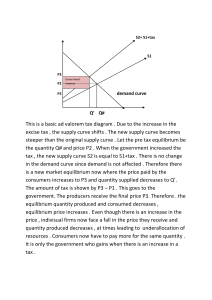

Unit 3 Households & Firms earn income – yes, they earn income. Household & Firms spending. Firms spend on the factors of production & household spend on the goods and service market. Firms provided goods and services and in return earn income. Household & Firms exchange. The exchange happens in the factor market & goods and services market. Household send factors of production through the firms which firm needs to pay for the factors of production. When the firm pays for the factor of production it becomes income for households. Households & Firms pay tax to the government. Government receives labour from FOP, in return the government spends. Firms borrow money from banks for capital injection to spend on raw material (machinery) Banks are part of the circular flow in the financial section. Exporting is an injection. Importing is a leakage. Closed economy is only looking at domestic/ closed to trading. When saving occurs money is leaking but when there is capital investment money is being invested. Unit 4 Demand & Supply People who demand must have money or ability to pay. WE DEMAND MORE WHEN THE PRICE IS LOW. The price of related products which are related to each other either complements or substitutes. Examples of substitutes products affect demand: Fresh milk or power milk, beef or chicken and petrol or diesel. Examples of complements product affect demand: book & pen, shocks and shoes and butter & bread. Income of consumer affects demand. More money more demand less money less demand. Taste or preference – demand according to your preference. Number of people in the household – more people more demand Demand curve slopes down from down from left to right. It’s called a negative slop as the relation between price and demand. High price – low demand. Price and quantity have a opposite relationship. Every point on the graph represent a combination. Join points on the graph which is called a demand curve. At R4 we demand 3kg tomatoes. When price goes down, we demand more. With price of tomatoes each person demanded is different. To calculate market demand you add demand by individuals. (eg price of tomatoes 5, Avesh 5kg, Candice 2kg, Mum 0kg = MARKET DEMAND = 7KG ) Movements along the demand curve it is possible to move along the demand curve as result of price. CETERIS PARIBUS – all other factors remain (eg: substitutes products, complements product, Income of consumer, Taste or preference and Number of people in the household) constant besides price. Shift in the demand curve Can move to the left or right. Anything else other than price will cause a shift in demand. (eg income changes). We must hold price constant and let the other things change. We cannot allow price to come into the picture. • Related goods (price of substitutes). Price of burgers versus pizza. Because pizza cost less you will demand more which will shift right on the supply curve. • Related goods (complements). If golf balls drop, the demand for clubs will increase. • Changes in income – more money you demand more products. If income decrease you buy less. This will cause a shift along the curve, but price must be constant. Taste & Preferences – if you don’t like burgers one day the shift on the curve will be left. Household size- more people will demand more. This will cause a right shift on the curve. Expectation – Petrol as example. When low you buy more. Distribution of Income – Distribution of income to low-income household. Rich people pay more tax. The demand curve of the low income people will shift right. • • • • Supply – Supply is from firm/producer. The consumer demand and the curve belong to them whereas the supply curve belongs to the producer. It has a positive slope. Vertical line is price and horizontal line is quantity. Supplier will supply more when price goes up. Price and quantity on the supply curve move in the same direction. What determines supply • • • • Price of the product Price of alternative products - if a firm makes shoes or belt depending on which product cost they will make more of that to earn more revenue. Expected future price State of technology – better technology change in supply. Market Supply – you add the different supply points at the price We can also move along the supply curve. Price causes movement along the supply curve. High price more quantity supplied and low price less quantity supplied. Supply curve can shift right or left Market Equilibrium – where curves intersect, is the producer and consumer agree. If do not intersects producer and consumer are Dis Equilibrium. Do not interfere as they will come at equilibrium Only place where there is no extra demand or supply is at Equilibrium. Unit 5 – DEMAND IN SUPPLY IN ACTION Let the market forces determine equilibrium. Change in quantity demanded – The PRICE!! Causes a movement along the demand curve but everything else must be kept constant. Change in Demand – the curve is shifting • • • • • Increase in the price of substitute Decrease on the price of complementary product Increase in consumer income Positive change in preferences towards the product Expectations of a price The red line shows an increase in demand. Above could be the cause for the shift. The supply curve stayed the same. We have a new equilibrium. Consumers are happy to buy more at lower price (P0 below) At the old price at P0 there will be excess demand. NEW EQUILIBRIUM at E1. Decrease in demand: THE DEMAND WILL SHIFT LEFT The price of substitute fall The price of a complementary product increase The consumers income fall There be a reduced preference for the product The price of the product expected to fall When firms have extra