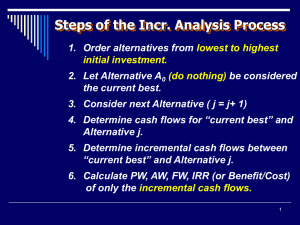

Engineering Economics Mubashir Rasheed Multiple IRR Values In the cash flow series presented thus far, the algebraic signs on the net cash flows changed only once, usually from minus in year 0 to plus at some time during the series This is called a conventional ( or simple) cash flow series However, for some series the net cash flows switch between positive and negative from one year to another, so there is more than one sign change. Such a series is called nonconventional (nonsimple) Multiple IRR Values When there is more than one sign change in the net cash flows, it is possible that there will be multiple i * values There are two tests to perform in sequence on the nonconventional series to determine if there is one unique value or possibly multiple i *values that are real numbers. Multiple IRR Values Test 1: (Descartes’) rule of signs states that the total number of realnumber roots is always less than or equal to the number of sign changes in the series Test 2: Cumulative cash flow sign test, also known as Norstrom’s criterion, states that only one sign change in a series of cumulative cash flows which starts negatively indicates that there is one positive root to the polynomial relation Zero values in the series are neglected when applying Norstrom’s criterion Observe the sign of S0 and count the sign changes in the series S0 , S1 , . . . , S n . Only if S0 0 and signs change one time in the series is there a single, real-number, positive i *. Multiple IRR Values Example Multiple IRR Values Example Multiple IRR Values Example Multiple IRR Values Example Multiple IRR Values Example EER: External Rate of Return The reinvestment assumption of the IRR method may not be valid in an engineering economy study. For instance, if a firm’s MARR is 20% per year and the IRR for a project is 42.4%, it may not be possible for the firm to reinvest net cash proceeds from the project at much more than 20% This situation, coupled with the computational demands and possible multiple interest rates associated with the IRR method, has given rise to other rate of return methods that can remedy some of these weaknesses One such method is the ERR method If this external reinvestment rate, which is usually the firm’s MARR, happens to equal the project’s IRR, then the ERR method produces results identical to those of the IRR method In general, three steps are used in the calculating procedure. First, all net cash outflows are discounted to time zero (the present) at ∈% per compounding period. Second, all net cash inflows are compounded to period N at ∈%. Third, the ERR, which is the interest rate that establishes equivalence between the two quantities, is determined. EER: External Rate of Return The absolute value of the present equivalent worth of the net cash outflows at ∈% (first step) is used in this last step. In equation form, the ERR is the i′% at which In general, three steps are used in the calculating procedure. First, all net cash outflows are discounted to time zero (the present) at ∈% per compounding period. Second, all net cash inflows are compounded to period N at ∈%. Third, the ERR, which is the interest rate that establishes equivalence between the two quantities, is determined. EER: External Rate of Return The absolute value of the present equivalent worth of the net cash outflows at ∈% (first step) is used in this last step. In equation form, the ERR is the i′% at which EER: External Rate of Return Example EER: External Rate of Return Example When two or more mutually exclusive alternatives are evaluated, engineering economy can identify the one alternative that is the best economically Incremental Analysis technique is used to selected the best alternative among the presented IRR of Multiple Alternatives When independent projects are evaluated, no incremental analysis is necessary between projects. Each project is evaluated separately from others, and more than one can be selected. IRR of Multiple Alternatives To conduct an incremental ROR analysis, it is necessary to calculate the incremental cash flow series over the lives of the alternatives. IRR of Multiple Alternatives Incremental analysis The incremental ROR method requires that the equal-service requirement be met. Therefore, the LCM (least common multiple) of lives for each pairwise comparison must be used. All the assumptions of equal service present for PW analysis are necessary for the incremental IRR method. When a study period is established, only this number of years is used for the evaluation. All incremental cash flows outside the period are neglected Only for the purpose of simplification, use the convention that between two alternatives, the one with the larger initial investment will be regarded as alternative B . Incremental cash flow = cash flow B - cash flow A IRR of Multiple Alternatives Incremental analysis IRR of Multiple Alternatives Incremental analysis IRR of Multiple Alternatives Incremental analysis IRR of Multiple Alternatives Incremental analysis The incremental cash flows in year 0 of Tables 8–2 and 8–3 reflect the extra investment or cost required if the alternative with the larger first cost is selected IRR of Multiple Alternatives Incremental analysis If the incremental cash flows of the larger investment don’t justify it, we must select the cheaper one. In Example the new drill press requires an extra investment of $6000 (Table 8–2). If the new machine is purchased, there will be a “savings” of $1200 per year for 25 years, plus an extra $300 in year 25. The decision to buy the used or new machine can be made on the basis of the profitability of investing the extra $6000 in the new machine. If the equivalent worth of the savings is greater than the equivalent worth of the extra investment at the MARR, the extra investment should be made (i.e., the larger first-cost proposal should be accepted). On the other hand, if the extra investment is not justified by the savings, select the lower-investment proposal If the rate of return available through the incremental cash flow equals or exceeds the MARR, the alternative associated with the extra investment should be selected. IRR of Multiple Alternatives Incremental analysis For multiple revenue alternatives, calculate the internal rate of return i * for each alternative, and eliminate all alternatives that have an i * MARR. Compare the remaining alternatives incrementally When independent projects are evaluated, there is no comparison on the extra investment. The ROR value is used to accept all projects with i * MARR, assuming there is no budget limitation. IRR of Multiple Alternatives Incremental analysis Example IRR of Multiple Alternatives Incremental analysis Example