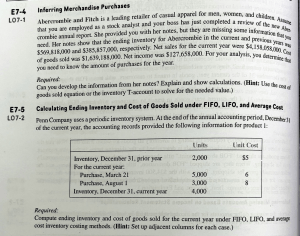

Accounting Principles 11th Edition - US GAAP Questions & Solutions Chapter 6 Inventories Jerry J. Weygandt Paul D. Kimmel Donald E. Kieso BRIEF EXERCISES BE6-1 Farley Company identifies the following items for possible inclusion in the taking of a physical inventory. Indicate whether each item should be included or excluded from the inventory taking. (a) Goods shipped on consignment by Farley to another company. (b) Goods in transit from a supplier shipped FOB destination. Identify items to be included in taking a physical inventory. (LO 1) 306 6 Inventories (c) Goods sold but being held for customer pickup. (d) Goods held on consignment from another company. Identify the components of goods available for sale. (LO 2) Compute ending inventory using FIFO and LIFO. (LO 2) BE6-2 Wilbur Company has the following items: (a) Freight-In, (b) Purchase Returns and Allowances, (c) Purchases, (d) Sales Discounts, and (e) Purchase Discounts. Identify which items are included in goods available for sale. BE6-3 In its first month of operations, Bethke Company made three purchases of merchandise in the following sequence: (1) 300 units at $6, (2) 400 units at $7, and (3) 200 units at $8. Assuming there are 360 units on hand, compute the cost of the ending inventory under the (a) FIFO method and (b) LIFO method. Bethke uses a periodic inventory system. Compute the ending inventory using average-cost. BE6-4 Data for Bethke Company are presented in BE6-3. Compute the cost of the ending inventory under the average-cost method, assuming there are 360 units on hand. (LO 2) BE6-5 The management of Svetlana Corp. is considering the effects of inventory-costing methods on its financial statements and its income tax expense. Assuming that the price the company pays for inventory is increasing, which method will: Explain the financial statement effect of inventory cost flow assumptions. (LO 3) Explain the financial statement effect of inventory cost flow assumptions. (LO 3) Determine the LCM valuation using inventory categories. (LO 4) (a) (b) (c) (d) Provide the highest net income? Provide the highest ending inventory? Result in the lowest income tax expense? Result in the most stable earnings over a number of years? BE6-6 In its first month of operation, Franklin Company purchased 120 units of inventory for $6, then 200 units for $7, and finally 140 units for $8. At the end of the month, 180 units remained. Compute the amount of phantom profit that would result if the company used FIFO rather than LIFO. Explain why this amount is referred to as phantom profit. The company uses the periodic method. BE6-7 Central Appliance Center accumulates the following cost and market data at December 31. Inventory Categories Cost Data Market Data Cameras Camcorders DVD players $12,000 9,500 14,000 $12,100 9,700 12,800 Compute the lower-of-cost-or-market valuation for the company’s total inventory. Determine correct income statement amounts. (LO 5) Compute inventory turnover and days in inventory. (LO 6) Apply cost flow methods to perpetual inventory records. BE6-8 Pettit Company reports net income of $90,000 in 2014. However, ending inventory was understated $7,000. What is the correct net income for 2014? What effect, if any, will this error have on total assets as reported in the balance sheet at December 31, 2014? BE6-9 At December 31, 2014, the following information was available for A. Kamble Company: ending inventory $40,000, beginning inventory $60,000, cost of goods sold $270,000, and sales revenue $380,000. Calculate inventory turnover and days in inventory for A. Kamble Company. *BE6-10 Gregory Department Store uses a perpetual inventory system. Data for product E2-D2 include the following purchases. (LO 7) Date Number of Units Unit Price May 7 July 28 50 30 $10 13 On June 1, Gregory sold 26 units, and on August 27, 40 more units. Prepare the perpetual inventory schedule for the above transactions using (a) FIFO, (b) LIFO, and (c) movingaverage cost. Apply the gross profit method. *BE6-11 At May 31, Suarez Company has net sales of $330,000 and cost of goods available (LO 8) Apply the retail inventory method. (LO 8) for sale of $230,000. Compute the estimated cost of the ending inventory, assuming the gross profit rate is 35%. *BE6-12 On June 30, Calico Fabrics has the following data pertaining to the retail inventory method. Goods available for sale: at cost $38,000; at retail $50,000; net sales $40,000; and ending inventory at retail $10,000. Compute the estimated cost of the ending inventory using the retail inventory method. Exercises > 307 DO IT! Review DO IT! 6-1 Gomez Company just took its physical inventory. The count of inventory items on hand at the company’s business locations resulted in a total inventory cost of $300,000. In reviewing the details of the count and related inventory transactions, you have discovered the following. Apply rules of ownership to determine inventory cost. (LO 1) 1. Gomez has sent inventory costing $26,000 on consignment to Kako Company. All of this inventory was at Kako’s showrooms on December 31. 2. The company did not include in the count inventory (cost, $20,000) that was sold on December 28, terms FOB shipping point. The goods were in transit on December 31. 3. The company did not include in the count inventory (cost, $17,000) that was purchased with terms of FOB shipping point. The goods were in transit on December 31. Compute the correct December 31 inventory. DO IT! 6-2 The accounting records of Old Towne Electronics show the following data. Beginning inventory Purchases Sales 3,000 units at $5 8,000 units at $7 9,400 units at $10 Compute cost of goods sold under different cost flow methods. (LO 2) Determine cost of goods sold during the period under a periodic inventory system using (a) the FIFO method, (b) the LIFO method, and (c) the average-cost method. (Round unit cost to nearest tenth of a cent.) DO IT! 6-3 (a) Moberg Company sells three different categories of tools (small, medium, and large). The cost and market value of its inventory of tools are as follows. Small Medium Large Cost Market Value $ 64,000 290,000 152,000 $ 73,000 260,000 171,000 Compute inventory value under LCM. (LO 4) Determine the value of the company’s inventory under the lower-of-cost-or-market approach. (b) Janus Company understated its 2013 ending inventory by $31,000. Determine the impact this error has on ending inventory, cost of goods sold, and owner’s equity in 2013 and 2014. DO IT! 6-4 Early in 2014, Chien Company switched to a just-in-time inventory system. Its sales, cost of goods sold, and inventory amounts for 2013 and 2014 are shown below. Sales Cost of goods sold Beginning inventory Ending inventory 2013 2014 $3,120,000 1,200,000 180,000 220,000 $3,713,000 1,425,000 220,000 100,000 Compute inventory turnover and assess inventory level. (LO 6) Determine the inventory turnover and days in inventory for 2013 and 2014. Discuss the changes in the amount of inventory, the inventory turnover and days in inventory, and the amount of sales across the two years. EXERCISES E6-1 Tri-State Bank and Trust is considering giving Josef Company a loan. Before doing so, management decides that further discussions with Josef’s accountant may be desirable. One area of particular concern is the inventory account, which has a year-end balance of $297,000. Discussions with the accountant reveal the following. 1. Josef sold goods costing $38,000 to Sorci Company, FOB shipping point, on December 28. The goods are not expected to arrive at Sorci until January 12. The goods were not included in the physical inventory because they were not in the warehouse. Determine the correct inventory amount. (LO 1) 308 6 Inventories 2. The physical count of the inventory did not include goods costing $95,000 that were shipped to Josef FOB destination on December 27 and were still in transit at year-end. 3. Josef received goods costing $22,000 on January 2. The goods were shipped FOB shipping point on December 26 by Solita Co. The goods were not included in the physical count. 4. Josef sold goods costing $35,000 to Natali Co., FOB destination, on December 30. The goods were received at Natali on January 8. They were not included in Josef’s physical inventory. 5. Josef received goods costing $44,000 on January 2 that were shipped FOB destination on December 29. The shipment was a rush order that was supposed to arrive December 31. This purchase was included in the ending inventory of $297,000. Instructions Determine the correct inventory amount on December 31. Determine the correct inventory amount. (LO 1) E6-2 Rachel Warren, an auditor with Laplante CPAs, is performing a review of Schuda Company’s inventory account. Schuda did not have a good year, and top management is under pressure to boost reported income. According to its records, the inventory balance at year-end was $740,000. However, the following information was not considered when determining that amount. 1. Included in the company’s count were goods with a cost of $250,000 that the company is holding on consignment. The goods belong to Harmon Corporation. 2. The physical count did not include goods purchased by Schuda with a cost of $40,000 that were shipped FOB destination on December 28 and did not arrive at Schuda warehouse until January 3. 3. Included in the inventory account was $14,000 of office supplies that were stored in the warehouse and were to be used by the company’s supervisors and managers during the coming year. 4. The company received an order on December 29 that was boxed and sitting on the loading dock awaiting pick-up on December 31. The shipper picked up the goods on January 1 and delivered them on January 6. The shipping terms were FOB shipping point. The goods had a selling price of $40,000 and a cost of $28,000. The goods were not included in the count because they were sitting on the dock. 5. On December 29, Schuda shipped goods with a selling price of $80,000 and a cost of $60,000 to Reza Sales Corporation FOB shipping point. The goods arrived on January 3. Reza Sales had only ordered goods with a selling price of $10,000 and a cost of $8,000. However, a sales manager at Schuda had authorized the shipment and said that if Reza wanted to ship the goods back next week, it could. 6. Included in the count was $40,000 of goods that were parts for a machine that the company no longer made. Given the high-tech nature of Schuda’s products, it was unlikely that these obsolete parts had any other use. However, management would prefer to keep them on the books at cost, “since that is what we paid for them, after all.” Instructions Prepare a schedule to determine the correct inventory amount. Provide explanations for each item above, saying why you did or did not make an adjustment for each item. Calculate cost of goods sold using specific identification and FIFO. (LO 2, 3) E6-3 On December 1, Marzion Electronics Ltd. has three DVD players left in stock. All are identical, all are priced to sell at $150. One of the three DVD players left in stock, with serial #1012, was purchased on June 1 at a cost of $100. Another, with serial #1045, was purchased on November 1 for $90. The last player, serial #1056, was purchased on November 30 for $80. Instructions (a) Calculate the cost of goods sold using the FIFO periodic inventory method assuming that two of the three players were sold by the end of December, Marzion Electronics’ year-end. (b) If Marzion Electronics used the specific identification method instead of the FIFO method, how might it alter its earnings by “selectively choosing” which particular players to sell to the two customers? What would Marzion’s cost of goods sold be if the company wished to minimize earnings? Maximize earnings? (c) Which of the two inventory methods do you recommend that Marzion use? Explain why. Exercises E6-4 Linda’s Boards sells a snowboard, Xpert, that is popular with snowboard enthusiasts. Information relating to Linda’s purchases of Xpert snowboards during September is shown below. During the same month, 121 Xpert snowboards were sold. Linda’s uses a periodic inventory system. Date Explanation Units Unit Cost Total Cost Sept. 1 Sept. 12 Sept. 19 Sept. 26 Inventory Purchases Purchases Purchases 26 45 20 50 $ 97 102 104 105 $ 2,522 4,590 2,080 5,250 Totals 141 309 Compute inventory and cost of goods sold using FIFO and LIFO. (LO 2) $14,442 Instructions (a) Compute the ending inventory at September 30 and cost of goods sold using the FIFO and LIFO methods. Prove the amount allocated to cost of goods sold under each method. (b) For both FIFO and LIFO, calculate the sum of ending inventory and cost of goods sold. What do you notice about the answers you found for each method? E6-5 Xiong Co. uses a periodic inventory system. Its records show the following for the month of May, in which 65 units were sold. May 1 15 24 Inventory Purchases Purchases Units Unit Cost Total Cost 30 25 35 $ 8 11 12 $240 275 420 Compute inventory and cost of goods sold using FIFO and LIFO. (LO 2) Totals 90 $935 Instructions Compute the ending inventory at May 31 and cost of goods sold using the FIFO and LIFO methods. Prove the amount allocated to cost of goods sold under each method. E6-6 Kaleta Company reports the following for the month of June. June 1 12 23 30 Inventory Purchase Purchase Inventory Units Unit Cost Total Cost 200 400 300 100 $5 6 7 $1,000 2,400 2,100 Compute inventory and cost of goods sold using FIFO and LIFO. (LO 2, 3) Instructions (a) Compute the cost of the ending inventory and the cost of goods sold under (1) FIFO and (2) LIFO. (b) Which costing method gives the higher ending inventory? Why? (c) Which method results in the higher cost of goods sold? Why? E6-7 Lisa Company had 100 units in beginning inventory at a total cost of $10,000. The company purchased 200 units at a total cost of $26,000. At the end of the year, Lisa had 80 units in ending inventory. Instructions (a) Compute the cost of the ending inventory and the cost of goods sold under (1) FIFO, (2) LIFO, and (3) average-cost. (b) Which cost flow method would result in the highest net income? (c) Which cost flow method would result in inventories approximating current cost in the balance sheet? (d) Which cost flow method would result in Lisa paying the least taxes in the first year? E6-8 Inventory data for Kaleta Company are presented in E6-6. Instructions (a) Compute the cost of the ending inventory and the cost of goods sold using the averagecost method. (b) Will the results in (a) be higher or lower than the results under (1) FIFO and (2) LIFO? (c) Why is the average unit cost not $6? Compute inventory under FIFO, LIFO, and average-cost. (LO 2, 3) Compute inventory and cost of goods sold using average-cost. (LO 2, 3) 310 6 Inventories Determine ending inventory under LCM. (LO 4) E6-9 Optix Camera Shop uses the lower-of-cost-or-market basis for its inventory. The following data are available at December 31. Item Units Unit Cost Market 5 6 $170 150 $156 152 12 14 125 120 115 135 Cameras: Minolta Canon Light meters: Vivitar Kodak Instructions Determine the amount of the ending inventory by applying the lower-of-cost-or-market basis. Compute lower-of-costor-market. (LO 4) E6-10 Serebin Company applied FIFO to its inventory and got the following results for its ending inventory. Cameras DVD players iPods 100 units at a cost per unit of $65 150 units at a cost per unit of $75 125 units at a cost per unit of $80 The cost of purchasing units at year-end was cameras $71, DVD players $67, and iPods $78. Instructions Determine the amount of ending inventory at lower-of-cost-or-market. Determine effects of inventory errors. (LO 5) E6-11 Hamid’s Hardware reported cost of goods sold as follows. Beginning inventory Cost of goods purchased Cost of goods available for sale Ending inventory Cost of goods sold 2013 2014 $ 20,000 150,000 $ 30,000 175,000 170,000 30,000 205,000 35,000 $140,000 $170,000 Hamid’s made two errors: (1) 2013 ending inventory was overstated $3,000, and (2) 2014 ending inventory was understated $6,000. Instructions Compute the correct cost of goods sold for each year. Prepare correct income statements. (LO 5) E6-12 Rulix Watch Company reported the following income statement data for a 2-year period. 