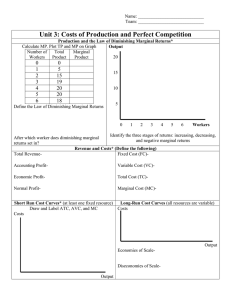

Law of demand Demand function Demand concepts Demand curve (graph of inverse demand function) Elastic, Unit-elastic, and Inelastic Elasticity Perfectly elastic and inelastic Elasticity and total expenditure on a good Price elasticity of demand Own-price Larger for goods with close substitutes, occupy a large portion of the budget, are seen as discretionary, or have longer time to adjust to changes in its price. Cross-price Income Substitution and income effects Law of diminishing marginal returns Supply analysis : cost, marginal returns, and productivity Total cost: TC = wL + rK w = hourly wage; L = labor hours; r = rental rate of capital; K = capital hours Total, average, and marginal product of labor Economic profit = Total revenue (TR) - Economic cost (total cost (TC)) Accounting profit = TR - Accounting cost Economic vs Accounting Economic depreciation: What am I giving up if I use my resources to produce output in the coming period? Accounting depreciation: How should I distribute the historical cost—that I have already paid—across units of output that I intend to produce this period? Marginal revenue (MR) and marginal cost (MC) Demand & Supply Cooperative vs Non-cooperative countries Total, Variable, Fixed, and Marginal Costs Landlocked countries rely on neighbors for access to vital resources => cooperation more important. National security or military S, the lowest point on the AVC curve, is where MC = AVC. Beyond quantity QAVC, MC > AVC; thus, the AVC curve begins to rise. T, the lowest point on the ATC curve, is where MC = ATC. Beyond quantity QATC, MC > ATC; thus, the ATC curve is rising. A, the difference between ATC and AVC at output quantity Q1, is exactly the AFC. R is the lowest point on the MC curve. Beyond this point of production, fixed input constraints reduce labor productivity. X is the difference between ATC and AVC at Q2. X < A because AFC (Y) falls with output. Countries highly connected to trade routes or acting as a conduit for trade use their geographic location as a lever of power in broader international dynamics. Domestically, growing national wealth and limiting income inequality contribute to social stability, an important component of national security. Economy Internationally, countries that cooperates in support of their economic interest are focused on 1 of 2 factors: (1) securing essential resources through trade, or (2) leveling the global playing field for their companies/industries through standardization. Motivations for cooperation Livable geography and climate, access to food and water, etc. Highly unequal among countries. Perfect and imperfect competition Geophysical Resource Endowment More endowed with a resource => more political leverage when dealing with another in need of that resource. Resource-rich => use or sale of the resource benefits certain groups more than others => internal political instability. Resource Endowment, Standardization, and Soft Power Regulatory cooperation: Basel Committee on Banking Supervision (BCBS): more effective supervision of the global banking sector and international capital flows. State actors (national governments) & Political cooperation Standardization Perfectly competitive firm Process standardization: Society for Worldwide Interbank Financial Telecommunication (SWIFT): global payment infrastructure. Profit-Maximization, Breakeven, and Shutdown Points of Production Monopolist firm Operational synchronization: Containerization: reduces time and cost of shipping. Historical or modern Cultural Considerations and “Soft Power” Cultural programs, advertisement, travel grants, and university exchanges, etc. Generally, strong institutions => more stable internal and external political forces => more opportunity to develop cooperative relationships. The Role of Institutions Countries with strong institutions => more authority and independence in the international space. Increasing returns to scale. Specialization in one task rather than perform many duties. More efficient equipment, and adaptation the latest in technology. Marketable byproducts, less energy consumption, and enhanced quality control. Better use of market information for more effective decision making. Obtaining discounted prices on resources when buying in bulk. Breakeven: P = MR = SMC = ATC Shutdown: SMC = AVC Decreasing returns to scale. Being so large that it cannot be properly managed. Overlapping and duplication of business functions and product lines. Higher resource prices because of supply constraints when buying inputs in bulk. Stronger institutions => more durable cooperative relationships. Economies of scale Every country has different resources, goals, and leadership => different priorities. Economies and Diseconomies of scale Priorities may shift as political leadership turns over or as global events change. Hierarchy of Interests and Costs of Cooperation Some elements on the hierarchy of national interests may be universally clear-cut. However, as basic societal needs are met, the hierarchy of national interests can become more subjective. Power of the Decision Maker Diseconomies of scale The length of a country’s political cycle has an important impact on priority designation. Political Non-Cooperation Features of globalization