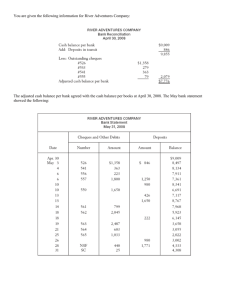

CHAPTER 3 Reconciliations: Bank reconciliations Progression ► Grade 10: Preparation of debtors’ and creditors’ lists to reconcile with the debtors’ and creditors’ control accounts ► Grade 11: Preparation of reconciliation statements by reconciling to bank and creditors’ statements ► Grade 12: Analysis and interpretation of bank, debtors’ and creditors’ reconciliations and age-analysis _______________________________________________ Introduction What are bank reconciliations? ► Bank reconciliations involve a monthly comparison of the business’s cash records (CRJ and CPJ) with the bank’s records of the business’s transactions (the bank statement). ► In theory, the cash transactions recorded by the business should exactly match the transactions recorded by the bank. ► However in practice this is seldom the case, for a variety of reasons such as: Money that has been received by the business, but not yet deposited in the bank. Cheques that have been paid by the business, but not yet presented to the bank for payment. Payments made by the bank on behalf of the business, but not yet recorded by the business. Errors made by either the business or the bank; or possibly even fraudulent transactions committed by employees of the business or the bank. Why are bank reconciliations important? ► Bank reconciliations are an important part of the business’s internal control system. ► By performing a bank reconciliation, the business can: check the accuracy of its records against those of the bank account for transactions processed by the bank on behalf of the business uncover errors or fraudulent transactions __________________________________________________________________________________ Internal control of money ► The business’s current bank account is probably its most frequently used account. ► Money is deposited, withdrawn and transferred on a daily basis. ► Due to the large volume of these transactions, there is a significant risk of errors occurring. ► It is thus very important to ensure that all the money is accounted for and properly controlled. ► In order to comply with proper accounting control procedures, a business should: record all its cash receipts and cash payments. ensure that all money received is supported by a source document. check that money and cheques received agree with the deposit slip. require that cheques are signed by at least two authorised signatories. preferably make all payments by cheque or EFT. __________________________________________________________________________________ Accounting procedure for recording money received ► When money is received, the business will issue: a receipt a cash invoice; or a till slip. ► These source documents are then used to record the transaction in the Cash Receipts Journal. ► Each amount received is first entered in the Analysis of receipts column in the CRJ. ► At the end of each day, these amounts are added together and the total is entered into the Bank column in the CRJ. ► This total amount represents all the money received on that particular day. ► This total amount is the amount that is entered on the deposit slip and deposited at the bank. __________________________________________________________________________________ Accounting procedure for recording money received (cont.) Example Transaction: The total received by Pule’s Service Centre on 1 June 2019 is R80 000. Required: Record this transaction in the CRJ of Pule’s Service Centre. Also show how this amount would be recorded on a deposit slip. Solution Cash Receipts Journal of Pule’s Service Centre for June 2019 Doc no. Day 01 1 Details P George Fol. Analysis of receipts 80 000 00 CRJ1 Bank Sundry accounts Amount Details 80 000 00 80 000 00 Capital Accounting procedure for recording money paid ► There are a variety of methods that businesses use to make payments, such as: Cheques Credit and debit cards Internet transfers (EFTs) ► All payments must be recorded on source documents. ► The source documents are then used to record the payment in the Cash Payments Journal. Payments by means of cheque ► A cheque is a legal document that instructs the bank: to pay the amount of money written on the cheque to the person or entity written on the cheque from the business’s bank account. ► A cheque is valid for six months from the date on the cheque. ► A cheque that is not cashed within the six months is called a “stale cheque”. __________________________________________________________________________________ Accounting procedure for recording money paid (cont.) Example Transactions: Pule’s Service Centre made two payments by cheque on 2 June 2019. The cheque counterfoils (shown alongside) remained in the cheque book and are the source documents that will be used to record the transactions. Required: Record these transactions in the Cash Payments Journal of Pule’s Service Centre. Solution Cash Payments Journal of Pule’s Service Centre for June 2019 Doc