2013 2014 Sales revenue Cost of goods sold Beginning inventory Cost of goods purchased Cost of goods available for sale Ending inventory Cost of goods sold Gross profit $220,000 $250,000 32,000 173,000 44,000 202,000 205,000 44,000 246,000 52,000 161,000 194,000 $ 59,000 $ 56,000 Rulix uses a periodic inventory system. The inventories at January 1, 2013, and December 31, 2014, are correct. However, the ending inventory at December 31, 2013, was overstated $6,000. Instructions (a) Prepare correct income statement data for the 2 years. (b) What is the cumulative effect of the inventory error on total gross profit for the 2 years? (c) Explain in a letter to the president of Rulix Watch Company what has happened, i.e., the nature of the error and its effect on the financial statements. Exercises E6-13 This information is available for Quick’s Photo Corporation for 2012, 2013, and 2014. Beginning inventory Ending inventory Cost of goods sold Sales revenue 2012 2013 2014 $ 100,000 300,000 900,000 1,200,000 $ 300,000 400,000 1,120,000 1,600,000 $ 400,000 480,000 1,300,000 1,900,000 311 Compute inventory turnover, days in inventory, and gross profit rate. (LO 6) Instructions Calculate inventory turnover, days in inventory, and gross profit rate (from Chapter 5) for Quick’s Photo Corporation for 2012, 2013, and 2014. Comment on any trends. E6-14 The cost of goods sold computations for Alpha Company and Omega Company are shown below. Alpha Company Omega Company Beginning inventory Cost of goods purchased $ 45,000 200,000 $ 71,000 290,000 245,000 55,000 361,000 69,000 $190,000 $292,000 Cost of goods available for sale Ending inventory Cost of goods sold Compute inventory turnover and days in inventory. (LO 6) Instructions (a) Compute inventory turnover and days in inventory for each company. (b) Which company moves its inventory more quickly? *E6-15 Bufford Appliance uses a perpetual inventory system. For its flat-screen television sets, the January 1 inventory was 3 sets at $600 each. On January 10, Bufford purchased 6 units at $660 each. The company sold 2 units on January 8 and 4 units on January 15. Apply cost flow methods to perpetual records. (LO 7) Instructions Compute the ending inventory under (1) FIFO, (2) LIFO, and (3) moving-average cost. *E6-16 Kaleta Company reports the following for the month of June. Date Explanation Units Unit Cost Total Cost June 1 12 23 30 Inventory Purchase Purchase Inventory 200 400 300 100 $5 6 7 $1,000 2,400 2,100 Calculate inventory and cost of goods sold using three cost flow methods in a perpetual inventory system. (LO 7) Instructions (a) Calculate the cost of the ending inventory and the cost of goods sold for each cost flow assumption, using a perpetual inventory system. Assume a sale of 440 units occurred on June 15 for a selling price of $8 and a sale of 360 units on June 27 for $9. (b) How do the results differ from E6-6 and E6-8? (c) Why is the average unit cost not $6 [($5 1 $6 1 $7) 4 3 5 $6]? *E6-17 Information about Linda’s Boards is presented in E6-4. Additional data regarding Linda’s sales of Xpert snowboards are provided below. Assume that Linda’s uses a perpetual inventory system. Date Sept. 5 Sept. 16 Sept. 29 Sale Sale Sale Totals Units Unit Price Total Revenue 12 50 59 $199 199 209 $ 2,388 9,950 12,331 121 $24,669 Instructions (a) Compute ending inventory at September 30 using FIFO, LIFO, and moving-average cost. (b) Compare ending inventory using a perpetual inventory system to ending inventory using a periodic inventory system (from E6-4). (c) Which inventory cost flow method (FIFO, LIFO) gives the same ending inventory value under both periodic and perpetual? Which method gives different ending inventory values? Apply cost flow methods to perpetual records. (LO 7) 312 6 Inventories Use the gross profit method to *E6-18 Brenda Company reported the following information for November and December estimate inventory. 2014. (LO 8) Cost of goods purchased Inventory, beginning-of-month Inventory, end-of-month Sales revenue November December $536,000 130,000 120,000 840,000 $ 610,000 120,000 ? 1,000,000 Brenda’s ending inventory at December 31 was destroyed in a fire. Instructions (a) Compute the gross profit rate for November. (b) Using the gross profit rate for November, determine the estimated cost of inventory lost in the fire. Determine merchandise lost using the gross profit method of estimating inventory. (LO 8) *E6-19 The inventory of Hauser Company was destroyed by fire on March 1. From an examination of the accounting records, the following data for the first 2 months of the year are obtained: Sales Revenue $51,000, Sales Returns and Allowances $1,000, Purchases $31,200, Freight-In $1,200, and Purchase Returns and Allowances $1,400. Instructions Determine the merchandise lost by fire, assuming: (a) A beginning inventory of $20,000 and a gross profit rate of 40% on net sales. (b) A beginning inventory of $30,000 and a gross profit rate of 30% on net sales. Determine ending inventory at cost using retail method. (LO 8) *E6-20 Gepetto Shoe Store uses the retail inventory method for its two departments, Women’s Shoes and Men’s Shoes. The following information for each department is obtained. Item Women’s Shoes Men’s Shoes Beginning inventory at cost Cost of goods purchased at cost Net sales Beginning inventory at retail Cost of goods purchased at retail $ 25,000 110,000 178,000 46,000 179,000 $ 45,000 136,300 185,000 60,000 185,000 Instructions Compute the estimated cost of the ending inventory for each department under the retail inventory method. EXERCISES: SET B AND CHALLENGE EXERCISES Visit the book’s companion website, at www.wiley.com/college/weygandt, and choose the Student Companion site to access Exercise Set B and Challenge Exercises. PROBLEMS: SET A Determine items and amounts to be recorded in inventory. P6-1A Austin Limited is trying to determine the value of its ending inventory as of February 28, 2014, the company’s year-end. The following transactions occurred, and the accountant asked your help in determining whether they should be recorded or not. (LO 1) (a) On February 26, Austin shipped goods costing $800 to a customer and charged the customer $1,000. The goods were shipped with terms FOB shipping point and the receiving report indicates that the customer received the goods on March 2. (b) On February 26, Louis Inc. shipped goods to Austin under terms FOB shipping point. The invoice price was $450 plus $30 for freight. The receiving report indicates that the goods were received by Austin on March 2. (c) Austin had $650 of inventory isolated in the warehouse. The inventory is designated for a customer who has requested that the goods be shipped on March 10. Problems: Set A 313 (d) Also included in Austin’s warehouse is $700 of inventory that Ryhn Producers shipped to Austin on consignment. (e) On February 26, Austin issued a purchase order to acquire goods costing $900. The goods were shipped with terms FOB destination on February 27. Austin received the goods on March 2. (f) On February 26, Austin shipped goods to a customer under terms FOB destination. The invoice price was $350; the cost of the items was $200. The receiving report indicates that the goods were received by the customer on March 2. Instructions For each of the above transactions, specify whether the item in question should be included in ending inventory, and if so, at what amount. P6-2A Express Distribution markets CDs of the performing artist Fishe. At the beginning of October, Express had in beginning inventory 2,000 of Fishe’s CDs with a unit cost of $7. During October, Express made the following purchases of Fishe’s CDs. Oct. 3 2,500 @ $8 Oct. 9 3,500 @ $9 Oct. 19 3,000 @ $10 Oct. 25 4,000 @ $11 Determine cost of goods sold and ending inventory using FIFO, LIFO, and average-cost with analysis. (LO 2, 3) During October, 10,900 units were sold. Express uses a periodic inventory system. Instructions (a) Determine the cost of goods available for sale. (b) Determine (1) the ending inventory and (2) the cost of goods sold under each of the assumed cost flow methods (FIFO, LIFO, and average-cost). Prove the accuracy of the cost of goods sold under the FIFO and LIFO methods. (c) Which cost flow method results in (1) the highest inventory amount for the balance sheet and (2) the highest cost of goods sold for the income statement? P6-3A Ziad Company had a beginning inventory on January 1 of 150 units of Product 4-18-15 at a cost of $20 per unit. During the year, the following purchases were made. Mar. 15 400 units at $23 July 20 250 units at $24 Sept. 4 350 units at $26 Dec. 2 100 units at $29 (b)(2) Cost of goods sold: FIFO $ 94,500 LIFO $108,700 Average $101,370 Determine cost of goods sold and ending inventory, using FIFO, LIFO, and average-cost with analysis. (LO 2, 3) 1,000 units were sold. Ziad Company uses a periodic inventory system. Instructions (a) Determine the cost of goods available for sale. (b) Determine (1) the ending inventory, and (2) the cost of goods sold under each of the assumed cost flow methods (FIFO, LIFO, and average-cost). Prove the accuracy of the cost of goods sold under the FIFO and LIFO methods. (c) Which cost flow method results in (1) the highest inventory amount for the balance sheet, and (2) the highest cost of goods sold for the income statement? (b)(2) Cost of goods sold: FIFO $23,400 LIFO $24,900 Average $24,160 P6-4A The management of Felipe Inc. is reevaluating the appropriateness of using its present inventory cost flow method, which is average-cost. The company requests your help in determining the results of operations for 2014 if either the FIFO or the LIFO method had been used. For 2014, the accounting records show these data: Compute ending inventory, prepare income statements, and answer questions using FIFO and LIFO. Inventories Beginning (7,000 units) Ending (17,000 units) (LO 2, 3) Purchases and Sales $14,000 Total net sales (180,000 units) Total cost of goods purchased (190,000 units) $747,000 466,000 Purchases were made quarterly as follows. Quarter Units Unit Cost Total Cost 1 2 3 4 50,000 40,000 40,000 60,000 $2.20 2.35 2.50 2.70 $110,000 94,000 100,000 162,000 190,000 $466,000 Operating expenses were $130,000, and the company’s income tax rate is 40%. Instructions (a) Prepare comparative condensed income statements for 2014 under FIFO and LIFO. (Show computations of ending inventory.) (a) Gross profit: FIFO $312,900 LIFO $303,000 314 6 Inventories (b) Calculate ending inventory, cost of goods sold, gross profit, and gross profit rate under periodic method; compare results. (LO 2, 3) (a) (iii) Gross profit: LIFO $4,215 FIFO $4,645 Average $4,414.60 Compare specific identification, FIFO, and LIFO under periodic method; use cost flow assumption to justify price increase. (LO 2, 3) (a) Gross profit: (1) Specific identification $3,715 (2) FIFO (3) LIFO $3,930 $3,385 Compute ending inventory, prepare income statements, and answer questions using FIFO and LIFO. (LO 2, 3) Answer the following questions for management. (1) Which cost flow method (FIFO or LIFO) produces the more meaningful inventory amount for the balance sheet? Why? (2) Which cost flow method (FIFO or LIFO) produces the more meaningful net income? Why? (3) Which cost flow method (FIFO or LIFO) is more likely to approximate the actual physical flow of goods? Why? (4) How much more cash will be available for management under LIFO than under FIFO? Why? (5) Will gross profit under the average-cost method be higher or lower than FIFO? Than LIFO? (Note: It is not necessary to quantify your answer.) P6-5A You are provided with the following information for Najera Inc. for the month ended June 30, 2014. Najera uses the periodic method for inventory. Date Description Quantity Unit Cost or Selling Price June 1 June 4 June 10 June 11 June 18 June 18 June 25 June 28 Beginning inventory Purchase Sale Sale return Purchase Purchase return Sale Purchase 40 135 110 15 55 10 65 30 $40 44 70 70 46 46 75 50 Instructions (a) Calculate (i) ending inventory, (ii) cost of goods sold, (iii) gross profit, and (iv) gross profit rate under each of the following