Raising sales Raising profits Reducing costs (lower tax-operating environments, reduce labor costs, or seek other supply chain efficiency gains) Motivations for globalization Portfolio investment flows Non-state actors & Forces of globalization Marginal revenue (MR) and marginal cost (MC) Access to resources and markets FDI Intrinsic gain (personal growth and education, improved productivity, higher standards) Unequal Accrual of Economic and Financial Gains Lower Environmental, Social, and Governance Standards Political Consequences (income/wealth inequality, differences in opportunity Costs of globalization Interdependence (if there is a disruption to the supply chain, firms may not be able to produce the good themselves) Reshoring essentials How firms fortify their supply chains Re-globalizing production Perfect competition Doubling down on key markets Monopolistic competition 4 market structures Autarky Self-sufficiency, sometimes swifter economic and political development, but gradual loss of economic and political development within the country Oligopoly Monopoly Assessing geopolitical actors and risks Hegemony Regional or global leaders, influence on global affairs, but may become more competitive and increase geopolitical risk when gaining or losing influence Geopolitics Number and relative size of firms Degree of product differentiation Multilateralism Both capable of and highly dependent on international cooperation for economic growth. Pricing power Regionalism In between the two extremes of bilateralism and multilateralism. In regionalism, a group of countries cooperate with one another. Both bilateralism and regionalism can be conducted at the exclusion of other groups. Determinants of market structure Bilateralism One-at-a-time agreements without multiple partners. Analysis of market structures Barrier to entry and exit National security tools Degree of non-price competition Cooperative: trade agreements, WTO, common markets/currency Economics 1 Threat of entry Economic tools Non-cooperative: nationalization, voluntary export restraints, domestic content requirements Power of suppliers Power of buyers Porter's 5 forces Tools of geopolitics Financial tools Threat of substitutes Cooperative: currency exchange Reduce geopolitical risk if they encourage cooperation in security, economic, or financial arenas. May cause vulnerabilities (e.g., global use of the USD) Non-cooperative: limiting access to local currency markets, restricting foreign investments, sanctions Rivalry among existing competitors Q = a - bP Multi-tool approaches Perfect competition Cabotage: the right to transport passengers or goods within a country by a foreign firm MR = ΔTR/ΔQ Geopolitical Risk and Comparative Advantage A consistent threat of conflict may drive more regular volatility in asset prices. Countries/regions with limited geopolitical risk may attract more labor and capital. Not every country will be endowed with the same factors and capabilities => benefit from trade => more variety of products, higher competition between firms, and more efficient resource allocation. Own-price Substitutes => (+) Cross-price Complements => (-) Event risk: evolves around set dates, such as elections, new legislation, or other date-driven milestones, such as holidays or political anniversaries, known in advance. Income Elasticity of demand Horizontal demand schedule (perfectly elastic) Types of geopolitical risk Extremes Exogeneous risk: sudden or unanticipated risk that impacts either a country’s cooperative stance, the ability of non-state actors to globalize, or both. Vertical demand schedule (perfectly inelastic) Thematic risk: known risks that evolve and expand over a period of time (climate change, pattern migration, the rise of populist forces, threat of terrorism, and cyver threats) Price elasticity will be higher if there are many close substitutes for the product. Determinants The greater the share of the consumer’s budget spent on the item, the higher the price elasticity of demand. Black swan risk: An event that is rare and difficult to predict but has an important impact. The length of time within which the demand schedule is being considered. Likelihood (how likely the risk is to happen) Long term: Impact investors' asset allocation. May have important environmental, social, governance, and other impacts. Immediate impact on portfolios is likely to be more limited. TR, MR and price elasticity Incorporating geopolitical risk into investment Assessing Geopolitical Threats The difference between the value that a consumer places on units purchased and the amount of money that was required to pay for them. Velocity (how quickly the risk impacts investment portfolios) Time horizon Consumer surplus Medium term: Impair companies’ processes, costs, and investment opportunities, resulting in lower valuations. Impact some more than others. Short term: Volatility in the markets may affect entire industries or even the entire market. Long-term changes are unnecessary. Economic costs = Total accounting costs - Implicit opportunity costs P = AR = MR Optimal price and output in perfect competition Supply analysis, optimal price, and output in perfectly competitive markets Low => adjust asset allocation Law of diminishing returns => Profit maximization