable income by making pretax contributions Delay taxes on your contributions and earnings until you make a withdrawal Annual Salary Retirement Savings Taxable Income Taxes (25%) Take-home Pay Contributing 5% to the 401(k) Plan Contributing 0% to the 401(k) Plan $30,000 $30,000 $1,500 $0 $28,500 $30,000 $7,125 $7,500 $21,375 $22,500 ARE YOU LOOKING … for a tax break? 401(k) Plan Snapshot Retirement Savings $1,500 Tax Savings $7,500 - $7,125 = $375 Reduction in Take-home Pay $22,500 - $21,375 = $1,125 These examples assume the employee earns $30,000 per year and contributes 5% to the plan on a pretax basis. The calculations are for illustration only. ARE YOU … taking advantage of your employer match? Your Annual Contribution Company’s Annual Contribution Maximum Amount of Company’s Annual Contribution $30,000 x 4% = $1,200 $.50 x $1,200 = $600 $30,000 x 2% = $600 $0 $.50 x $900 = $450 $30,000 x 1.5% = $450 $600 – $450 = $150 $30,000 x 3% = $900 Lost Benefit This example assumes the employee earns $30,000 per year, and that the company contributes $0.50 for every $1 the employee contributes to the plan, up to a maximum of 4% of the employee’s compensation per year. CONTRIBUTING JUST 1% MORE … can have a significant impact over time. Contributes 5% for 30 Years Contributes 6% for 30 Years $183,518 $220,222 Difference of $37,000 $54,000 $45,000 Contributions Account Balance Investor B Account Balance Investor A Total Account Value Contributions Total Account Value This example assumes both investors earn $30,000 per year. Investor A contributes 5% to the plan on a pretax basis; Investor B contributes 6% to the plan on a pretax basis. Their investments earn an average of 8% per year for 30 years. The calculations do not factor in salary increases, any company match or inflation and are for illustration only. THE SOONER YOU START … the better you’ll finish. Saves for 10 Years and Stops Waits 10 Years to Start Saving $160,720 Account Balance Investor B Account Balance Investor A Less $40,000 $118,432 $37,000 $15,000 Contributions Starting at Age 30 and Ending at Age 40 Total Account Value Contributions Starting at Age 40 and Ending at Age 65 Total Account Value This example assumes both investors earn $30,000 per year and contribute 5% to the plan on a pretax basis. Investor A starts saving at age 30, stops saving at age 40, and retires at age 65. Investor B starts saving at age 40 and stops saving when he retires at age 65. Their investments earn an average of 8% per year. The calculations do not factor in salary increases or inflation and are for illustration only. INVESTMENT OPTIONS ALLOCATION … Asset allocation is the process of dividing your contributions among three basic asset classes: stocks, bonds, and cash equivalents. INVESTMENT OPTIONS You take a more active role in financial planning You select the combination of funds that best meet your risk tolerance and return objectives Asset Class Investment Options Fixed Income (Cash Equivalents) FMT/FFTW Income Plus Balanced Funds FMT/Touchstone Growth (90% stock, 10% bonds) FMT/Touchstone Moderate Gr. (75% stock, 25% bonds) FMT/Touchstone Conservative (35% stock, 65% bonds) Domestic Stocks FMT/Vanguard 500 Index FMT/Vanguard Mid Cap Index FMT/Vanguard Small Cap Index INVESTMENTS AND INFLATION 12% 10% 9.8% Percentage of Annual Returns Compared With Inflation, 1926 – 2010 8% 5.3% 6% 3.7% 4% Inflation 2% 3.0% 0% Large-cap Stocks Intermediate-term Government Bonds U.S. Treasury Bills Source: Ibbotson Associates, Stocks, Bonds, Bills and Inflation Yearbook 2011. Stocks are represented by the Standard & Poor’s 500 Stock Index, bonds by a one-bond portfolio or intermediate-term government bonds, T-Bills by a one-bond portfolio of U.S. Treasury bills. Investors cannot invest directly in these indexes. Note that common stocks and bonds fluctuate in value. The interest and principal on U.S. Treasury bills and many government bonds are guaranteed. Inflation is represented by the Consumer Price Index. Inflation data do not represent investment return. Past performance is not indicative of future results of the performance of any fund in your plan. BEST AND WORST ONE-YEAR RETURNS 1990 – 2010 Average return Largest one-year return Worst one-year return Source: Ibbotson Associates, Stocks, Bonds, Bills and Inflation Yearbook 2011. Stocks are represented by the Standard & Poor’s 500 Stock Index, bonds by a one-bond portfolio or intermediate-term government bonds, T-Bills by a one-bond portfolio of U.S. Treasury bills. Investors cannot invest directly in these indexes. Note that common stocks and bonds fluctuate in value. The interest and principal on U.S. Treasury bills and many government bonds are guaranteed. Past performance is not indicative of future results of the performance of any fund in your plan. KEEP IN TOUCH planretire.53.com Secure, password-protected, encrypted site Review account information, transaction history, and statements Transfer account balance among investment options and/or change your deferral amount Access educational information and planning tools Toll-free Participant Services Line 1.800.754.9080 Client Service Representatives available Monday to Friday 8:30 AM to 7:00 PM (ET) How do I enroll? •Complete the New Account Form •Complete the Designation of Beneficiary Form Q&A Questions?