methods. (1) LIFO. (2) FIFO. (3) Average-cost. (b) Compare results for the three cost flow assumptions. P6-6A You are provided with the following information for Barton Inc. Barton Inc. uses the periodic method of accounting for its inventory transactions. March 1 March 3 March 5 March 10 March 20 March 30 Beginning inventory 2,000 liters at a cost of 60¢ per liter. Purchased 2,500 liters at a cost of 65¢ per liter. Sold 2,300 liters for $1.05 per liter. Purchased 4,000 liters at a cost of 72¢ per liter. Purchased 2,500 liters at a cost of 80¢ per liter. Sold 5,200 liters for $1.25 per liter. Instructions (a) Prepare partial income statements through gross profit, and calculate the value of ending inventory that would be reported on the balance sheet, under each of the following cost flow assumptions. (Round ending inventory and cost of goods sold to the nearest dollar.) (1) Specific identification method assuming: (i) The March 5 sale consisted of 1,000 liters from the March 1 beginning inventory and 1,300 liters from the March 3 purchase; and (ii) The March 30 sale consisted of the following number of units sold from beginning inventory and each purchase: 450 liters from March 1; 550 liters from March 3; 2,900 liters from March 10; 1,300 liters from March 20. (2) FIFO. (3) LIFO. (b) How can companies use a cost flow method to justify price increases? Which cost flow method would best support an argument to increase prices? P6-7A The management of Sherlynn Co. asks your help in determining the comparative effects of the FIFO and LIFO inventory cost flow methods. For 2014, the accounting records provide the following data. Problems: Set A Inventory, January 1 (10,000 units) Cost of 100,000 units purchased Selling price of 80,000 units sold Operating expenses 315 $ 45,000 532,000 700,000 140,000 Units purchased consisted of 35,000 units at $5.10 on May 10; 35,000 units at $5.30 on August 15; and 30,000 units at $5.60 on November 20. Income taxes are 30%. Instructions (a) Prepare comparative condensed income statements for 2014 under FIFO and LIFO. (Show computations of ending inventory.) (b) Answer the following questions for management. (1) Which inventory cost flow method produces the most meaningful inventory amount for the balance sheet? Why? (2) Which inventory cost flow method produces the most meaningful net income? Why? (3) Which inventory cost flow method is most likely to approximate actual physical flow of the goods? Why? (4) How much additional cash will be available for management under LIFO than under FIFO? Why? (5) How much of the gross profit under FIFO is illusory in comparison with the gross profit under LIFO? *P6-8A Mercer Inc. is a retailer operating in British Columbia. Mercer uses the perpetual inventory method. All sales returns from customers result in the goods being returned to inventory; the inventory is not damaged. Assume that there are no credit transactions; all amounts are settled in cash. You are provided with the following information for Mercer Inc. for the month of January 2014. Date Description Quantity Unit Cost or Selling Price January 1 January 5 January 8 January 10 January 15 January 16 January 20 January 25 Beginning inventory Purchase Sale Sale return Purchase Purchase return Sale Purchase 100 140 110 10 55 5 90 20 $15 18 28 28 20 20 32 22 Instructions (a) For each of the following cost flow assumptions, calculate (i) cost of goods sold, (ii) ending inventory, and (iii) gross profit. (1) LIFO. (2) FIFO. (3) Moving-average cost. (b) Compare results for the three cost flow assumptions. *P6-9A Terando Co. began operations on July 1. It uses a perpetual inventory system. During July, the company had the following purchases and sales. Purchases Date July July July July July July 1 6 11 14 21 27 Units Unit Cost 5 $120 7 $136 8 $147 (a) Net income FIFO $105,700 LIFO $91,000 Calculate cost of goods sold and ending inventory under LIFO, FIFO, and movingaverage cost under the perpetual system; compare gross profit under each assumption. (LO 7) (a)(iii) Gross profit: LIFO $2,160 FIFO $2,560 Average $2,421 Determine ending inventory under a perpetual inventory system. (LO 7) Sales Units 4 3 6 Instructions (a) Determine the ending inventory under a perpetual inventory system using (1) FIFO, (2) moving-average cost, and (3) LIFO. (b) Which costing method produces the highest ending inventory valuation? (a) Ending inventory FIFO $1,029 Avg. $994 LIFO $958 316 6 Inventories Compute gross profit rate and inventory loss using gross profit method. *P6-10A Suzuki Company lost all of its inventory in a fire on December 26, 2014. The accounting records showed the following gross profit data for November and December. (LO 8) Net sales Beginning inventory Purchases Purchase returns and allowances Purchase discounts Freight-in Ending inventory November December (to 12/26) $600,000 32,000 389,000 13,300 8,500 8,800 36,000 $700,000 36,000 420,000 14,900 9,500 9,900 ? Suzuki is fully insured for fire losses but must prepare a report for the insurance company. (a) Gross profit rate 38% Compute ending inventory using retail method. (LO 8) Instructions (a) Compute the gross profit rate for November. (b) Using the gross profit rate for November, determine the estimated cost of the inventory lost in the fire. *P6-11A Dixon Books uses the retail inventory method to estimate its monthly ending inventories. The following information is available for two of its departments at October 31, 2014. Hardcovers Beginning inventory Purchases Freight-in Purchase discounts Net sales Paperbacks Cost Retail Cost Retail $ 420,000 2,135,000 24,000 44,000 $ 700,000 3,200,000 $ 280,000 1,155,000 12,000 22,000 $ 360,000 1,540,000 3,100,000 1,570,000 At December 31, Dixon Books takes a physical inventory at retail. The actual retail values of the inventories in each department are Hardcovers $790,000 and Paperbacks $335,000. (a) Hardcovers: End. Inv. $520,000 Instructions (a) Determine the estimated cost of the ending inventory for each department at October 31, 2014, using the retail inventory method. (b) Compute the ending inventory at cost for each department at December 31, assuming the cost-to-retail ratios for the year are 65% for Hardcovers and 75% for Paperbacks. PROBLEMS: SET B Determine items and amounts to be recorded in inventory. (LO 1) P6-1B Weber Limited is trying to determine the value of its ending inventory at February 28, 2014, the company’s year-end. The accountant counted everything that was in the warehouse as of February 28, which resulted in an ending inventory valuation of $48,000. However, she didn’t know how to treat the following transactions so she didn’t record them. (a) On February 26, Weber shipped to a customer goods costing $800. The goods were shipped FOB shipping point, and the receiving report indicates that the customer received the goods on March 2. (b) On February 26, Gretel Inc. shipped goods to Weber FOB destination. The invoice price was $350. The receiving report indicates that the goods were received by Weber on March 2. (c) Weber had $500 of inventory at a customer’s warehouse “on approval.” The customer was going to let Weber know whether it wanted the merchandise by the end of the week, March 4. (d) Weber also had $400 of inventory on consignment at a Roslyn craft shop. (e) On February 26, Weber ordered goods costing $750. The goods were shipped FOB shipping point on February 27. Weber received the goods on March 1. Problems: Set B 317 (f) On February 28, Weber packaged goods and had them ready for shipping to a customer FOB destination. The invoice price was $350; the cost of the items was $250. The receiving report indicates that the goods were received by the customer on March 2. (g) Weber had damaged goods set aside in the warehouse because they are no longer saleable. These goods cost $400 and Weber originally expected to sell these items for $600. Instructions For each of the above transactions, specify whether the item in question should be included in ending inventory and, if so, at what amount. For each item that is not included in ending inventory, indicate who owns it and in what account, if any, it should have been recorded. P6-2B Xinxin Distribution markets CDs of the performing artist Carly. At the beginning of March, Xinxin had in beginning inventory 1,500 Carly CDs with a unit cost of $7. During March Xinxin made the following purchases of Carly CDs. March 5 March 13 3,000 @ $8 4,500 @ $9 March 21 March 26 4,000 @ $10 2,500 @ $11 Determine cost of goods sold and ending inventory using FIFO, LIFO, and average-cost with analysis. (LO 2, 3) During March, 12,000 units were sold. Xinxin uses a periodic inventory system. Instructions (a) Determine the cost of goods available for sale. (b) Determine (1) the ending inventory and (2) the cost of goods sold under each of the assumed cost flow methods (FIFO, LIFO, and average-cost). Prove the accuracy of the cost of goods sold under the FIFO and LIFO methods. (c) Which cost flow method results in (1) the highest inventory amount for the balance sheet and (2) the highest cost of goods sold for the income statement? P6-3B Walz Company had a beginning inventory of 400 units of Product Ribo at a cost of $8 per unit. During the year, purchases were: Feb. 20 May 5 600 units at $9 500 units at $10 Aug. 12 Dec. 8 300 units at $11 200 units at $12 (b)(2) Cost of goods sold: FIFO $105,000 LIFO $116,000 Average $110,321 Determine cost of goods sold and ending inventory using FIFO, LIFO, and average-cost with analysis. (LO 2, 3) Walz Company uses a periodic inventory system. Sales totaled 1,500 units. Instructions (a) Determine the cost of goods available for sale. (b) Determine (1) the ending inventory and (2) the cost of goods sold under each of the assumed cost flow methods (FIFO, LIFO, and average-cost). Prove the accuracy of the cost of goods sold under the FIFO and LIFO methods. (c) Which cost flow method results in (1) the lowest inventory amount for the balance sheet, and (2) the lowest cost of goods sold for the income statement? (b) Cost of goods sold: FIFO $13,600 LIFO $15,200 Average $14,475 P6-4B The management of Patel Co. is reevaluating the appropriateness of using its present inventory cost flow method, which is average-cost. They request your help in determining the results of operations for 2014 if either the FIFO method or the LIFO method had been used. For 2014, the accounting records show the following data. Compute ending inventory, prepare income statements, and answer questions using FIFO and LIFO. Inventories Beginning (15,000 units) Ending (28,000 units) (LO 2, 3) Purchases and Sales $32,000 Total net sales (217,000 units) Total cost of goods purchased (230,000 units) $865,000 Purchases were made quarterly as follows. Quarter Units Unit Cost Total Cost 1 2 3 4 60,000 50,000 50,000 70,000 $2.40 2.50 2.70 2.80 $144,000 125,000 135,000 196,000 230,000 $600,000 Operating expenses were $147,000, and the company’s income tax rate is 34%. 600,000 318 6 Inventories (a) Net income FIFO $108,504 LIFO $98,472 (b)(4) $5,168 Calculate ending inventory, cost of goods sold, gross profit, and gross profit rate under periodic method; compare results. (LO 2, 3) (a)(iii) Gross profit: LIFO $3,050 FIFO $3,230 Average $3,141 Compare specific identification, FIFO and LIFO under periodic method; use cost flow assumption to influence earnings. (LO 2, 3) (a) Gross profit: (1) Maximum $163,600 (2) Minimum $154,000 Compute ending inventory, prepare income statements, and answer questions using FIFO and LIFO. (LO 2, 3) Instructions (a) Prepare comparative condensed income statements for 2014 under FIFO and LIFO. (Show computations of ending inventory.) (b) Answer the following questions for management. (1) Which cost flow method (FIFO or LIFO) produces the more meaningful inventory amount for the balance sheet? Why? (2) Which cost flow method (FIFO or LIFO) produces the more meaningful net income? Why? (3) Which cost flow method (FIFO or LIFO) is more likely to approximate actual physical flow of the goods? Why? (4) How much additional cash will be available for management under LIFO than under FIFO? Why? (5) Will gross profit under the average-cost method be higher or lower than (i) FIFO and (ii) LIFO? (Note: It is not necessary to quantify your answer.) P6-5B You are provided with the following information for Perkins Inc. for the month ended October 31, 2014. Perkins uses a periodic method for inventory. Date Description Units Unit Cost or Selling Price October 1 October 9 October 11 October 17 October 22 October 25 October 29 Beginning inventory Purchase Sale Purchase Sale Purchase Sale 60 120 100 70 60 80 110 $25 26 35 27 40 28 40 Instructions (a) Calculate (i) ending inventory, (ii) cost of goods sold, (iii) gross profit, and (iv) gross profit rate under each of the following methods. (1) LIFO. (2) FIFO. (3) Average-cost. (b) Compare results for the three cost flow assumptions. P6-6B You have the following information for Princess Diamonds. Princess Diamonds uses the periodic method of accounting for its inventory transactions. Princess only carries one brand and size of diamonds—all are identical. Each batch of diamonds purchased is carefully coded and marked with its purchase cost. March 1 March 3 March 5 March 10 March 25 Beginning inventory 150 diamonds at a cost of $300 per diamond. Purchased 200 diamonds at a cost of $360 each. Sold 180 diamonds for $600 each. Purchased 350 diamonds at a cost of $380 each. Sold 400 diamonds for $650 each. Instructions (a) Assume that Princess Diamonds uses the specific identification cost flow method. (1) Demonstrate how Princess Diamonds could maximize its gross profit for the month by specifically selecting which diamonds to sell on March 5 and March 25. (2) Demonstrate how Princess Diamonds could minimize its gross profit for the month by selecting which diamonds to sell on March 5 and March 25. (b) Assume that Princess Diamonds uses the FIFO cost flow assumption. Calculate cost of goods sold. How much gross profit would Princess Diamonds report under this cost flow assumption? (c) Assume that Princess Diamonds uses the LIFO cost flow assumption. Calculate cost of goods sold. How much gross profit would the company report under this