at output level where MR = MC Quickness Medium => adjust investments in specific sectors Only perfect competition has a defined supply function. Profit maximization at output level where MR = MC High => flight to quality (the herd-like behavior of investors to shift out of risky assets during financial downturns or bear markets) Firm and market structures Impact The long-run marginal cost schedule is the perfectly competitive firm’s supply curve. Long-run equilibrium in perfect competition The firm’s demand curve is dictated by the aggregate market’s equilibrium price. Scenario analysis: evaluating portfolio outcomes across potential circumstances or states of the world. The long-run competitive equilibrium occurs where MC = AC = P Groupthink: thinking or making decisions as a group in a way that discourages creativity or individual responsibility. For scenario analysis to be useful in portfolio management, teams must build creative processes, identify scenarios, track these scenarios, and assess the need for action on a regular cadence. Tracking risks according to signposts Short-run profit maximization at output level where MR = MC There is no well-defined supply function. The information used to determine the appropriate level of output is based on the intersection of MC and MR. However, the price that will be charged is based on the market demand schedule. Acting on Geopolitical Risk Consider objectives, risk tolerance, and time horizon. Monopolistic competition Long-run equilibrium in monopolistic competition: MR = MC High levels of geopolitical risk reduce investment, employment, and price level of the stock market. Observations from the Geopolitical Risk Index (GPR) Firms reduce investment in the wake of idiosyncratic events, which would be unlikely to repeat. The threat of an event was shown to have a larger impact over time than that of the actual events themselves. In a market where collusion is present, the aggregate market demand curve is divided up by the individual production participants. Under non-colluding market conditions, each firm faces an individual demand curve depending on the pricing strategies adopted by the participating firms. 1. If price increases, the competitor ignores it so demand is more responsive (more elastic). 2. If the price falls, the competitor matches it so demand is less responsive (more inelastic). The kink point => current price offered by the market. Assumption in which each firm determines its profit-maximizing production level assuming that the other firms’ output will not change. Cournot assumption The Cournot strategy’s solution can be found by setting Q = q1 + q2, where q1 and q2 represent the output levels of the two firms. Oligopoly and pricing strategies When two or more participants in a non-cooperative game have no incentive to deviate from their respective equilibrium strategies given their opponent’s strategies. The number and size distribution of sellers: number of firms is small or if one firm is dominant. The similarity of the products: products are homogeneous. Nash equilibrium Cost structure: similar the cost structures. Determinants of successful cartel Order size and frequency: orders are frequent, received on a regular basis, and relatively small. The strength and severity of retaliation: low threat. The degree of external competition. Stackelberg model: a prominent model of strategic decision making in which firms are assumed to make their decisions sequentially. Top-dog strategy: the leader aggressively overproduce to force the follower to scale back its production or even punish or eliminate the weaker opponent. The price leader identifies its profit-maximizing output where MRL = MCL, at output QL. No single optimum price and output analysis that fits all oligopoly market situations because of the interdependence. Optimal price, output, and long-run equilibrium in Oligopoly Optimal price is determined at the output level where MR = MC (at kinked point) Long-run economic profits are possible for firms operating in oligopoly markets but over time, the market share of the dominant firm declines. The profit-maximizing level of output occurs where MR = MC. Demand/Supply and Optimal Price/Output First-degree: charge each customer the highest price the customer is willing to pay. Second-degree: charge different per-unit prices using the quantity purchased. Monopoly Price discrimination and consumer surplus Third-degree: segregates customers into groups based on characteristics and offers different pricing to each group. Economic profit is possible. To maintain a monopoly market position in the long run, the firm must be protected by substantial and ongoing barriers to entry, or national ownership of the monopoly. Long-run equilibrium in monopoly The regulator sets price equal to LRAC. Observed price and quantity are the equilibrium values of price and quantity and do not represent the value of either supply or demand. Econometric approaches Identification of market structure Must use a model with 2 equations, an equation of demanded quantity and an equation of supplied quantity. Herfindahl–Hirschman index Concentration ratio Unaffected by mergers among the top market incumbents. Does not directly quantify market power and threat of entrance. Simpler approaches