Uploaded by

Nguyễn Thị Xuân - 2M19

CVP Analysis: Textbook Chapter on Cost-Volume-Profit

advertisement

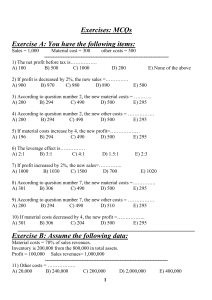

CHAPTER 3: CVP ANALYSIS 1. How can CVP analysis help CVP analysis assists managers in understanding the behavior of managers? a product’s or service’s total costs, total revenues, and operating income as changes occur in the output level, selling price, variable costs, or fixed costs. 2. How determine point or the achieve a income? can managers the breakeven output needed to target operating The breakeven point is the quantity of output at which total revenues equal total costs. The three methods for computing the breakeven point and the quantity of output to achieve target operating income are the equation method, the contribution margin method, and the graph method. Each method is merely a restatement of the others. Managers often select the method they find easiest to use in a specific decision situation. 3. How can managers Income taxes can be incorporated into CVP analysis by using the incorporate income taxes net income to calculate the target operating income. The break into CVP analysis? point is unaffected by income taxes because no income taxes are when operating income equals zero. 4. How do managers use CVP analysis to make decisions? Managers compare how revenues, costs, and contribution margins change across various alternatives. They then choose the alternative that maximizes operating income. 5. What can managers do to cope with uncertainty or changes in underlying assumptions? Sensitivity analysis is a “what-if” technique that examines how an outcome will change if the original predicted data are not achieved or if an underlying assumption changes. When making decisions, managers use CVP analysis to compare contribution margins and fixed costs under different assumptions. Managers also calculate the margin of safety equal to budgeted revenues minus breakeven revenues. 6. How should managers choose among different variable-cost/fixed-cost structures? Choosing the variable-cost/fixed-cost structure is a strategic decision for companies. CVP analysis helps managers compare the risk of losses when revenues are low and the upside profits when revenues are high for different proportions of variable and fixed costs in a company’s cost structure. 7. How can managers apply Managers apply CVP analysis in a company producing multiple CVP analysis to a company products by assuming the sales mix of products sold remains producing multiple constant as the total quantity of units sold changes. products? 8. How do managers apply Managers define output measures such as passenger-miles in CVP analysis in service and the case of airlines or patient-days in the context of hospitals not-for-profit organizations? and identify costs that are fixed and those that vary with these measures of output. 9. What is the difference Contribution margin is revenues minus all variable costs between contribution margin whereas gross margin is revenues minus cost of goods sold. and gross margin? Contribution margin measures the risk of a loss, whereas gross margin measures the competitiveness of a product. CHAPTER 6: MASTER BUDGET 1. What is the master budget, The master budget summarizes the financial projections of all and why is it useful? the company’s budgets. It expresses management’s operating and financing plans—the formalized outline of the company’s financial objectives and how they will be attained. Budgets are tools that, by themselves, are neither good nor bad. Budgets are useful when administered skillfully. 2. When should a company prepare budgets? What are the advantages of preparing budgets? Budgets should be prepared when their expected benefits exceed their expected costs. There are four key advantages of budgets: (a) they compel strategic analysis and planning, (b) they promote coordination and communication among subunits of the company, (c) they provide a framework for judging performance and facilitating learning, and (d) they motivate managers and other employees. 3. What is the operating The operating budget is the budgeted income statement and its budget and what are its supporting budget schedules. The starting point for the operating components? budget is generally the revenues budget. The following supporting schedules are derived from the revenues budget and the activities needed to support the revenues budget: production budget, direct materials usage budget, direct materials purchases budget, direct manufacturing labor cost budget, manufacturing overhead costs budget, ending inventories budget, cost of goods sold budget, R&D/product design cost budget, marketing cost budget, distribution cost budget, and customer-service cost budget. 6. Why are human factors The administration of budgets requires education, participation, crucial in budgeting? persuasion, and intelligent interpretation. When wisely administered, budgets create commitment, accountability, and honest communication among employees and can be used as the basis for continuous improvement efforts. When badly managed, budgeting can lead to game-playing and budgetary slack—the practice of making budget targets more easily achievable. 7. What are the special challenges involved in budgeting at multinational companies? Budgeting is a valuable tool for multinational companies but is challenging because of the uncertainties posed by operating in multiple countries. In addition to budgeting in different currencies, managers in multinational companies also need to budget for foreign exchange rates and consider the political, legal, and economic environments of the different countries in which they operate. In times of high uncertainty, managers use budgets to help the organization learn and adapt to its circumstances rather than to evaluate performance. CHAPTER 11: DECISION MAKING AND RELEVANT INFORMATION 1. What is the five-step process that managers can use to make decisions? The five-step decision-making process is (a) identify the problem and uncertainties, (b) obtain information, (c) make predictions about the future, (d) make decisions by choosing among alternatives, and (e) implement the decision, evaluate performance, and learn. 3. What is and why consider insourcing decisions? an opportunity cost should managers it when making versus-outsourcing Opportunity cost is the contribution to income that is forgone by not using a limited resource in its next-best alternative use. Opportunity cost is included in decision making because the relevant cost of any decision is (a) the incremental cost of the decision plus (b) the opportunity cost of the profit forgone from making that decision. When capacity is constrained, managers must consider the opportunity cost of using the capacity when deciding whether to produce the product in-house versus outsourcing it. 8. How can conflicts arise between the decision model a manager uses and the performance evaluation model top management uses to evaluate that manager? Top management faces a persistent challenge: making sure that the performance-evaluation model of lower-level managers is consistent with the decision model. A common inconsistency is to tell these managers to take a multiple-year view in their decision making but then to judge their performance only on the basis of the current year’s operating income. 6. In deciding to add or drop customers or to add or discontinue branch offices or business divisions, what should managers focus on and how should they take into account allocated overhead costs? When making decisions about adding or dropping customers or adding or discontinuing branch offices and business divisions, managers should focus on only those costs that will change and any opportunity costs. Managers should ignore allocated overhead costs. 5. What steps can managers take to manage bottlenecks? Managers can take four steps to manage bottlenecks: (a) recognize that the bottleneck operation determines throughput (contribution) margin, (b) identify the bottleneck, (c) keep the bottleneck busy and subordinate all nonbottleneck operations to the bottleneck operation, and (d) increase bottleneck efficiency and capacity. CHAPTER 13: PRICING DECISIONS AND COST MANAGEMENT 1. What are the three Customers, competitors, and costs influence prices through their major factors affecting effects on demand and supply; customers and competitors affect pricing decisions? demand; and costs affect supply 2. How do companies Companies consider all future costs (whether variable or fixed in the make long-run pricing short run) and use a market-based or a cost-based pricing approach decisions? to earn a target return on investment. 3. How do companies One approach to long-run pricing is to determine a target price. determine target cost? Target price is the estimated price that potential customers are willing to pay for a product or service. Target cost per unit equals target price minus target operating income per unit. Target cost per unit is the estimated long-run cost of a product or service that, when sold, enables the company to achieve target operating income per unit. Value-engineering methods help a company make the cost improvements necessary to achieve target cost.