cost flow assumption? (d) Which cost flow method should Princess Diamonds select? Explain. P6-7B The management of Chelsea Inc. asks your help in determining the comparative effects of the FIFO and LIFO inventory cost flow methods. For 2014, the accounting records provide the following data. Problems: Set B Inventory, January 1 (10,000 units) Cost of 120,000 units purchased Selling price of 100,000 units sold Operating expenses 319 $ 35,000 504,500 665,000 130,000 Units purchased consisted of 35,000 units at $4.00 on May 10; 60,000 units at $4.20 on August 15; and 25,000 units at $4.50 on November 20. Income taxes are 28%. Instructions (a) Prepare comparative condensed income statements for 2014 under FIFO and LIFO. (Show computations of ending inventory.) (b) Answer the following questions for management in the form of a business letter. (1) Which inventory cost flow method produces the most meaningful inventory amount for the balance sheet? Why? (2) Which inventory cost flow method produces the most meaningful net income? Why? (3) Which inventory cost flow method is most likely to approximate the actual physical flow of the goods? Why? (4) How much more cash will be available for management under LIFO than under FIFO? Why? (5) How much of the gross profit under FIFO is illusionary in comparison with the gross profit under LIFO? *P6-8B Minsoo Ltd. is a retailer operating in Edmonton, Alberta. Minsoo uses the perpetual inventory method. All sales returns from customers result in the goods being returned to inventory; the inventory is not damaged. Assume that there are no credit transactions; all amounts are settled in cash. You are provided with the following information for Minsoo Ltd. for the month of January 2014. Date Description Quantity Unit Cost or Selling Price December 31 January 2 January 6 January 9 January 9 January 10 January 10 January 23 January 30 Ending inventory Purchase Sale Sale return Purchase Purchase return Sale Purchase Sale 160 100 150 10 80 10 60 100 110 $17 21 40 40 24 24 45 28 50 Instructions (a) For each of the following cost flow assumptions, calculate (i) cost of goods sold, (ii) ending inventory, and (iii) gross profit. (1) LIFO. (2) FIFO. (3) Moving-average cost. (b) Compare results for the three cost flow assumptions. *P6-9B Buffet Appliance Mart began operations on May 1. It uses a perpetual inventory system. During May, the company had the following purchases and sales for its Model 25 Sureshot camera. Units Unit Cost May 1 4 8 12 15 20 25 7 $150 8 $170 6 $185 Calculate cost of goods sold and ending inventory for FIFO, moving-average cost, and LIFO under the perpetual system; compare gross profit under each assumption. (LO 7) (a)(iii) Gross profit: LIFO $6,540 FIFO $7,780 Average $7,354 Determine ending inventory under a perpetual inventory system. (LO 7) Purchases Date (a) Gross profit: FIFO $259,000 LIFO $240,500 Sales Units 4 5 3 4 Instructions (a) Determine the ending inventory under a perpetual inventory system using (1) FIFO, (2) moving-average cost, and (3) LIFO. (b) Which costing method produces (1) the highest ending inventory valuation and (2) the lowest ending inventory valuation? $925 (a) FIFO Average $874 LIFO $790 320 6 Inventories Estimate inventory loss using gross profit method. *P6-10B Liis Company lost 70% of its inventory in a fire on March 25, 2014. The accounting records showed the following gross profit data for February and March. (LO 8) Net sales Net purchases Freight-in Beginning inventory Ending inventory February March (to 3/25) $300,000 176,800 3,900 4,500 20,200 $250,000 139,000 3,000 20,200 ? Liis Company is fully insured for fire losses but must prepare a report for the insurance company. (a) Gross profit rate 45% Compute ending inventory using retail method. (LO 8) Instructions (a) Compute the gross profit rate for the month of February. (b) Using the gross profit rate for February, determine both the estimated total inventory and inventory lost in the fire in March. *P6-11B Belden Department Store uses the retail inventory method to estimate its monthly ending inventories. The following information is available for two of its departments at August 31, 2014. Sporting Goods Net sales Purchases Purchase returns Purchase discounts Freight-in Beginning inventory Jewelry and Cosmetics Cost Retail Cost Retail $675,000 (26,000) (12,360) 9,000 47,360 $1,000,000 1,066,000 (40,000) — — 74,000 $741,000 (12,000) (2,440) 14,000 39,440 $1,160,000 1,158,000 (20,000) — — 62,000 At December 31, Belden Department Store takes a physical inventory at retail. The actual retail values of the inventories in each department are Sporting Goods $95,000 and Jewelry and Cosmetics $44,000. (b) Sporting Goods: End. Inv. $63,000 Instructions (a) Determine the estimated cost of the ending inventory for each department on August 31, 2014, using the retail inventory method. (b) Compute the ending inventory at cost for each department at December 31, assuming the cost-to-retail ratios are 60% for Sporting Goods and 64% for Jewelry and Cosmetics. SOLUTIONS TO BRIEF EXERCISES BRIEF EXERCISE 6-1 (a) Ownership of the goods belongs to Farley. Thus, these goods should be included in Farley’s inventory. (b) The goods in transit should not be included in the inventory count because ownership by Farley does not occur until the goods reach the buyer. (c) The goods being held belong to the customer. They should not be included in Farley’s inventory. (d) Ownership of these goods rests with the other company. Thus, these goods should not be included in the physical inventory. BRIEF EXERCISE 6-2 The items that should be included in goods available for sale are: (a) (b) (c) (e) Freight-In Purchase Returns and Allowances Purchases Purchase Discounts BRIEF EXERCISE 6-3 (a) The ending inventory under FIFO consists of 200 units at $8 + 160 units at $7 for a total allocation of $2,720 or ($1,600 + $1,120). (b) The ending inventory under LIFO consists of 300 units at $6 + 60 units at $7 for a total allocation of $2,220 or ($1,800 + $420). 6-10 Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) BRIEF EXERCISE 6-4 Average unit cost is $6.89 computed as follows: 300 X $6 = $1,800 400 X $7 = 2,800 200 X $8 = 1,600 900 $6,200 $6,200 ÷ 900 = $6.89 (rounded). The cost of the ending inventory is $2,480 or (360 X $6.89). BRIEF EXERCISE 6-5 (a) (b) (c) (d) FIFO would result in the highest net income. FIFO would result in the highest ending inventory. LIFO would result in the lowest income tax expense (because it would result in the lowest net income). Average-cost would result in the most stable income over a number of years because it averages out any big changes in the cost of inventory. BRIEF EXERCISE 6-6 Cost of good sold under: Purchases Cost of goods available for sale Less: Ending inventory Cost of goods sold LIFO $6 X 120 $7 X 200 $8 X 140 $ 3,240 1,140 $ 2,100 FIFO $6 X 120 $7 X 200 $8 X 140 $ 3,240 1,400 $ 1,840 Since the cost of goods sold is $260 less under FIFO ($2,100 – $1,840) that is the amount of the phantom profit. It is referred to as “phantom profit” because FIFO matches current selling prices with old inventory costs. To replace the units sold, the company will have to pay the current price of $8 per unit, rather than the $6 per unit which some of the units were priced at under FIFO. Therefore, profit under LIFO is more representative of what the company can expect to earn in future periods. Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) 6-11 BRIEF EXERCISE 6-7 Inventory Categories Cameras Camcorders DVD players Total valuation Cost $12,000 9,500 14,000 Market $12,100 9,700 12,800 LCM $12,000 9,500 12,800 $34,300 BRIEF EXERCISE 6-8 The understatement of ending inventory caused cost of goods sold to be overstated $7,000 and net income to be understated $7,000. The correct net income for 2014 is $97,000 or ($90,000 + $7,000). Total assets in the balance sheet will be understated by the amount that ending inventory is understated, $7,000. BRIEF EXERCISE 6-9 Inventory turnover: Days in inventory: $270,000 $270,000 = = 5.4 ($60,000 + $40,000 ) ÷ 2 $50,000 365 = 67.6 days 5.4 *BRIEF EXERCISE 6-10 (a) FIFO Method Date May 7 June 1 July 28 Purchases (50 @ $10) $500 (26 @ $10) $260 (24 @ $10) (16 @ $13) } $448 (30 @ $13) $390 Aug. 27 6-12 Product E2-D2 Cost of Goods Sold Copyright © 2013 John Wiley & Sons, Inc. Balance (50 @ $10) $500 (24 @ $10) $240 (24 @ $10) (30 @ $13) } $630 (14 @ $13) Weygandt, Accounting Principles, 11/e, Solutions Manual $182 (For Instructor Use Only) *BRIEF EXERCISE 6-10 (Continued) (b) LIFO Method Date May 7 June 1 July 28 Purchases (50 @ $10) $500 Product E2-D2 Cost of Goods Sold (26 @ $10) $260 (30 @ $13) (10 @ $10) } $490 (30 @ $13) $390 Aug. 27 Balance (50 @ $10) $500 (24 @ $10) $240 (24 @ $10) (30 @ $13) } $630 (14 @ $10) $140 (c) Average-Cost Date May 7 June 1 July 28 Aug. 27 Purchases (50 @ $10) $500 Product E2-D2 Cost of Goods Sold (26 @ $10) $260 (30 @ $13) $390 (40 @ $11.67) $467 Balance (50 @ $10) $500 (24 @ $10) $240 (54 @ $11.67)*$630 (14 @ $11.67) $163 *($240 + $390) ÷ 54 *BRIEF EXERCISE 6-11 (1) Net sales .............................................................................. Less: Estimated gross profit (35% X $330,000) .............. Estimated cost of goods sold ............................................ $330,000 115,500 $214,500 (2) Cost of goods available for sale ........................................ Less: Estimated cost of goods sold ................................ Estimated cost of ending inventory .................................. $230,000 214,500 $ 15,500 *BRIEF EXERCISE 6-12 Goods available for sale Net sales Ending inventory at retail At Cost $38,000 At Retail $50,000 40,000 $10,000 Cost-to-retail ratio = ($38,000 ÷ $50,000) = 76% Estimated cost of ending inventory = ($10,000 X 76%) = $7,600 Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) 6-13 SOLUTIONS FOR DO IT! REVIEW EXERCISES DO IT! 6-1 Inventory per physical count .................................................... Inventory out on consignment ................................................. Inventory sold, in transit at year-end ....................................... Inventory purchased, in transit at year-end ............................ Correct December 31 inventory................................................ $300,000 26,000 –0– 17,000 $343,000 DO IT! 6-2 Cost of goods available for sale = (3,000 X $5) + (8,000 X $7) = $71,000 Ending inventory = 3,000 + 8,000 – 9,400 = 1,600 units (a) FIFO: $71,000 – (1,600 X $7) = $59,800 (b) LIFO: $71,000 – (1,600 X $5) = $63,000 (c) Average-cost: $71,000/11,000 = $6.455 per unit 9,400 X $6.455 = $60,677 DO IT! 6-3 (a) The lowest value for each inventory type is: Small $64,000, Medium $260,000, and Large $152,000. The total inventory value is the sum of these figures, $476,000. (b) Ending inventory Cost of goods sold Owner’s equity 6-14 2013 $31,000 understated $31,000 overstated $31,000 understated Copyright © 2013 John Wiley & Sons, Inc. 2014 No effect $31,000 understated No effect Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) DO IT! 6-4 2013 Inventory turnover $1,200,000 = 6 ($180,000 + $220,000)/2 Days in inventory 365 ÷ 6 = 60.8 days 2014 $1,425,000 ($220,000 + $100,000)/2 = 8.9 365 ÷ 8.9 = 41 days The company experienced a very significant decline in its ending inventory as a result of the just-in-time inventory. This decline improved its inventory turnover and its days in inventory. It is possible that this increase is the result of a more focused inventory policy. It appears that this change is a win-win situation for Chien Company. Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) 6-15 SOLUTIONS TO EXERCISES EXERCISE 6-1 Ending inventory—physical count ................................................. 1. No effect—title passes to purchaser upon shipment when terms are FOB shipping point ................................... 2. No effect—title does not transfer to Josef until goods are received ............................................................... 3. Add to inventory: Title passed to Josef when goods were shipped ......................................................................... 4. Add to inventory: Title remains with Josef until purchaser receives goods ................................................... 5. The goods did not arrive prior to year-end. The goods, therefore, cannot be included in the inventory .................. Correct inventory ............................................................................. $297,000 0 0 22,000 35,000 (44,000) $310,000 EXERCISE 6-2 Ending inventory—as reported ...................................................... 1. Subtract from inventory: The goods belong to Harmon Corporation. Schuda is merely holding them as a consignee ............................................................ 2. No effect—title does not pass to Schuda until goods are received (Jan. 3) ................................................. 3. Subtract from inventory: Office supplies should be carried in a separate account. They are not considered inventory held for resale.................................. 4. Add to inventory: The goods belong to Schuda until they are shipped (Jan. 1) ............................................. 5. Add to inventory: Reza Sales ordered goods with a cost of $8,000. Schuda should record the corresponding sales revenue of $10,000. Schuda’s decision to ship extra “unordered” goods does not constitute a sale. The manager’s statement that Reza could ship the goods back indicates that Schuda knows this over-shipment is not a legitimate sale. The manager acted unethically in an attempt to improve Schuda’s reported income by over-shipping ..................................... 