no. Day 01 2 02 Name of Payee Fol. Bank CPJ1 Materials Sundry accounts Amount Details Unicity Council 1 500 00 City Spares 9 200 00 1 500 00 Trading license 9 200 00 Cheque fraud ► Bank reconciliations are an essential part of a business’s system of internal control. ► They play an important role in identifying bank errors and detecting fraud. ► Cheques are often used as a means for committing fraud and cheque fraud is a major threat to most businesses. ► In order to protect against the risk of cheque fraud, it is critical that businesses: perform regular bank reconciliations and implement adequate control processes. Click here to view a list guidelines for preventing and safeguarding against cheque fraud __________________________________________________________________________________ Services offered by a commercial bank Commercial banks offer the business two main services: ► they look after the business’s money in a bank account. ► they lend money to the business. Opening and using a bank account ► When the owner of the business opens an account at the commercial bank, an initial amount of money is deposited into the bank account. ► When the business receives money, it is deposited into the bank account. ► When the business makes a payment, the amount paid is transferred out of the bank account. __________________________________________________________________________________ Services offered by a commercial bank (cont.) Payment options offered by commercial banks ► Cash payments can be made by withdrawing money either from a branch of the bank or from an ATM machine. ► Cheque payments can be made by writing out a cheque. ► Internet payments (EFT’s) can be made by transferring funds via the Internet using a secure website provided by the bank. ► Debit card payments can be made by using a debit card, the money paid is deducted directly from the bank account. ► Debit order or stop order payments can be made by the bank on behalf the business. These payments are pre-arranged with the bank and are usually regular monthly payments, such as insurance premiums or cellphone contracts. ► Telephone banking payments can be made by transferring funds via the telephone using a secure password to access the bank account. __________________________________________________________________________________ Fees charged by a commercial bank ► Commercial banks charge their customers fees for the services they provide. ► These fees are called “bank charges”. ► Bank charges include fees charged to the business for: making deposits, withdrawals or payments receiving bank statements making balance enquiries ► This is the “price” that the business pays for having the bank look after its money. ► Bank charges vary from one bank to another. ► Some banks offer a fixed monthly charge that allows the business to make a certain number of transactions each month. __________________________________________________________________________________ The bank reconciliation process ► The bank reconciliation is an essential control process that should be performed every month. ► It involves a comparison of the cash transactions in the business’s records (CRJ and CPJ) with those of the bank. ► At the end of each month, the business will receive the bank statement from its bank. ► The bank statement is a reflection of the bank’s transactions with the business. ► The bank statement usually includes certain transactions that have been recorded by the bank, which do not appear in the books of the business. ► There are also usually certain transactions that have been recorded by the business, which do not appear on the bank statement. ► The bank reconciliation process reveals these discrepancies and provides a method for accounting for these differences. The reconciliation process may be divided into three parts: ► Part 1: Starting the bank reconciliation process ► Part 2: Completing the bank reconciliation process ► Part 3: Drawing up the Bank Reconciliation Statement __________________________________________________________________________________ The bank reconciliation process (cont.) Part 1: Starting the bank reconciliation process This part of the process involves the following steps: Compare the credit column of the bank statement with the Bank column of the CRJ. Compare the debit column of the bank statement with the Bank column of the CPJ. Tick off items which appear in both the bank statement and the cash journals. Circle all the items which have not been ticked off. ► The items that are circled will be all the items that did not appear in both the bank statement and the cash journals. ► The possible reasons for the circled items will be discussed using the following headings: Circled items in the Bank column of the CRJ Circled items in the Bank column of the CPJ Circled items in the debit column of the bank statement Circled items in the credit column of the bank statement __________________________________________________________________________________ The bank reconciliation process (cont.) Circled items in the Bank column of the CRJ are usually: Outstanding deposits ► ► These amounts have been received by the business and recorded in the CRJ, but have either: not yet been received by the bank, or not yet recorded by the bank. This is normally referred to as a timing difference and these amounts will usually appear on the following month’s bank statement. Circled items in the Bank column of the CPJ are usually: Cheques not yet presented to the bank for payment ► These cheques have been issued by the business and recorded in the CPJ, but the payee has not yet presented the cheque to bank for payment. ► This is also referred to as a timing difference and these cheque will often appear on the following month’s bank statement. ► Remember that a cheque is valid for six months, so the payee may take a while to present the cheque to the bank for payment. __________________________________________________________________________________ The bank reconciliation process (cont.) Circled items in the debit column of the bank statement could be: Bank charges ► The fees charged by the bank for administering the bank account of the business. ► E.g. Monthly service fee, cheque book fee, cash handling fee, transaction charges Stop orders ► An instruction given to the bank to pay a third party, a fixed amount on a regular basis. Debit orders ► An agreement between the business and a third party, which allows the third party to receive payment from the business’s bank account. Debit orders may be fixed or variable amounts. Interest on overdraft ► When the business has an overdrawn balance, it will pay interest on the amount that is overdrawn for the period of time that it is overdrawn. Dishonoured cheques ► The bank will dishonour cheques for the following reasons: no money in the drawers account the drawer is deceased or insolvent refer to drawer there is a problem on the cheque (e.g. incorrect signature or amount in words not matching amount in figures). __________________________________________________________________________________ The bank reconciliation process (cont.) Circled items in the credit column of the bank statement could be: Direct deposits ► Money can be directly deposited into the business’s bank account by anyone owing money to the business. Interest on current account ► When the business has a favourable bank balance, it will earn interest on the favourable balance for the period of time that it is favourable. __________________________________________________________________________________ The bank reconciliation process (cont.) Part 2: Completing the bank reconciliation process This part of the process involves the following steps: Enter the totals into the CRJ, CPJ and Bank account. Circled amounts in the credit (+) column of the bank statement must be entered into the CRJ. Circled amounts in the debit (–) column of the bank statement must be entered into the CPJ. Total the bank columns of the CRJ and CPJ and post these totals to the Bank account. ► The business cannot add entries onto the bank statement in order to account for the amounts that appear in the Cash Journals, but not on the bank statement. ► Therefore these differences are accounted for by drawing up a Bank Reconciliation Statement (BRS) in the books of the business. _____________________________________________________________________________ The bank reconciliation process (cont.) Part 3: Drawing up the Bank Reconciliation Statement This part of the process involves the following steps: Enter the closing balance on the bank statement into the BRS. Circled amounts in the CRJ must be entered into the credit column of the BRS. Circled amounts in the CPJ must be entered into the debit column of the BRS. Enter the closing balance in the bank account into the BRS. Shu-Biz Stores Bank Reconciliation Statement on 31 August 2019 Debit Credit Credit balance as per bank statement Credit outstanding deposits Debit outstanding cheques: no. 02 1 250 00 no. 05 10 820 00 no. 11 6 450 00 no. 13 765 00 no. 14 265 00 Debit balance as per Bank account 22 745 00 42 295 00 32 955 00 9 340 00 42 295 00 Overdrawn bank balance Overdraft ► An overdraft is a facility provided by banks, which allows businesses to overdraw on their current bank account. ► This means that the business is allowed to spend more money than it has in its account. ► When this happens, the business will owe the bank money and the bank will be a liability in the books of the business. In the books of the business (Shu-Biz Stores) (–) Bank (Liability) All deposits decrease the overdraft (+) All withdrawals increase the overdraft In the books of the business, the bank account has a credit balance. In the books of the bank (First Bank) (+) Shu-Biz Stores (Asset) All withdrawals increase the amount owing to the bank (–) All deposits decrease the amount owing to the bank In the books of the bank, the business’s account