Natural Gas Market Recent History

New York’s

Energy Opportunities 2010

Gordon Boyd, EnergyNext, Inc.

For

Congressman Scott Murphy’s

Economic Action Summit

March 15, 2010

Good News and Bad News

1.

Historic low energy prices…today.

2.

Capital Region still pays more than it should

3.

Cap and Trade upside for NY.

4.

Energy renewables agenda.

5.

Energy infrastructure agenda.

6.

Consumers have the responsibility to choose.

Energy Opportunities 2010

Why are prices low?

Demand destruction: The Great

Recession ( Bad news )

Speculators out of market ( Good news )

Natural gas supplies are up.

Unconventional, shale gas. ( Good news )

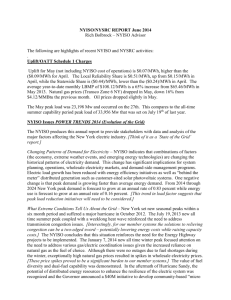

Energy Opportunities 2010

Wholesale Power Prices at Historic

Low in 2009 (NYISO)

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Load

GWh

428

430

435

433

438

458

444

458

452

435

Av.Electric

$/MWh

$58.26

$51.22

$49.90

$62.58

$62.80

$93.83

$76.45

$80.29

$95.31

$48.63

Av.NatGas

$/MMBtu

$5.52

$4.54

$3.85

$6.48

$6.80

$10.01

$7.36

$8.50

$10.13

$4.87

Energy Opportunities 2010

Wholesale Electricity Price Trend

2000-2009 (Average, NYS)

Average Wholesale Electric prices $/MWh (NYISO 2010)

$120.00

$100.00

$80.00

$60.00

$40.00

$20.00

$-

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Energy Opportunities 2010

Price $/MWh

Wholesale Natural Gas Price Trends

2000-2009 (Average, NYS)

Average NatGas Prices $/MMBtu

$12.00

$10.00

$8.00

$6.00

NatGas$/MMBtu

$4.00

$2.00

$-

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Energy Opportunities 2010

Total Electric Demand

NYS 2000-2009

Load GWh (NYISO 2010)

450

445

440

435

430

425

420

415

410

465

460

455

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Energy Opportunities 2010

Load GWh

NYMEX Natural Gas Prices

Natural gas storage trend, last

24 months (USEIA)

Energy Opportunities 2010

January 3, 2010, 1 p.m.

Energy Opportunities 2010

January 6, 2010, 9 a.m.

Energy Opportunities 2010

Capital Region Pricing Factors

Transmission congestion

Insufficient local generation

Stable, growing demand (Global

Foundries)

Cost to region +/- $200,000,000 per year.

Energy Opportunities 2010

Grid upgrade plans

(NYISO 2010)

Firm: Spier Falls to Rotterdam

Non-firm:

Spier to Luther Forest

Rotterdam to Luther Forest

Mohican to Luther Forest

North Troy to Luther Forest

Irish Road to Luther Forest

Just announced: Champlain-Hudson Express

Energy Opportunities 2010

Cap and Trade: Good News for

New York ratepayers

Carbon tax will raise price of coalfired generation.

Other states are more dependent on coal than New York.

Electric prices will normalize.

Energy Opportunities 2010

New York vs U.S.

New York State 15.27 cents/kwh

U.S. average 8.90 cents/kwh

Energy Opportunities 2010

Pennsylvania Electric generation fuel mix, Nov. 2009

Coal

Petroleum

Natural Gas

Nuclear

Renewables

Energy Opportunities 2010

Ohio Electric generation fuel mix Nov. 2009

Coal

Petroleum

Natural Gas

Nuclear

Renewables

Energy Opportunities 2010

NY State Electric generation by fuel source Nov. 2009

Coal

Petroleum

Natural Gas

Nuclear

Renewables

Energy Opportunities 2010

Renewables by 2015

(NYS Energy Plan)

Wind (1,280MW as of 2009):

On shore 7,993 MW

Off shore 534 MW

Solar PV: 100 MW (14.6MW as of 2006)

Total NYS peak electric demand 2008:

+/- 38,720 MW (USEIA)

Energy Opportunities 2010

New York wind resources

Energy Opportunities 2010

Private Investment in renewables

Energy price hedge

On-site, behind the meter, PPAs

Bi-lateral deals with developers

Green marketing

Renewable Energy Credits (RECs)

Energy Opportunities 2010

…What’s next?

NYS Energy Plan encourages

1.

New capacity, both Generation and

Transmission.

2.

Fuel diversity, especially renewables.

3.

Clear signals to consumers from energy markets to induce efficiency.

Energy Opportunities 2010

Other policy initiatives under way

Smart metering – Installations began 2008.

Net metering – Customer sited generation banking.

Article 10 - One-stop permitting expired

2002. Is renewed effort in store?

Federal ARRA funding, block grants

Energy Opportunities 2010

Consumer Choices and Responsibilities

Shop for energy supplies, price, rate, tax savings. Pay less.

Energy efficiency, SCR, NYSERDA programs. Use less.

Federal incentives, tax credits for efficiency and renewables

Energy Opportunities 2010