6-16 Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual $740,000 (250,000) 0 (14,000) 28,000 52,000 (For Instructor Use Only) EXERCISE 6-2 (Continued) 6. Subtract from inventory: GAAP require that inventory be valued at the lower of cost or market. Obsolete parts should be adjusted from cost to zero if they have no other use. ............................................................................... Correct inventory.............................................................................. (40,000) $516,000 EXERCISE 6-3 (a) FIFO Cost of Goods Sold (#1012) $100 + (#1045) $90 = $190 (b) It could choose to sell specific units purchased at specific costs if it wished to impact earnings selectively. If it wished to minimize earnings it would choose to sell the units purchased at higher costs—in which case the Cost of Goods Sold would be $190. If it wished to maximize earnings it would choose to sell the units purchased at lower costs—in which case the cost of goods sold would be $170. (c) I recommend they use the FIFO method because it produces a more appropriate balance sheet valuation and reduces the opportunity to manipulate earnings. (The answer may vary depending on the method the student chooses.) EXERCISE 6-4 (a) FIFO Beginning inventory (26 X $97) .................................... $ 2,522 Purchases Sept. 12 (45 X $102) ................................................ $4,590 Sept. 19 (20 X $104) ................................................ 2,080 Sept. 26 (50 X $105) ................................................ 5,250 11,920 Cost of goods available for sale .................................. 14,442 Less: Ending inventory (20 X $105) ............................ 2,100 Cost of goods sold ........................................................ $12,342 Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) 6-17 EXERCISE 6-4 (Continued) Date 9/1 9/12 9/19 9/26 Units 26 45 20 30 121 Proof Unit Cost $ 97 102 104 105 Total Cost $ 2,522 4,590 2,080 3,150 $12,342 LIFO Cost of goods available for sale .......................................................... $14,442 Less: Ending inventory (20 X $97) ..................................................... 1,940 Cost of goods sold ............................................................................... $12,502 Date 9/26 9/19 9/12 9/1 Units 50 20 45 6 121 Proof Unit Cost $105 104 102 97 Total Cost $ 5,250 2,080 4,590 582 $12,502 (b) FIFO $2,100 (ending inventory) + $12,342 (COGS) = $14,442 LIFO $1,940 (ending inventory) + $12,502 (COGS) = $14,442 } Cost of goods available for sale Under both methods, the sum of the ending inventory and cost of goods sold equals the same amount, $14,442, which is the cost of goods available for sale. EXERCISE 6-5 FIFO Beginning inventory (30 X $8) ............................................... Purchases May 15 (25 X $11) ............................................................ May 24 (35 X $12) ............................................................ Cost of goods available for sale ............................................ Less: Ending inventory (25 X $12) ....................................... Cost of goods sold ................................................................. 6-18 Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual $240 $275 420 695 935 300 $635 (For Instructor Use Only) EXERCISE 6-5 (Continued) Date 5/1 5/15 5/24 Units 30 25 10 65 Proof Unit Cost $ 8 11 12 Total Cost $240 275 120 $635 LIFO Cost of goods available for sale .......................................................... Less: Ending inventory (25 X $8) ........................................................ Cost of goods sold ................................................................................ Date 5/24 5/15 5/1 Units 35 25 5 65 Proof Unit Cost $12 11 8 $935 200 $735 Total Cost $420 275 40 $735 EXERCISE 6-6 (a) FIFO Beginning inventory (200 X $5) ............................... Purchases June 12 (400 X $6) ............................................. June 23 (300 X $7) ............................................. Cost of goods available for sale .............................. Less: Ending inventory (100 X $7) ......................... Cost of goods sold ................................................... LIFO Cost of goods available for sale .............................. Less: Ending inventory (100 X $5) ......................... Cost of goods sold ................................................... Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual $1,000 $2,400 2,100 4,500 5,500 700 $4,800 $5,500 500 $5,000 (For Instructor Use Only) 6-19 EXERCISE 6-6 (Continued) (b) The FIFO method will produce the higher ending inventory because costs have been rising. Under this method, the earliest costs are assigned to cost of goods sold and the latest costs remain in ending inventory. For Kaleta Company, the ending inventory under FIFO is $700 or (100 X $7) compared to $500 or (100 X $5) under LIFO. (c) The LIFO method will produce the higher cost of goods sold for Kaleta Company. Under LIFO the most recent costs are charged to cost of goods sold and the earliest costs are included in the ending inventory. The cost of goods sold is $5,000 or [$5,500 – (100 X $5)] compared to $4,800 or ($5,500 – $700) under FIFO. EXERCISE 6-7 (a) (1) (2) (3) FIFO Beginning inventory .......................................... Purchases ........................................................... Cost of goods available for sale ....................... Less: ending inventory (80 X $130) ................. Cost of goods sold............................................. $10,000 26,000 36,000 10,400 $25,600 LIFO Beginning inventory .......................................... Purchases ........................................................... Cost of goods available for sale ....................... Less: ending inventory (80 X $100) ................. Cost of goods sold............................................. $10,000 26,000 36,000 8,000 $28,000 AVERAGE-COST Beginning inventory .......................................... Purchases ........................................................... Cost of goods available for sale ....................... Less: ending inventory (80 X $120) ................. Cost of goods sold............................................. $10,000 26,000 36,000 9,600 $26,400 (b) The use of FIFO would result in the highest net income since the earlier lower costs are matched with revenues. (c) The use of FIFO would result in inventories approximating current cost in the balance sheet, since the more recent units are assumed to be on hand. (d) The use of LIFO would result in Lisa paying the least taxes in the first year since income will be lower. 6-20 Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) EXERCISE 6-8 (a) Total Units Cost of Goods Available for Sale ÷ Available for Sale 900 $5,500 Ending inventory (100 X $6.11) Cost of goods sold (800 X $6.11) = Weighted Average Unit Cost $6.11 $ 611 4,889 (b) Ending inventory is lower than FIFO ($700) and higher than LIFO ($500). In contrast, cost of goods sold is higher than FIFO ($4,800) and lower than LIFO ($5,000). (c) The average-cost method uses a weighted-average unit cost, not a simple average of unit costs. EXERCISE 6-9 Lower -of-Cost -or-Market: Cost Market Cameras Minolta Canon Total $ 850 900 1,750 $ 780 912 1,692 $ 780 900 Light meters Vivitar Kodak Total Total inventory 1,500 1,680 3,180 $4,930 1,380 1,890 3,270 $4,962 1,380 1,680 $4,740 Market $ 7,100 10,050 9,750 $26,900 Lower -of-Costor-Market: $ 6,500 10,050 9,750 $26,300 EXERCISE 6-10 Cameras DVD players Ipods Total inventory Cost $ 6,500 11,250 10,000 $27,750 Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) 6-21 EXERCISE 6-11 Beginning inventory ............................................ Cost of goods purchased ................................... Cost of goods available for sale ......................... Corrected ending inventory ................................ Cost of goods sold .............................................. a $30,000 – $3,000 = $27,000. b 2013 $ 20,000 150,000 170,000 a 27,000 $143,000 2014 $ 27,000 175,000 202,000 b 41,000 $161,000 $35,000 + $6,000 = $41,000. EXERCISE 6-12 (a) Sales ................................................................. Cost of goods sold Beginning inventory ................................. Cost of goods purchased ........................ Cost of goods available for sale ............. Ending inventory ($44,000 – $6,000) ....... Cost of goods sold ................................... Gross profit ...................................................... 2013 $220,000 2014 $250,000 32,000 173,000 205,000 38,000 167,000 $ 53,000 38,000 202,000 240,000 52,000 188,000 $ 62,000 (b) The cumulative effect on total gross profit for the two years is zero as shown below: Incorrect gross profits: Correct gross profits: Difference $59,000 + $56,000 = $115,000 $53,000 + $62,000 = 115,000 $ 0 (c) Dear Mr./Ms. President: Because your ending inventory of December 31, 2013 was overstated by $6,000, your net income for 2013 was overstated by $6,000. For 2014 net income was understated by $6,000. In a periodic system, the cost of goods sold is calculated by deducting the cost of ending inventory from the total cost of goods you have available for sale in the period. Therefore, if this ending inventory figure is overstated, as it was in December 2013, then the cost of goods sold is understated and therefore net income will be overstated by that amount. Consequently, this overstated ending inventory figure goes on to become the next period’s beginning inventory amount and is a part of the total cost of goods available for sale. Therefore, the mistake repeats itself in the reverse. 6-22 Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) EXERCISE 6-12 (Continued) The error also affects the balance sheet at the end of 2013. The inventory reported in the balance sheet is overstated; therefore, total assets are overstated. The overstatement of the 2013 net income results in the capital account balance being overstated. The balance sheet at the end of 2014 is correct because the overstatement of the capital account at the end of 2013 is offset by the understatement of the 2014 net income and the inventory at the end of 2014 is correct. Thank you for allowing me to bring this to your attention. If you have any questions, please contact me at your convenience. Sincerely, EXERCISE 6-13 Inventory turnover 2012 2013 $900,000 ($100,000 + $300,000) ÷ 2 $1,120,000 ($300,000 + $400,000) ÷ 2 $900,000 $200,000 Days in inventory Gross profit rate 365 4.5 $1,120,000 $350,000 = 4.5 = 81.1 days $1,200,000 – $900,000 = 25% $1,200,000 365 3.2 2014 $1,300,000 ($400,000 + $480,000) ÷ 2 $1,300,000 $440,000 = 3.2 365 2.95 = 114.1 days $1,600,000 – $1,120,000 = 30% $1,600,000 = 2.95 = 123.7 days $1,900,000 – $1,300,000 = 32% $1,900,000 The inventory turnover decreased by approximately 34% from 2012 to 2014 while the days in inventory increased by almost 53% over the same time period. Both of these changes would be considered negative since it’s better to have a higher inventory turnover with a correspondingly lower days in inventory. However, Quick’s Photo gross profit rate increased by 28% from 2012 to 2014, which is a positive sign. Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) 6-23 EXERCISE 6-14 (a) Inventory Turnover Alpha Company Omega Company $190,000 ($45,000 + $55,000)/2 = 3.80 $292,000 ($71,000 + $69,000)/2 = 4.17 365/3.80 = 96 days 365/4.17 = 88 days Days in Inventory (b) Omega Company is moving its inventory more quickly, since its inventory turnover is higher, and its days in inventory is lower. *EXERCISE 6-15 (1) Date Purchases Jan. 1 8 10 (6 @ $660) $3,960 15 Purchases Jan. 1 8 10 (6 @ $660) $3,960 15 6-24 (2 @ $600) $1,200 (1 @ $600) (3 @ $660) $2,580 (2) Date FIFO Cost of Goods Sold Copyright © 2013 John Wiley & Sons, Inc. LIFO Cost of Goods Sold (2 @ $600) $1,200 (4 @ $660) $2,640 Balance (3 @ $600) $1,800 (1 @ $600) 600 (1 @ $600) 4,560 (6 @ $660) (3 @ $660) 1,980 Balance (3 @ $600) (1 @ $600) (1 @ $600) (6 @ $660) (1 @ $600) (2 @ $660) Weygandt, Accounting Principles, 11/e, Solutions Manual $1,800 600 4,560 1,920 (For Instructor Use Only) *EXERCISE 6-15 (Continued) MOVING-AVERAGE COST (3) Date Purchases Cost of Goods Sold Jan. 1 8 (2 @ $600) $1,200 10 (6 @ $660) $3,960 15 (4 @ $651.43) $2,606 Balance (3 @ $600) $1,800 (1 @ $600) 600 (7 @ $651.43)* 4,560 (3 @ $651.43) 1,954 *Average-cost = ($600 + $3,960) ÷ 7 = $651.43 (rounded) *EXERCISE 6-16 (a) The cost of goods available for sale is: June 1 Inventory 200 @ $5 June 12 Purchase 400 @ $6 June 23 Purchase 300 @ $7 Total cost of goods available for sale Date June 1 June 12 FIFO Cost of Goods Sold Purchases (400 @ $6) $2,400 June 15 June 23 Balance (200 @ $5) $1,000 (200 @ $5) $3,400 (400 @ $6) } (200 @ $5) (240 @ $6) $1,000 1,440 (300 @ $7) $2,100 June 27 $1,000 2,400 2,100 $5,500 (160 @ $6) (200 @ $7) 960 1,400 $4,800 (160 @ $6) (160 @ $6) (300 @ $7) (100 @ $7) $ 960 } $3,060 $ 700 Ending inventory: $700. Cost of goods sold: $5,500 – $700 = $4,800. Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) 6-25 *EXERCISE 6-16 (Continued) LIFO Cost of Goods Sold Purchases Date June 1 June 12 (400 @ $6) $2,400 Balance (200 @ $5) $1,000 (200 @ $5) $3,400 (400 @ $6) } June 15 (400 @ $6) (40 @ $5) $2,400 $ 200 June 23 (300 @ $7) $2,100 June 27 (300 @ $7) 60 @ $5 (160 @ $5) (160 @ $5) (300 @ $7) $ 800 } $2,900 $2,100 300 (100 @ $5) $5,000 $ 500 Ending inventory: $500. Cost of goods sold: $5,500 – $500 = $5,000. Date June 1 June 12 June 15 June 23 June 27 Purchases Moving-Average Cost Cost of Goods Sold (400 @ $6) $2,400 (440 @ $5.666) (300 @ $7) $2,100 (360 @ $6.537) Balance (200 @ $5) (600 @ $5.666) $2,493 (160 @ $5.666) (460 @ $6.537) $2,353 (100 @ $6.537) $4,846 $1,000 $3,400 $ 907 $3,007 $ 654 Ending inventory: $654. Cost of goods sold: $5,500 – $654 = $4,846. (b) FIFO gives the same ending inventory and cost of goods sold values under both the periodic and perpetual inventory system. LIFO and average-cost normally give different ending inventory and cost of goods sold values under the periodic and perpetual inventory systems, but in this case LIFO gives the same results. (c) The simple average would be [($5 + $6 + $7) ÷ 3)] or $6. However, the moving-average cost method uses a weighted-average unit cost that changes each time a purchase is made rather than a simple average. 