has a debit balance. Interest on overdraft ► The bank charges the business interest on the amount that is overdrawn. ► This interest is known as interest on overdraft and is an expense to the business. ► The bank charges this interest directly to the business’s account and the amount charged will appear on the bank statement at the end of the month. ► Interest on overdraft is not part of Bank charges and must always be accounted for separately. _____________________________________________________________________________________ Comparing the bank statement with the previous month’s Bank Reconciliation Statement ► As previously mentioned, due to timing differences some items might appear in the cash journals of the business, but not on the bank statement. These items are normally either: Outstanding deposits – deposits that have not yet been received or recorded by the bank Outstanding cheques – cheques that have not yet been presented to the bank for payment ► Remember that these outstanding items are recorded on the Bank Reconciliation Statement. ► These outstanding items will often be received and recorded by the bank in the following month and will then appear on the following month’s bank statement. ► Therefore, when performing a bank reconciliation, the business should also compare the bank statement with the previous month’s Bank Reconciliation Statement, in order to check if any of the outstanding items from the previous month have been received and record by the bank. ► Outstanding items from the previous month’s Bank Reconciliation Statement, which appear on the current month’s bank statement should be: ► Ticked off in both the previous month’s Bank Reconciliation Statement and the current month’s bank statement. Any outstanding items from the previous month’s Bank Reconciliation Statement, which still do not appear on the current month’s bank statement should be: Circled in the previous month’s Bank Reconciliation Statement. These items are thus still outstanding and must be recorded again (as outstanding) in the current month’s Bank Reconciliation Statement. ________________________________________________________________________________________ Cancelled cheques Cheques issued by the business may need to be cancelled for various reasons, such as: Stale cheque ► the cheque has become stale (older than six months). ► the bank does not need to be notified as the payee will not be able to present this cheque for payment. Stolen or lost cheque ► the cheque has been stolen or lost. ► the business will stop payment on the cheque by notifying the bank and will usually issue a new cheque to the payee. Non-performance ► the business stops payment on a cheque that was issued for a service that was either not received or not properly performed. ► E.g. A cheque was issued for advertising, but the advert did not appear in the newspaper. Procedure for cancelling a cheque in the books of the business: ► Remember that when the cheque was issued in would have been recorded in the CPJ. ► The entry in the CPJ can not be deleted. ► So the transaction must be cancelled (reversed) by recording the equivalent entry in the CRJ. ___________________________________________________________________________________ Correction of errors ► One of the main reasons for performing a bank reconciliation is to check for errors. ► Errors may occur, either: in the cash journals (CRJ and CPJ), or on the bank statement. Errors in the cash journals ► Errors in the cash journals usually relate to amounts being entered incorrectly. ► These errors do not affect the bank’s records and must therefore be corrected by making an appropriate entry in the cash journals of the business. ► If the amount entered in the: CRJ is too little correct by entering the difference in the CRJ CRJ is too much correct by entering the difference in the CPJ CPJ is too little correct by entering the difference in the CPJ CPJ is too much correct by entering the difference in the CRJ ___________________________________________________________________________________ Correction of errors (cont.) Errors on the bank statement ► Errors on the bank statement usually relate to, either: amounts being recorded incorrectly, or transactions being entered erroneously in the business’s account. ► The business should notify the bank if it discovers any such error and the bank will then correct this error by making an appropriate entry in its books. ► This correction entry will appear on the following month’s bank statement. ► In order to reconcile the cash journals with the bank statement, the business must make an entry in the Bank Reconciliation Statement (BRS). ► This entry should match the correction entry that the bank is expected to make. ► So, if the bank is expected to correct the error by: ► debiting the business’s account then the business must debit the BRS crediting the business’s account then the business must credit the BRS When the comparison is done in the