stock, they lower the price. When there is a shift in the curve, we end uo with a new equilibrium. Change in SUPPLY – it can shift to right or left • • • Price of an alternative product Reduction in the price of the factors of production An improvement in the factors of products. The price of alternative will down causing a right shift. Old Equilibrium = E Excesss supply is shown below = S = S1. Demand remains the sam There’s a new insection and equilibrium. The customer pay’s less for more quantity. (SHIFT TO THE RIGHT). THE FIRMS IN ORDER TO SELL EXCESS SUPPLY AT P0 HAD TO LOWER THEIR PRICES AND NEW EQUILIBRIUM WAS FORMED. THE SUPPLY CURVE CAN ALSO SHIFT TO THE LEFT – • • • The price of alternative product inreases Increase in the factors of production Poorer technology will shift left SUPPLY CURVE SHIFT LEFT • • • At the old price we have excess demand. If too much demand and less supply. YOU WOULD OFFER A HIGHER PRICE. The demand and supply can shift SIMULTANEOUSLY. Government Intervention The government interferes with equilibrium price. • • They set a maximum price (known as price ceilings). They set a minimum price (known as price floors). Society losses when government interferes with the price. WHICH IS CALLED A WELLFARE LOSS TO SOCEITY. If the maximum price is set above equilibrium, it’s no problem because market forces will bring it down. If the maximum price is set below equilibrium that’s a problem as the market forces is unable to take it back to equilibrium where there was NO government interference. E = intersection between demand and supply agreement between consumer and firm. Government can set the price PM as below. The equilibrium was at P0. At PM firms supply less (Q1) because of the price being low. At PM consumer demand (Q2) because of the price being low. At PM there is excess demand. To get rid of the excess demand we higher the price until excess demand is sorted out known as “first come first serve” or one per customer. The market forces can not fix the market forces. MORE PEOPLE DEMANDING WITH LESS SUPPLY. • • • • • • • • • E – is when the market is working. Government set price at PM. When the price above P1 (D , E, P1) the triangle is the consumer surplus. It below the demand line and above the price line. It was where surplus was maximize. The blue line below the consumer (DEMAND LINE). The area above the green line under the price line is the produce surplus To give society the most benefit we must the maximize the total surplus ( CONSUMER + FIRM SURPLUS = TOTAL SURPLUS) B now belongs to the consumer surplus. New equilibrium B belongs to the consumer surplus. A,C is surplus that has been lost. Known as the deadweight loss At R40 only 4 is demanded (blue line), and supply is 9 (green line) • • • • Consumer surplus is P,R, PM (new equilibrium) Consumer surplus is P,E, P1(old equilibrium) O,PM,R,T is the firm surplus. The producer gained A B,C has been lost. Unit 6 – Elasticity Price elasticity is how responsive of the quantity demanded to change in price of the product. Refers to the % change in the quantity divided by the % change in price. 𝑷𝒓𝒊𝒄𝒆 𝑬𝒍𝒂𝒔𝒕𝒊𝒄𝒊𝒕𝒚 (𝑬𝒑) = % 𝐜𝐡𝐚𝐧𝐠𝐞 𝐢𝐧 𝐪𝐮𝐚𝐧𝐭𝐢𝐭𝐲 % 𝐂𝐡𝐚𝐧𝐠𝐞 𝐢𝐧 𝐩𝐫𝐢𝐜𝐞 When ep = 1 UNITARY ELASTIC When 0 < ep < 1 INELASTIC DEMAND When 1 < ep < infinity – ELASTIC DEMAND When ep = infinity ep PERFECTLY ELASTIC • • At EP = 0 then total revenue is at maximin Below shows total revenue is link to elasticity • • • • The below table shows Total revenue increasing when elasticity is = 1. Then it is starts falling when ep < 1 to 0 When Ep 0, Total revenue is also 0 When Ep is infinity, Total revenue is also 0 • • When Ep = 0, then Perfectly Inelastic, Quantity DOES NOT respond to a change in price. It is perfectly inelastic. They didn’t buy less they still bought the same amount. Example BREAD When Ep <1, then Inelastic Demand, the quantity demanded goes down by 2% as per below. The change in quantity is less than the change in price. Example (Petrol, Cigarettes). • • Ep = 1 then Unitary, the 10% in price resulted in a 10% change in quantity demanded. Ep > 1 then Elastic, A 10% in price results in a 15% change in quantity demanded. – Flat curve • Ep = infinity, the demand curve will be horizontal, At P1 customer are willing any amount. If you increase the price, they will stop buying. What determines price ELASTICITY • Number of substitutes – if are substitutes the demand will be elastic • Degree of complementarity – These are products used together, petrol and cars. They inelastic • Type of wants satisfied • Time – if you are rushing you are not concern around the price – Inelastic • Proportion of income spent • Definition of the market Income Elasticity The theory of product & cost • • • • Business produces good and services to EARN PROFIT To earn profit business must exclude expenses taken to make the product In SA we have a lot of Informal traders. If firms don’t make profit, they will not survive. Revenue = Price * Quantity (P*Q) Average Revenue = Total Revenue/Quantity (TR/Q) Marginal Revenue = Total Revenue/Quantity (TR/Q) Economist – Your cost is your opportunity cost (what you sacrificed). (Consider implicit and explicit cost) Accountant – Actual expenses incurred (what did you pay for? eg petrol wages paid). Consider explicit cost only Implicit cost is not in money is WHAT YOU GAVE UP 3 different types of profit Total Profit or accounting profit – Total Revenue – Explicit Cost Normal profit – your best return you could have made in another business Economic profit – Total Revenue – (Explicit - Implicit cost/opportunity cost) Accounting gets recorded in your financial statements COST TC = FC +VC AC = TC/Q MC = TC/Q (cost of producing one extra burger)