6-26 Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) *EXERCISE 6-17 (a) Date 9/1 9/5 9/12 FIFO Cost of Goods Sold Purchases (12 @ $ 97) $1,164 (45 @ $102) $4,590 9/16 (14 @ $ 97) (36 @ $102) $5,030 9/19 (20 @ $104) $2,080 9/26 (50 @ $105) $5,250 9/29 Date 9/1 9/5 9/12 ( 9 @ $102) (20 @ $104) (30 @ $105) $6,148 LIFO Cost of Goods Sold Purchases (12 @ $ 97) $1,164 (45 @ $102) $4,590 9/16 (45 @ $102) ( 5 @ $ 97) $5,075 9/19 (20 @ $104) $2,080 9/26 (50 @ $105) $5,250 9/29 Copyright © 2013 John Wiley & Sons, Inc. (50 @ $105) ( 9 @ $104) $6,186 Weygandt, Accounting Principles, 11/e, Solutions Manual Balance (26 @ $ 97) $2,522 (14 @ $ 97) $1,358 (14 @ $ 97) $5,948 (45 @ $102) ( 9 @ $102) $ 918 ( 9 @ $102) (20 @ $104) $2,998 ( 9 @ $102) (20 @ $104) $8,248 (50 @ $105) (20 @ $105) $2,100 Balance (26 @ $ 97) $2,522 (14 @ $ 97) $1,358 (14 @ $ 97) $5,948 (45 @ $102) ( 9 @ $ 97) ( 9 @ $ 97) (20 @ $104) ( 9 @ $ 97) (20 @ $104) (50 @ $105) ( 9 @ $ 97) (11 @ $104) $ 873 $2,953 $8,203 $2,017 (For Instructor Use Only) 6-27 *EXERCISE 6-17 (Continued) Date 9/1 9/5 9/12 9/16 9/19 9/26 9/29 Purchases Moving-Average Cost Cost of Goods Sold (12 @ $97) $1,164 (50 @ $100.81) $5,041* (59 @ $104.27) $6,152* (45 @ $102) $4,590 (20 @ $104) $2,080 (50 @ $105) $5,250 Balance (26 @ $97) (14 @ $97) (59 @ $100.81)a ( 9 @ $100.81) (29 @ $103.00)b (79 @ $104.27)c (20 @ $104.27) $2,522 $1,358 $5,948 $ 907 $2,987 $8,237 $2,085 *Rounded a $5,948 ÷ 59 = $100.81 b $2,987 ÷ 29 = $103.00 c $8,237 ÷ 79 = $104.27 (b) Ending Inventory FIFO Ending Inventory LIFO (c) Periodic $2,100 $1,940 Perpetual $2,100 $2,017 FIFO yields the same ending inventory value under both the periodic and perpetual inventory system. LIFO usually yields different ending inventory values when using the periodic versus perpetual inventory system. *EXERCISE 6-18 (a) Sales ...................................................................... Cost of goods sold Inventory, November 1 ................................ Cost of goods purchased ........................... Cost of goods available for sale ................ Inventory, December 31 .............................. Cost of goods sold ............................. Gross profit ........................................................... $840,000 $130,000 536,000 666,000 120,000 546,000 $294,000 Gross profit rate $294,000/$840,000 = 35% 6-28 Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) *EXERCISE 6-18 (Continued) (b) Sales ........................................................................................ $1,000,000 Less: Estimated gross profit (35% X $1,000,000) ............... 350,000 Estimated cost of goods sold ................................................ $ 650,000 Beginning inventory ............................................................... Cost of goods purchased ...................................................... Cost of goods available for sale ............................................ Less: Estimated cost of goods sold .................................... Estimated cost of ending inventory ...................................... $120,000 610,000 730,000 650,000 $ 80,000 *EXERCISE 6-19 (a) Net sales ($51,000 – $1,000) ................................................... Less: Estimated gross profit (40% X $50,000) .................... Estimated cost of goods sold ................................................ $50,000 20,000 $30,000 Beginning inventory ............................................................... Cost of goods purchased ($31,200 – $1,400 + $1,200) ........ Cost of goods available for sale ............................................ Less: Estimated cost of goods sold .................................... Estimated cost of merchandise lost ..................................... $20,000 31,000 51,000 30,000 $21,000 (b) Net sales .................................................................................. Less: Estimated gross profit (30% X $50,000) .................... Estimated cost of goods sold ................................................ $50,000 15,000 $35,000 Beginning inventory ............................................................... Cost of goods purchased ...................................................... Cost of goods available for sale ............................................ Less: Estimated cost of goods sold .................................... Estimated cost of merchandise lost ..................................... $30,000 31,000 61,000 35,000 $26,000 Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) 6-29 *EXERCISE 6-20 Women’s Shoes Cost Retail Beginning inventory Goods purchased Goods available for sale Net sales Ending inventory at retail Cost-to-retail ratio $ 25,000 110,000 $135,000 $ 46,000 179,000 225,000 178,000 $ 47,000 $135,000 = 60% $225,000 Estimated cost of ending inventory $47,000 X 60% = $28,200 6-30 Copyright © 2013 John Wiley & Sons, Inc. Men’s Shoes Cost Retail $ 45,000 136,300 $181,300 $ 60,000 185,000 245,000 185,000 $ 60,000 $181,300 = 74% $245,000 $60,000 X 74% = $44,400 Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) PROBLEM 6-1A (a) The sale will be recorded on February 26. The goods (cost, $800) should be excluded from Austin’s February 28 inventory. (b) Austin owns the goods once they are shipped on February 26. Include inventory of $480. (c) Include $650 in inventory. (d) Exclude the items from Austin’s inventory. Title remains with the consignor. (e) Title of the goods does not transfer to Austin until March 2. Exclude this amount from the February 28 inventory. (f) Title to the goods does not transfer to the customer until March 2. The $200 cost should be included in ending inventory. Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) 6-31 PROBLEM 6-2A (a) Date Oct. 1 3 9 19 25 COST OF GOODS AVAILABLE FOR SALE Explanation Units Unit Cost Beginning Inventory 2,000 $7 Purchase 2,500 8 Purchase 3,500 9 Purchase 3,000 10 11 Purchase 4,000 Total 15,000 (b) Total Cost $ 14,000 20,000 31,500 30,000 44,000 $139,500 FIFO Ending Inventory Unit Date Units Cost Oct. 25 4,000 $11 19 100 10 4,100* (1) Total Cost $44,000 1,000 $45,000 (2) Cost of Goods Sold Cost of goods available for sale $139,500 Less: Ending inventory 45,000 Cost of goods sold $ 94,500 *15,000 – 10,900 = 4,100 Date Oct. 1 3 9 19 Proof of Cost of Goods Sold Units Unit Cost Total Cost 2,000 $7 $14,000 2,500 8 20,000 3,500 9 31,500 10 29,000 2,900 10,900 $94,500 LIFO (1) Ending Inventory Unit Date Units Cost Oct. 1 2,000 $7 3 2,100 8 4,100 6-32 Copyright © 2013 John Wiley & Sons, Inc. Total Cost $14,000 16,800 $30,800 (2) Cost of Goods Sold Cost of goods available for sale $139,500 Less: Ending inventory 30,800 Cost of goods sold $108,700 Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) PROBLEM 6-2A (Continued) Proof of Cost of Goods Sold Unit Total Date Units Cost Cost Oct. 25 4,000 $11 $ 44,000 19 3,000 10 30,000 9 3,500 9 31,500 3 400 8 3,200 10,900 $108,700 AVERAGE COST (1) Ending Inventory (2) Cost of Goods Sold $139,500 ÷ 15,000 = $9.30 Cost of goods available for sale $139,500 Units Unit Cost Total Cost Less: Ending inventory 38,130 4,100 $9.30 $38,130 Cost of goods sold $101,370 (c) (1) FIFO results in the highest inventory amount for the balance sheet, $45,000. (2) LIFO results in the highest cost of goods sold, $108,700. Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) 6-33 PROBLEM 6-3A (a) Date 1/1 3/15 7/20 9/4 12/2 COST OF GOODS AVAILABLE FOR SALE Explanation Units Unit Cost Beginning Inventory 150 $20 Purchase 400 23 Purchase 250 24 Purchase 350 26 29 Purchase 100 Total 1,250 (b) Total Cost $ 3,000 9,200 6,000 9,100 2,900 $30,200 FIFO (1) Date 12/2 9/4 Ending Inventory Unit Units Cost 100 $29 150 26 250 Total Cost $2,900 3,900 $6,800 (2) Cost of Goods Sold Cost of goods available for sale $30,200 Less: Ending inventory 6,800 Cost of goods sold $23,400 Proof of Cost of Goods Sold Unit Total Date Units Cost Cost 1/1 150 $20 $ 3,000 3/15 400 23 9,200 7/20 250 24 6,000 26 5,200 9/4 200 1,000 $23,400 LIFO (1) Date 1/1 3/15 6-34 Ending Inventory Unit Units Cost 150 $20 100 23 250 Copyright © 2013 John Wiley & Sons, Inc. Total Cost $3,000 2,300 $5,300 (2) Cost of Goods Sold Cost of goods available for sale $30,200 Less: Ending inventory 5,300 Cost of goods sold $24,900 Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) PROBLEM 6-3A (Continued) Proof of Cost of Goods Sold Unit Total Date Units Cost Cost 12/2 100 $29 $ 2,900 9/4 350 26 9,100 7/20 250 24 6,000 3/15 300 23 6,900 1,000 $24,900 AVERAGE COST Ending Inventory (2) Cost of Goods Sold (1) $30,200 ÷ 1,250 = $24.16 Cost of goods available for sale $30,200 Units Unit Cost 6,040 Total Cost Less: Ending inventory 250 $24.16 $6,040 Cost of goods sold $24,160 Proof of Cost of Goods Sold 1,000 units X $24.16 = $24,160 (c) (1) FIFO results in the highest inventory amount, $6,800, as shown in (b) above. (2) LIFO produces the highest cost of goods sold, $24,900 as shown in (b) above. Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) 6-35 PROBLEM 6-4A (a) Felipe INC. Condensed Income Statements For the Year Ended December 31, 2014 Sales revenue ........................................... Cost of goods sold Beginning inventory .......................... Cost of goods purchased ................. Cost of goods available for sale ...... Ending inventory ............................... Cost of goods sold ............................ Gross profit............................................... Operating expenses ................................. Income before income taxes ................... Income tax expense (40%) ...................... Net income ................................................ FIFO LIFO $747,000 $747,000 14,000 466,000 480,000 a 45,900 434,100 312,900 130,000 182,900 73,160 $109,740 14,000 466,000 480,000 b 36,000 444,000 303,000 130,000 173,000 69,200 $103,800 a 17,000 X $2.70 = $45,900. $14,000 + (10,000 X $2.20) = $36,000. b (b) (1) The FIFO method produces the most meaningful inventory amount for the balance sheet because the units are costed at the most recent purchase prices. (2) The LIFO method produces the most meaningful net income because the cost of the most recent purchases are matched against sales. (3) The FIFO method is most likely to approximate actual physical flow because the oldest goods are usually sold first to minimize spoilage and obsolescence. (4) There will be $3,960 additional cash available under LIFO because income taxes are $69,200 under LIFO and $73,160 under FIFO. (5) Gross profit under the average cost method will be: (a) lower than FIFO and (b) higher than LIFO. 6-36 Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) PROBLEM 6-5A (a) Cost of Goods Available for Sale Date Explanation June 1 Beginning Inventory June 4 Purchase June 18 Purchase June 18 Purchase return June 28 Purchase Total Ending Inventory in Units: Units available for sale Sales (110 – 15 + 65) Units remaining in ending inventory 250 160 90 Units 40 135 55 (10) 30 250 Date June 10 11 25 Unit Cost $40 44 46 46 50 Total Cost $ 1,600 5,940 2,530 (460) 1,500 $11,110 Sales Revenue Unit Units Price Total Sales 110 $70 $ 7,700 (15) 70 (1,050) 65 75 4,875 160 $11,525 (1) LIFO (i) Ending Inventory June 1 40 @ $40 4 50 @ 44 90 (iii) Gross Profit Sales revenue Cost of goods sold Gross profit Copyright © 2013 John Wiley & Sons, Inc. $1,600 2,200 $3,800 $11,525 7,310 $ 4,215 (ii) Cost of Goods Sold Cost of goods available for sale Less: Ending inventory Cost of goods sold $11,110 3,800 $ 7,310 (iv) Gross Profit Rate Gross profit $ 4,215 = 36.6% Net sales $11,525 Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) 6-37 PROBLEM 6-5A (Continued) (2) FIFO (i) Ending Inventory June 28 30 @ $50 18 45 @ $46 4 15 @ $44 90 (iii) Gross Profit Sales revenue Cost of goods sold Gross profit $1,500 2,070 660 $4,230 $11,525 6,880 $ 4,645 (ii) Cost of Goods Sold Cost of goods available for sale Less: Ending inventory Cost of goods sold $11,110 4,230 $ 6,880 (iv) Gross Profit Rate Gross profit $ 4,645 = 40.3% Net sales $11,525 (3) Average-Cost Weighted-average cost per unit: Cost of goods available for sale Units available for sale $11,110 = $44.44 250 (i) Ending Inventory 90 units @$44.44 (iii) Gross Profit Sales revenue Cost of goods sold Gross profit 3,999.60 $11,525.00 7,110.40 $ 4,414.60 (ii) Cost of Goods Sold Cost of goods available for sale Less: Ending inventory Cost of goods sold $11,110.00 3,999.60 $ 7,110.40 (iv) Gross Profit Rate Gross profit $ 4,414.60 = 38.3% Net sales $11,525.00 (b) In this period of rising prices, LIFO gives the highest cost of goods sold and the lowest gross profit. FIFO gives the lowest cost of goods sold and the highest gross profit. 6-38 Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) PROBLEM 6-6A (a) BARTON INC. Income Statement (partial) For the Year Ended December 31, 2014 a Sales revenue Beginning inventory Purchasesb Cost of goods available for sale Ending inventoryc Cost of goods sold Gross profit Specific Identification $8,915 1,200 6,505 7,705 2,505 5,200 $3,715 FIFO $8,915 1,200 6,505 LIFO $8,915 1,200 6,505 7,705 2,720 4,985 $3,930 7,705 2,175 5,530 $3,385 (a) (2,300 @ $1.05) + (5,200 @ $1.25) (2,500 @ $ .65) + (4,000 @ $.72) + (2,500 @ $.80) (c) Specific identification ending inventory consists of: (b) 550 @ $.60 Beginning inventory (2,000 liters – 1,000 – 450) March 3 purchase (2,500 liters – 1,300 – 550) 650 @ $.65 March 10 purchase (4,000 liters – 2,900) 1,100 @ $.72 March 20 purchase (2,500 liters – 1,300) 1,200 @ $.80 3,500 liters $ 330.00 422.50 792.00 960.00 $2,504.50 FIFO ending inventory consists of: March 20 purchase March 10 purchase 2,500 @ $.80 1,000 @ $.72 3,500 liters $2,000 720 $2,720 2,000 @ $.60 1,500 @ $.65 3,500 liters $1,200 975 $2,175 LIFO ending inventory consists of: Beginning inventory March 3 purchase (b) Companies can choose a cost flow method that produces the highest possible cost of goods sold and lowest gross profit to justify price increases. In this example, LIFO produces the lowest gross profit and best support to increase selling prices. Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) 6-39 PROBLEM 6-7A (a) Sherlynn CO. Condensed Income Statement For the Year Ended December 31, 2014 Sales revenue ............................................. Cost of goods sold Beginning inventory ........................... Cost of goods purchased .................. Cost of goods available for sale ....... Ending inventory ................................ Cost of goods sold ............................. Gross profit................................................. Operating expenses ................................... Income before income taxes ..................... Income tax expense (30%) ........................ Net income .................................................. FIFO $700,000 LIFO $700,000 45,000 532,000 577,000 a 168,000 409,000 291,000 140,000 151,000 45,300 $105,700 45,000 532,000 577,000 b 147,000 430,000 270,000 140,000 130,000 39,000 $ 91,000 a (30,000 @ $5.60) = $168,000. (10,000 @ $4.50) + (20,000 @ $5.10) = $147,000. b (b) Answers to questions: (1) The FIFO method produces the most meaningful inventory amount for the balance sheet because the units are costed at the most recent purchase prices. (2) The LIFO method produces the most meaningful net income because the costs of the most recent purchases are matched against sales. (3) The FIFO method is most likely to approximate actual physical flow because the oldest goods are usually sold first to minimize spoilage and obsolescence. (4) There will be $6,300 additional cash available under LIFO because income taxes are $39,000 under LIFO and $45,300 under FIFO. (5) The illusionary gross profit is $21,000 or ($291,000 – $270,000). Under LIFO, Sherlynn Co. has recovered the current replacement cost of the units ($430,000), whereas under FIFO, it has only recovered the earlier costs ($409,000). This means that, under FIFO, the company must reinvest at least $21,000 of the gross profit to replace the units used. 6-40 Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) *PROBLEM 6-8A (a) Sales: January 8 January 10 (return) January 20 (1) LIFO Date January 1 January 5 110 (10 90 190 units @ $28 units @ $28) units @ $32 units Purchases $3,080 (280) 2,880 $5,680 Cost of Goods Sold (140 @ $18) $2,520 January 8 (110 @ $18) $1,980 January 10 (–10 @ $18) ($ 180) January 15 January 16 ( 55 @ $20) $1,100 ( –5 @ $20) ($ 100) ( 50 @ $20) ( 40 @ $18) January 20 January 25 } $1,720 ( 20 @ $22) $ 440 $3,520 Balance (100 @ $15) (100 @ $15) (140 @ $18) (100 @ $15) ( 30 @ $18) (100 @ $15) ( 40 @ $18) (100 @ $15) ( 40 @ $18) ( 55 @ $20) (100 @ $15) ( 40 @ $18) ( 50 @ $20) (100 @ $15) $1,500 } $4,020 } $2,040 } $2,220 } } $3,320 $3,220 $1,500 } (100 @ $15) } $1,940 ( 20 @ $22) (i) Cost of goods sold = $3,520. (ii) Ending inventory = $1,940. (iii) Gross profit = $5,680 – $3,520 = $2,160. Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) 6-41 *PROBLEM 6-8A (Continued) (2) FIFO Date Purchases Cost of Goods Sold January 1 January 5 (100 @ $15) (100 @ $15) (140 @ $18) (140 @ $18) $2,520 (100 @ $15) ( 10@ $18) (–10 @ $18) January 8 January 10 January 15 ( 55 @ $20) $1,100 January 16 ( –5 @ $20)($ 100) January 20 January 25 Balance (90 @ $18) } $1,500 } $4,020 $1,680 (130 @ $18) $2,340 ($ 180) (140 @ $18) (140 @ $18) ( 55 @ $20) (140 @ $18) ( 50 @ $20) ( 50 @ $18) ( 50 @ $20) ( 50 @ $18) ( 50 @ $20) ( 20 @ $22) $2,520 $1,620 ( 20 @ $22) $ 440 } } } } $3,620 $3,520 $1,900 $2,340 $3,120 (i) Cost of goods sold = $3,120. (ii) Ending inventory = $2,340. (iii) Gross profit = $5,680 – $3,120 = $2,560. (3) Moving-Average Cost Date January 1 January 5 January 8 January 10 January 15 January 16 January 20 January 25 Purchases Cost of Goods Sold (140 @ $18) $2,520 (110 @ $16.75) (–10 @ $16.75) $1,843 ($ 168) (90 @ $17.605) $1,584 ( 55 @ $20) $1,100 ( –5 @ $20) ($ 100) ( 20 @ $22) $ 440 Balance (100 @ $15) (240 @ $16.75)a (130 @ $16.75) (140 @ $16.75) (195 @ $17.667)b (190 @ $17.605)c (100 @ $17.605) (120 @ $18.342)d $1,500 $4,020 $2,177 $2,345 $3,445 $3,345 $1,761 $2,201 $3,259 *rounded $4,020 ÷ 240 = $16.75 b $3,445 ÷ 195 = $17.667 a c $3,345 ÷ 190 = $17.61 $2,201 ÷ 120 = $18.342 d (i) Cost of goods sold = $3,259. (ii) Ending inventory = $2,201. (iii) Gross profit = $5,680 – $3,259 = $2,421. 6-42 Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) *PROBLEM 6-8A (Continued) (b) Gross profit: Sales Cost of goods sold Gross profit Ending inventory LIFO $5,680 3,520 $2,160 $1,940 FIFO $5,680 3,120 $2,560 $2,340 Moving-Average Cost $5,680 3,259 $2,421 $2,201 In a period of rising costs, the LIFO cost flow assumption results in the highest cost of goods sold and lowest gross profit. FIFO gives the lowest cost of goods sold and highest gross profit. The moving-average cost flow assumption results in amounts between the other two. On the balance sheet, FIFO gives the highest ending inventory (representing the most current costs); LIFO gives the lowest ending inventory (representing the oldest costs); and moving-average cost results in an ending inventory falling between the other two. Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) 6-43 *PROBLEM 6-9A (a) (1) FIFO Date July 1 6 11 Purchases (5 @ $120) Cost of Goods Sold $ 600 (4 @ $120) (7 @ $136) $480 $ 952 (1 @ $120) (2 @ $136) 14 21 Balance (8 @ $147) } $392 $1,176 27 (5 @ $136) (1 @ $147) (2) } $827 (5 @ $120) (1 @ $120) (1 @ $120) (7 @ $136) $ 600 $ 120 } (5 @ $136) (5 @ $136) (8 @ $147) $1,072 $ 680 } (7 @ $147) $1,856 $1,029 MOVING-AVERAGE COST Date July 1 6 11 14 21 27 Purchases (5 @ $120) $ 600 (7 @ $136) $ 952 (8 @ $147) $1,176 Cost of Goods Sold (4 @ $120) $480 (3 @ $134) $402 (6 @ $142) $852 Balance ( 5 @ $120) ( 1 @ $120) ( 8 @ $134)* ( 5 @ $134) (13 @ $142)** ( 7 @ $142) $ 600 $ 120 $1,072 $ 670 $1,846 $ 994 *$1,072 ÷ 8 = $134 **$1,846 ÷ 13 = $142 (3) LIFO Date Purchases July 1 6 11 (5 @ $120) $ 600 (4 @ $120) (7 @ $136) (3 @ $136) (8 @ $147) $480 $ 952 14 21 Cost of Goods Sold $408 $1,176 27 (6 @ $147) $882 Balance (5 @ $120) (1 @ $120) (1 @ $120) (7 @ $136) (1 @ $120) (4 @ $136) (1 @ $120) (4 @ $136) (8 @ $147) (1 @ $120) (4 @ $136) (2 @ $147) $ 600 $ 120 } } } } $1,072 $ 664 $1,840 $ 958 (b) The highest ending inventory is $1,029 under the FIFO method. 6-44 Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) *PROBLEM 6-10A (a) Net sales ....................................................... Cost of goods sold Beginning inventory ............................ Purchases............................................. $389,000 Less: Purchase returns and allowances ................................ 13,300 Purchase discounts ................. 8,500 Add: Freight-in ................................... 8,800 Cost of goods purchased ................... Cost of goods available for sale ......... Ending inventory ................................. Cost of goods sold....................... Gross profit .................................................. Gross profit rate = $228,000 $600,000 November $600,000 $ 32,000 376,000 408,000 36,000 372,000 $228,000 = 38% (b) Net sales................................................. Less: Estimated gross profit (38% X $700,000) ........................ Estimated cost of goods sold ............... Beginning inventory .............................. Purchases............................................... Less: Purchase returns and allowances .................................. $14,900 Purchase discounts ................... 9,500 Net purchases ........................................ Freight-in ................................................ Cost of goods purchased ..................... Cost of goods available for sale ........... Less: Estimated cost of goods sold .............................................. Estimated inventory lost in fire ............ Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual $700,000 266,000 $434,000 $ 36,000 $420,000 24,400 395,600 9,900 405,500 441,500 434,000 $ 7,500 (For Instructor Use Only) 6-45 *PROBLEM 6-11A (a) Hardcovers Cost Beginning inventory Purchases Freight-in Purchase discounts Goods available for sale Net sales Ending inventory at retail $ 420,000 2,135,000 24,000 (44,000) $2,535,000 Retail Paperbacks Cost Retail $ 700,000 $ 280,000 $ 360,000 3,200,000 1,155,000 1,540,000 12,000 (22,000) 3,900,000 $1,425,000 1,900,000 3,100,000 1,570,000 $ 800,000 $ 330,000 Cost-to-retail ratio: Hardcovers—$2,535,000 ÷ $3,900,000 = 65%. Paperbacks—$1,425,000 ÷ $1,900,000 = 75%. Estimated ending inventory at cost: $800,000 X 65% = $520,000—Hardcovers. $330,000 X 75% = $247,500—Paperbacks. (b) Hardcovers—$790,000 X 65% = $513,500. Paperbacks—$335,000 X 75% = $251,250. 6-46 Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) SOLUTIONS TO PROBLEMS PROBLEM 6-1B (a) The goods should not be included in inventory as they were shipped FOB shipping point and shipped February 26. Title to the goods transfers to the customer February 26. Weber should have recorded the transaction in the Sales and Accounts Receivable accounts. (b) The amount should not be included in inventory as they were shipped FOB destination and not received until March 2. The seller still owns the inventory. No entry is recorded. (c) Include $500 in inventory. (d) Include $400 in inventory. (e) $750 should be included in inventory as the goods were shipped FOB shipping point. (f) The sale will be recorded on March 2. The goods should be included in inventory at the end of February at their cost of $250. (g) The damaged goods should not be included in inventory. They should be recorded in a loss account since they are not saleable. Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) 6-47 PROBLEM 6-2B (a) Date March 1 5 13 21 26 COST OF GOODS AVAILABLE FOR SALE Explanation Units Unit Cost Beginning Inventory 1,500 $ 7 Purchase 3,000 8 Purchase 4,500 9 Purchase 4,000 10 11 Purchase 2,500 Total 15,500 (b) Total Cost $ 10,500 24,000 40,500 40,000 27,500 $142,500 FIFO Ending Inventory Unit Date Units Cost March 26 2,500 $11 21 1,000 10 3,500* (1) Total Cost $27,500 10,000 $37,500 (2) Cost of Goods Sold Cost of goods available for sale $142,500 Less: Ending inventory 37,500 Cost of goods sold $105,000 *15,500 – 12,000 = 3,500 Proof of Cost of Goods Sold Unit Total Date Units Cost Cost March 1 1,500 $ 7 $ 10,500 5 3,000 8 24,000 13 4,500 9 40,500 21 3,000 10 30,000 12,000 $105,000 6-48 Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) PROBLEM 6-2B (Continued) LIFO Ending Inventory Unit Date Units Cost March 1 1,500 $7 5 2,000 8 3,500 (1) Total Cost $10,500 16,000 $26,500 (2) Cost of Goods Sold Cost of goods available for sale $142,500 Less: Ending inventory 26,500 Cost of goods sold $116,000 Proof of Cost of Goods Sold Unit Total Date Units Cost Cost March 26 2,500 $11 $27,500 21 4,000 10 40,000 13 4,500 9 40,500 5 1,000 8 8,000 12,000 $116,000 AVERAGE-COST Ending Inventory (2) Cost of Goods Sold (1) Cost of goods $142,500 ÷ 15,500 = $9.194 available for sale $142,500 Unit Less: Ending Units Cost Total Cost inventory 32,179 3,500 $9.194 $32,179* Cost of goods sold $110,321 *rounded to nearest dollar (c) (1) As shown in (b) above, FIFO produces the highest inventory amount, $37,500. (2) As shown in (b) above, LIFO produces the highest cost of goods sold, $116,000. Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) 6-49 PROBLEM 6-3B (a) Date 1/1 2/20 5/5 8/12 12/8 COST OF GOODS AVAILABLE FOR SALE Explanation Units Unit Cost Beginning Inventory 400 $ 8 Purchase 600 9 Purchase 500 10 Purchase 300 11 12 Purchase 200 Total 2,000 (b) Total Cost $ 3,200 5,400 5,000 3,300 2,400 $19,300 FIFO (1) Date 12/8 8/12 Ending Inventory Unit Units Cost 200 $12 300 11 500 Total Cost $2,400 3,300 $5,700 (2) Cost of Goods Sold Cost of goods available for sale $19,300 Less: Ending inventory 5,700 Cost of goods sold $13,600 Proof of Cost of Goods Sold Unit Total Date Units Cost Cost 1/1 400 $ 8 $ 3,200 2/20 600 9 5,400 10 5,000 5/5 500 1,500 $13,600 6-50 Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) PROBLEM 6-3B (Continued) (b) LIFO (1) Date 1/1 2/20 Ending Inventory Unit Units Cost 400 $8 100 9 500 Total Cost $3,200 900 $4,100 (2) Cost of Goods Sold Cost of goods available for sale $19,300 Less: Ending inventory 4,100 Cost of goods sold $15,200 Proof of Cost of Goods Sold Unit Total Date Units Cost Cost 12/8 200 $12 $ 2,400 8/12 300 11 3,300 5/5 500 10 5,000 9 4,500 2/20 500 1,500 $15,200 AVERAGE-COST Ending Inventory (2) Cost of Goods Sold (1) Cost of goods $19,300 ÷ 2,000 = $9.65 available for sale $19,300 Unit Less: Ending Total Units Cost inventory 4,825 Cost 500 $9.65 $4,825 Cost of goods sold $14,475 Proof of Cost of Goods Sold 1,500 units X 9.65 = $14,475 (c) (1) LIFO results in the lowest inventory amount for the balance sheet, $4,100. (2) FIFO results in the lowest cost of goods sold, $13,600. Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) 6-51 PROBLEM 6-4B (a) Patel CO. Condensed Income Statement For the Year Ended December 31, 2014 Sales revenue ............................................. Cost of goods sold Beginning inventory ........................... Cost of goods purchased .................. Cost of goods available for sale ....... Ending inventory ................................ Cost of goods sold ............................. Gross profit ................................................. Operating expenses ................................... Income before income taxes ..................... Income tax expense (34%) ........................ Net income .................................................. a 28,000 X $2.80 = $78,400. b FIFO $865,000 32,000 600,000 632,000 a 78,400 553,600 311,400 147,000 164,400 55,896 $108,504 LIFO $865,000 32,000 600,000 632,000 b 63,200 568,800 296,200 147,000 149,200 50,728 $98,472 $32,000 + (13,000 X $2.40) = $63,200. (b) (1) The FIFO method produces the most meaningful inventory amount for the balance sheet because the units are costed at the most recent purchase prices. (2) The LIFO method produces the most meaningful net income because the costs of the most recent purchases are matched against sales. (3) The FIFO method is most likely to approximate actual physical flow because the oldest goods are usually sold first to minimize spoilage and obsolescence. (4) There will be $5,168 additional cash available under LIFO because income taxes are $50,728 under LIFO and $55,896 under FIFO. (5) Gross profit under the average cost method will be: (a) lower than FIFO and (b) higher than LIFO. 6-52 Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) PROBLEM 6-5B Cost of Goods Available for Sale Date Explanation October 1 Beginning Inventory 9 Purchase 17 Purchase 25 Purchase Total Ending Inventory in Units: Units available for sale Sales (100 + 60 + 110) Units remaining in ending inventory Units 60 120 70 80 330 330 270 60 Unit Cost $25 26 27 28 Total Cost $1,500 3,120 1,890 2,240 $8,750 Sales Revenue Unit Date Units Price Total Sales October 11 100 $35 $ 3,500 22 60 40 2,400 29 110 40 4,400 270 $10,300 (a) (1) LIFO (i) Ending Inventory October 1 60 @ $25 = $1,500 (iii) Gross Profit Sales revenue Cost of goods sold Gross profit Copyright © 2013 John Wiley & Sons, Inc. $10,300 7,250 $ 3,050 (ii) Cost of Goods Sold Cost of goods available for sale Less: Ending inventory Cost of goods sold $8,750 1,500 $7,250 (iv) Gross Profit Rate Gross profit $ 3,050 = 29.6% Net sales $10,300 Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) 6-53 PROBLEM 6-5B (Continued) (2) FIFO (ii) Cost of Goods Sold Cost of goods available for sale Less: Ending inventory Cost of goods sold (i) Ending Inventory October 25 60 @ $28 = $1,680 (iii) Gross Profit Sales revenue Cost of goods sold Gross profit $10,300 7,070 $ 3,230 $ 8,750 1,680 $ 7,070 (iv) Gross Profit Rate Gross profit $ 3,230 = 31.4% Net sales $10,300 (3) Average-Cost Weighted-average cost per unit: cost of goods available for sale units available for sale $8,750 330 (i) Ending Inventory 60 @ $26.515 = $1,591* *rounded to nearest dollar (iii) Gross Profit Sales revenue Cost of goods sold Gross profit $10,300 7,159 $ 3,141 = $26.515 (ii) Cost of Goods Sold Cost of goods available for sale Less: Ending inventory Cost of goods sold $8,750 1,591 $7,159 (iv) Gross Profit Rate Gross profit $ 3,141 = 30.5% Net sales $10,300 (b) LIFO produces the lowest ending inventory value, gross profit, and gross profit rate because its cost of goods sold is higher than FIFO or average-cost. 6-54 Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) PROBLEM 6-6B (a) (1) To maximize gross profit, Princess Diamonds should sell the diamonds with the lowest cost. Sale Date March 5 March 25 Cost of Goods Sold 150 @ $300 $ 45,000 30 @ $360 10,800 170 @ $360 61,200 230 @ $380 87,400 580 $204,400 Sales Revenue 180 @ $600 $108,000 400 @ $650 260,000 580 $368,000 Gross profit $368,000 – $204,400 = $163,600. (2) To minimize gross profit, Princess Diamonds should sell the diamonds with the highest cost. Sale Date March 5 March 25 Cost of Goods Sold 180 @ $360 $ 64,800 350 @ $380 133,000 20 @ $360 7,200 30 @ $300 9,000 580 $214,000 Sales Revenue 180 @ $600 $108,000 400 @ $650 260,000 580 $368,000 Gross profit $368,000 – $214,000 = $154,000. (b) FIFO Cost of goods available for sale March 1 Beginning inventory 3 Purchase 10 Purchase Goods available for sale Units sold Ending inventory Copyright © 2013 John Wiley & Sons, Inc. 150 @ $300 200 @ $360 350 @ $380 700 $ 45,000 72,000 133,000 $250,000 700 580 120 @ $380 $45,600 Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) 6-55 PROBLEM 6-6B (Continued) Goods available for sale – Ending inventory Cost of goods sold $250,000 45,600 $204,400 Gross profit: $368,000 – $204,400 = $163,600. (c) LIFO Cost of goods available for sale (from part b) – Ending inventory 120 @ $300 Cost of goods sold $250,000 36,000 $214,000 Gross profit: $368,000 – $214,000 = $154,000. (d) The choice of inventory method depends on the company’s objectives. Since the diamonds are marked and coded, the company could use specific identification. This could, however, result in “earnings management” by the company because, as shown, it could carefully choose which diamonds to sell to result in the maximum or minimum income. Employing a cost flow assumption, such as LIFO or FIFO, would reduce record-keeping costs. FIFO would result in higher income, but LIFO would reduce income taxes and provide better matching of current sales revenue with current costs. 6-56 Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) PROBLEM 6-7B (a) Chelsea INC. Condensed Income Statement For the Year Ended December 31, 2014 FIFO Sales revenue............................................. Cost of goods sold Beginning inventory ........................... Cost of goods purchased ................... Cost of goods available for sale ........ Ending inventory ................................. Cost of goods sold .............................. Gross profit ................................................ Operating expenses .................................. Income before income taxes .................... Income tax expense (28%) ........................ Net income ................................................. LIFO $665,000 $665,000 35,000 504,500 539,500 a 133,500 406,000 259,000 130,000 129,000 36,120 $ 92,880 35,000 504,500 539,500 b 115,000 424,500 240,500 130,000 110,500 30,940 $ 79,560 a (25,000 @ $4.50) + ( 5,000 @ $4.20) = $133,500. (10,000 @ $3.50) + (20,000 @ $4.00) = $115,000. b (b) Answers to questions: (1) The FIFO method produces the most meaningful inventory amount for the balance sheet because the units are costed at the most recent purchase prices. (2) The LIFO method produces the most meaningful net income because the costs of the most recent purchases are matched against sales. (3) The FIFO method is most likely to approximate actual physical flow because the oldest goods are usually sold first to minimize spoilage and obsolescence. (4) There will be $5,180 additional cash available under LIFO because income taxes are $30,940 under LIFO and $36,120 under FIFO. Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) 6-57 PROBLEM 6-7B (Continued) (5) The illusionary gross profit is $18,500 or ($259,000 – $240,500). Under LIFO, Chelsea Inc. has recovered the current replacement cost of the units ($424,500), whereas under FIFO, it has only recovered the earlier costs ($406,000). This means that under FIFO the company must reinvest $18,500 of the gross profit to replace the units used. Answer in business letter form: Dear Chelsea Inc. After preparing the comparative condensed income statements for 2014 under FIFO and LIFO methods, we have found the following: The FIFO method produces the most meaningful inventory amount for the balance sheet because the units are costed at the most recent purchase prices. This method is most likely to approximate actual physical flow because the oldest goods are usually sold first to minimize spoilage and obsolescence. The LIFO method produces the most meaningful net income because the costs of the most recent purchases are matched against sales. There will be $5,180 additional cash available under LIFO because income taxes are $30,940 under LIFO and $36,120 under FIFO. There exists an illusionary gross profit of $18,500 ($259,000 – $240,500) under FIFO. Under LIFO, you have recovered the current replacement cost of the units ($424,500) whereas under FIFO you have only recovered the earlier costs ($406,000). This means that under FIFO, the company must reinvest $18,500 of the gross profit to replace the units sold. Sincerely, 6-58 Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) *PROBLEM 6-8B (a) Sales: Date January 6 January 9 (return) January 10 January 30 Total sales (1) LIFO Date 150 (10 60 110 units @ $40 units @ $40) units @ $45 units @ $50 Purchases $ 6,000 (400) 2,700 5,500 $13,800 Cost of Goods Sold January 1 January 2 January 6 (100 @ $21) $2,100 (100 @ $21) ( 50 @ $17) } $2,950 January 9 ( 80 @ $24) $1,920 January 9 January 10 (–10 @ $24) ($ 240) (–10 @ $17) ($ 170) January 10 ( 60 @ $24) $1,440 January 23 (100 @ $28) $2,800 January 30 (100 @ $28) ( 10 @ $24) } $3,040 Balance (160 @ $17) (160 @ $17) (100 @ $21) (110 @ $17) (120 @ $17) ( 80 @ $24) (120 @ $17) ( 70 @ $24) (120 @ $17) ( 10 @ $24) (120 @ $17) ( 10 @ $24) (100 @ $28) (120 @ $17) $2,720 } $4,820 $1,870 } $3,960 } $3,720 } $2,280 } $5,080 $2,040 $7,260 (i) Cost of goods sold: = $7,260. (ii) Ending inventory = $2,040. (iii) Gross profit = $13,800 – $7,260 = $6,540 Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) 6-59 *PROBLEM 6-8B (Continued) (2) FIFO Date Purchases Cost of Goods Sold January 1 January 2 January 6 January 9 January 9 (100 @ $21) $2,100 (150 @ $17) $2,550 (–10 @ $17) ($ 170) ( 80 @ $24) $1,920 January 10 January 10 (–10 @ $24) ($ 240) January 23 (100 @ $28) $2,800 ( 20 @ $17) ( 40 @ $21) January 30 ( 60 @ $21) ( 50 @ $24) } $1,180 } $2,460 Balance (160 @ $17) (160 @ $17) (100 @ $21) ( 10 @ $17) (100 @ $21) ( 20 @ $17) (100 @ $21) ( 80 @ $24) ( 20 @ $17) (100 @ $21) ( 70 @ $24) ( 60 @ $21) ( 70 @ $24) ( 60 @ $21) ( 70 @ $24) (100 @ $28) ( 20 @ $24) (100 @ $28) $2,720 } } } } $4,820 $2,270 $4,360 $4,120 } $2,940 } $5,740 } $3,280 $6,020 (i) Cost of goods sold = $6,020. (ii) Ending inventory = $3,280. (iii) Gross profit = $13,800 – $6,020 = $7,780. (3) Moving-Average Date January 1 January 2 January 6 January 9 January 9 January 10 January 10 January 23 January 30 Purchases Cost of goods sold (100 @ $21) $2,100 (150 @ $18.538) $2,781 (–10 @ $18.538) ($ 185) ( 80 @ $24) $1,920 (–10 @ $24) ($ 240) ( 60 @ $20.547) $1,233 (100 @ $28) $2,800 (110 @ $23.787) $2,617 $6,446 a c b d $4,820 ÷ 260 = $18.538 $4,144 ÷ 200 = $20.72 Balance (160 @ $17) (260 @ $18.538)a (110 @ $18.538) (120 @ $18.538) (200 @ $20.72) b (190 @ $20.547) c (130 @ $20.547) (230 @ $23.787) d (120 @ $23.787) $2,720 $4,820 $2,039 $2,224 $4,144 $3,904 $2,671 $5,471 $2,854 $3,904 ÷ 190 = $20.547 $5,471 ÷ 230 = $23.787 (i) Cost of goods sold = $6,446. (ii) Ending inventory = $2,854. (iii) Gross profit = $13,800 – $6,446 = $7,354. 6-60 Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) *PROBLEM 6-8B (Continued) (b) Gross profit: Sales Cost of goods sold Gross profit Ending inventory LIFO $13,800 7,260 $ 6,540 $ 2,040 FIFO $13,800 6,020 $ 7,780 $ 3,280 Moving-Average $13,800 6,446 $ 7,354 $ 2,854 In a period of rising costs, the LIFO cost flow assumption results in the highest cost of goods sold and lowest gross profit. FIFO gives the lowest cost of goods sold and highest gross profit. The moving average cost flow assumption results in amounts between the other two. On the balance sheet, FIFO gives the highest ending inventory (representing the most current costs); LIFO gives the lowest ending inventory (representing the oldest costs); and the moving average-cost results in an ending inventory falling between the other two. Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) 6-61 *PROBLEM 6-9B (a) (1) FIFO Date May 1 4 8 Cost of Goods Sold Purchases (7 @ $150) $1,050 (4 @ $150) (8 @ $170) (3 @ $150) (2 @ $170) (6 @ $185) $600 $1,360 12 15 Balance } $790 $1,110 20 (3 @ $170) $510 25 (3 @ $170) (1 @ $185) } $695 (2) (7 @ $150) (3 @ $150) (3 @ $150) (8 @ $170) $1,050 $ 450 } $1,810 (6 @ $170) (6 @ $170) (6 @ $185) (3 @ $170) (6 @ $185) $1,020 } $2,130 } $1,620 (5 @ $185) $ 925 MOVING-AVERAGE COST Date May 1 4 8 12 15 20 25 Purchases (7 @ $150) (8 @ $170) (6 @ $185) Cost of Goods Sold Balance $1,050 (4 @ $150) $600 (5 @ $164.55) $823 (3 @ $174.75) (4 @ $174.75) $524 $699 $1,360 $1,110 ( 7 @ $150) ( 3 @ $150) (11 @ $164.55)* ( 6 @ $164.55) (12 @ $174.75)** ( 9 @ $174.75) ( 5 @ $174.75) $1,050 $ 450 $1,810 $ 987 $2,097 $1,573 $ 874 *Average-cost = $1,810 ÷ 11 (rounded) **$2,097 ÷ 12 6-62 Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) *PROBLEM 6-9B (Continued) (3) LIFO Date May 1 4 8 Purchases (7 @ $150) $1,050 (4 @ $150) (8 @ $170) (5 @ $170) (6 @ $185) $600 $1,360 12 15 Cost of Goods Sold $850 $1,110 20 (3 @ $185) $555 25 (3 @ $185) (1 @ $170) } $725 Balance (7 @ $150) (3 @ $150) (3 @ $150) (8 @ $170) (3 @ $150) (3 @ $170) (3 @ $150) (3 @ $170) (6 @ $185) (3 @ $150) (3 @ $170) (3 @ $185) (3 @ $150) (2 @ $170) $1,050 $ 450 } } } } } $1,810 $ 960 $2,070 $1,515 $ 790 (b) (1) The highest ending inventory is $925 under the FIFO method. (2) The lowest ending inventory is $790 under the LIFO method. Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) 6-63 *PROBLEM 6-10B (a) February $300,000 Net sales .................................................. Cost of goods sold Beginning inventory ....................... $ 4,500 Net purchases ................................. $176,800 Add: Freight-in ............................... 3,900 Cost of goods purchased .............. 180,700 Cost of goods available for sale .... 185,200 Ending inventory ............................ 20,200 Cost of goods sold .................. 165,000 Gross profit .............................................. $135,000 Gross profit rate = $135,000 = 45% $300,000 (b) Net sales .............................................................. Less: Estimated gross profit (45% X $250,000) ...................................... Estimated cost of goods sold ............................ Beginning inventory............................................ Net purchases ..................................................... Add: Freight-in ................................................... Cost of goods purchased ................................... Cost of goods available for sale ........................ Less: Estimated cost of goods sold ................. Estimated total cost of ending inventory .......................................................... Less: Inventory not lost (30% X $24,700) ............................................... Estimated inventory lost in fire (70% X $24,700) .............................................. 6-64 Copyright © 2013 John Wiley & Sons, Inc. $250,000 112,500 $137,500 $ 20,200 $139,000 3,000 Weygandt, Accounting Principles, 11/e, Solutions Manual 142,000 162,200 137,500 24,700 7,410 $ 17,290 (For Instructor Use Only) *PROBLEM 6-11B (a) Sporting Goods Cost Beginning inventory Purchases Purchase returns Purchase discounts Freight-in Goods available for sale Net sales Ending inventory at retail Jewelry and Cosmetics Retail $ 47,360 $ 74,000 675,000 1,066,000 (26,000) (40,000) (12,360) 9,000 $693,000 1,100,000 (1,000,000) $ 100,000 Cost Retail $ 39,440 $ 62,000 741,000 1,158,000 (12,000) (20,000) (2,440) 14,000 $780,000 1,200,000 (1,160,000) $ 40,000 Cost-to-retail ratio: Sporting Goods—$693,000 ÷ $1,100,000 = 63%. Jewelry and Cosmetics—$780,000 ÷ $1,200,000 = 65%. Estimated ending inventory at cost: $100,000 X 63% = $63,000—Sporting Goods. $ 40,000 X 65% = $26,000—Jewelry and Cosmetics. (b) Sporting Goods—$95,000 X 60% = $57,000. Jewelry and Cosmetics—$44,000 X 64% = $28,160. Copyright © 2013 John Wiley & Sons, Inc. Weygandt, Accounting Principles, 11/e, Solutions Manual (For Instructor Use Only) 6-65