following month, this entry in the BRS will cancel out the bank’s correction entry (which will appear on the following month’s bank statement). ________________________________________________________________________________________ Comparing the Salaries Journal with the bank statement ► If a business pay its employees by cheque, then the Salaries Journal must also be compared with the bank statement. ► Although the total amount paid for salaries is recorded in the CPJ, the Salaries Journal shows: the separate amounts paid to each employee and the individual cheque numbers. ► These amounts and cheque numbers will need to be compared with those that appear on the bank statement. ► As with other payees, employees need to present their cheques to the bank for payment. ► Thus there might be timing differences between the business issuing the cheques and the cheques being presented to the bank. ► Any outstanding salary cheques must be entered into the BRS, in the same way as ordinary outstanding cheques are recorded. ________________________________________________________________________________________ Post-dated cheques Post-dated cheques are cheques that have been issued for a date in the future. Example: A cheque is issued and signed on 12 September 2019, but the date on the cheque is 20 October 2019. This cheque will only be paid by the bank on or after 20 October 2019. Post-dated cheques issued by the business ► A post-dated cheque issued must be entered in the CPJ on the day that it was issued. ► The payee will only be able to present this cheque on or after the date on the cheque. ► The post-dated cheque will thus be outstanding until that date and will be entered into the BRS (in the same way as ordinary outstanding cheques are recorded). Post-dated cheques received by the business ► A post-dated cheque received will not be entered in the CRJ on the day that it was received. ► This cheque will be written up in the Post-dated Cheques Register and will only be entered in the CRJ on the date that is written on the cheque. ► The reason for this is that all receipts in the CRJ must be deposited and a post-dated cheque cannot be deposited until the day that it is dated. ► Thus, since no entry is made when a post-dated cheque is received, it will have no effect on the bank reconciliation process. ________________________________________________________________________________________ Completing the bank reconciliation when comparisons are already done ► Often you will be asked to complete the bank reconciliation process from information where the comparisons between the CRJ, CPJ and bank statement have already been done. ► In this case, you will be given a list of the differences, errors and omissions. ► You will be require to: make the supplementary entries in the CRJ and CPJ draw up the Bank account prepare the Bank Reconciliation Statement ___________________________________________________________________________________ Entering information directly into the Bank account ► Sometimes a reconciliation is done directly into the Bank account in the General Ledger. ► This is done if the CRJ and CPJ are already closed off. ► Entries are made directly into the Bank account and the double-entry principle is applied. ► Just remember that any supplementary entry that would have been made in the: CRJ will be entered on the debit side of the Bank account CPJ will be entered on the credit side of the Bank account ___________________________________________________________________________________ Summary of where to record transactions involved in bank reconciliations Transaction CRJ CPJ Bank Reconciliation Statement Dr Direct deposit into bank account (on BS) Interest on favourable bank balance (on BS) Cancelled cheques (stale, stop payment, stolen or altered cheques) Error in the CPJ – where amount in CPJ is more than the original cheque Debit orders, Stop orders, Electronic payments (on BS) Bank charges, Interest on overdraft (on BS) Dishonoured cheques (on BS) Error in the CPJ – where amount in CPJ is less than the original cheque Cheques issued, but not appearing on BS Cheques outstanding on previous BRS and still not appearing on current BS Post-dated cheques issued Amount incorrectly credited on BS Outstanding deposits Amount incorrectly debited on BS Cheques outstanding on previous BRS, but appearing on current BS Deposit outstanding on previous BRS, but appearing on current BS Post-dated cheques received No entry Cr Solutions to activities Activity 3.1 Activity 3.11 Activity 3.2 Activity 3.12 Activity 3.3 Activity 3.13 Activity 3.4 Activity 3.14 Activity 3.5 Activity 3.6 Informal assessment 3.1 Activity 3.7 Informal assessment 3.2 Activity 3.8 Informal assessment 3.3 Activity 3.9 Activity 3.10 _______________________________________________________________________ Please note: Adobe Reader is required in order to view the solutions to the activities. Click here to go to the Adobe Reader download website.