Accounting Basics: Debits, Credits, and Adjusting Entries

advertisement

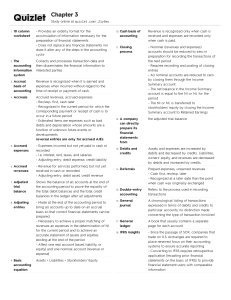

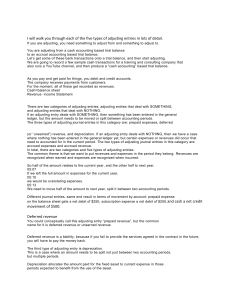

The following accounts are increased with a Debit: • • • • Dividends (Withdraws) Expenses Assets Losses D - E - A - L when recalling the accounts that are increased with a debit. The following accounts are increased with a Credit: • • • • • Gains Income Revenues Liabilities Stockholders' (Owner's) Equity G - I - R - L - S when recalling the accounts that are increased with a credit. Categories of Adjusting Entries Most adjusting entries fall into one of four general categories: 1. Converting assets to expenses (Deferred Expenses). Results from cash being paid prior to an expense being incurred. 2. Converting liabilities to revenue (Deferred Revenue). Results from cash being received prior to revenue being earned. 3. Accruing unpaid expenses (Accrued Expenses). Results from expenses being incurred before cash is paid. 4. Accruing uncollected revenue (Accrued Revenue). Results from revenue being earned before cash is received