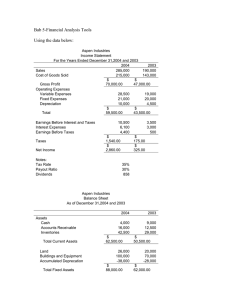

Chapter 2 Financial Statement Analysis Learning Objectives Explain basic financial statements and reports Explain the nature and need of financial analysis. Explain the meaning of financial ratio analysis. Develop skills in using different types of financial ratios. Make classified assessment of firm’s financial performance by using Du-Pont identity. Use comparative ratios and benchmarking for comparative financial analysis. Describe the uses and limitations of financial ratios. Use common size statements in financial analysis. Use percentage change analysis and trend analysis in analysis of financial statements of a firm. Financial Statements and Reports Corporation prepares various types of reports. The Annual Report is one of the basic documents to be issued publicly by corporations. Annual report basically contains two types of information. First section includes a descriptive report of firm’s operation during past year. It also presents new developments, if any, the corporation is going to pursue. Second section of annual report presents four basic financial statements—the income statement, the balance sheet, the statement of stockholders’ equity, and the statement of cash flow. The financial statements contain the basic financial information such as revenues, expenses, assets, liabilities and cash flows of the corporation during a specified period. The balance sheet and the income statement are basic financial statements. The income statement summarizes the revenues and expenditures of a firm during an accounting year The balance sheet summarizes the balance of the firm’s assets, liabilities, and shareholders’ claim outstanding on balance sheet preparation date. Financial statements provide an input to shareholders, creditors and other investors to form expectations about the required return and risk associated with the corporation’s financial affairs. Understanding financial statements is, therefore, important for shareholders, creditors, other investors and for the firm’s management. Role of Financial Statements 1. Financial statements are useful in reporting. 2. Financial statements are useful in business decision making. 3. Financial statements are useful in forecasting. 4. Other uses. Nature and Need of Financial Analysis The process of analyzing relative strengths and weaknesses of a firm’s financial position. Various stakeholders involve in financial analysis to ensure that their interests are being served. Financial analysis corporation’s is financial essential to statement is understand conveying what the about its financial performance. Financial statement analysis involves two types of comparison: Compare a firm’s performance with that of other firms in the same industry; Evaluate trends in the firm’s financial position over time. Financial managers can identify deficiencies in financial performance of the firm and take actions to improve the performance. Financial Ratio Analysis Financial ratios are important tools of financial analysis. The quantitative relationship between two or more sets of financial data derived from income statement and balance sheet. They furnish information about strengths and weaknesses of various aspects of a firm's performance. For example, Unilever Nepal Limited’s income statement for the year ended mid-July 2017 (Table 2.2) shows net income of Rs 965.229 million. We compare the net income against some other data, such as, assets, or equity, or sales, or so on, to derive meaningful conclusion about firm’s profitability. Table 2.1 Unilever Nepal Limited: Balance Sheet as of mid-July (in ‘000) ASSETS Net fixed assets Current Assets: Inventories Accounts receivable Short-term investments Cash and cash equivalents Bank balance other than CCE Total Current Assets Total Assets EQUITY AND LIABILITIES Equity: Share Capital Retained earnings Total Common Equity Long-term debt Current Liabilities: Accounts payables Accruals Notes payables Total Current Liabilities Total Liabilities Total Equity and Liabilities 2017 2016 Rs 581,814 Rs 489,845 Rs 620,026 680,278 1,160,494 241,737 37,480 Rs 2,740,015 Rs 3,321,829 2017 Rs 674,691 297,066 1,036,772 517,566 30,501 Rs 2,556,596 Rs 3,046,441 2016 Rs 92,070 1,982,201 Rs 2,074,271 Rs 12,949 Rs 92,070 1,956,919 Rs 2,048,989 Rs 10,870 Rs 1,019,448 160,332 54,829 Rs 1,234,609 Rs 1,247,557 Rs 3,321,829 Rs 902,020 43,664 40,898 Rs 986,582 Rs 997,452 Rs 3,046,441 Table 2.2 Unilever Nepal Limited: Income Statement for the year ended midJuly (in ‘000) Sales revenue Less: Cost of goods sold except depreciation Depreciation and amortization Other operating expenses Net operating income Add: Other income Earnings before interest and tax Less: Interest expenses Earnings before tax Less : Taxes Net income 2017 Rs 4,442,375 2016 Rs 3,946,476 2,283,003 32,987 1,483,299 Rs 643,086 626,332 Rs 1,269,418 8,724 Rs 1,260,694 295,465 Rs 965,229 2,006,171 26,434 1,012,699 Rs 901,172 512,725 Rs 1,413,897 6,417 Rs 1,407,480 285,802 Rs 1,121,678 Types of Financial Ratios Liquidity ratios Assets management ratios Debt management ratios Profitability ratios Market value ratios Liquidity Ratios The ratios used to assess the short-term solvency position of a firm. Measure a firm's ability to pay its short-term obligations out of current or liquid assets. Two Measures of Liquidity are: As a conventional rule, the current ratio of 2:1 and quick ratio of 1:1 is employed as a standard of comparison. However, these are only quantitative measures Problem Solving Please solve Problem 2.1, 2.2 and 2.3 to illustrate and interpret current and quick ratio Asset Management Ratios Asset management ratios are also known as turnover ratios or activity ratios or efficiency ratios. The ratios measuring the effectiveness of firm’s assets utilization. If high amount of funds are tied up in certain types of assets that could otherwise be employed more productively elsewhere, the firm is not as profitable as it should be. Inventory Turnover ratio (ITOR) - measures how a firm's investment in inventory is being used for generating sales. It is the test of the liquidity of firm's investment in inventories. A low inventory turnover ratio indicates that the firm is holding excessive stock of inventory or is unable to turn it over into sales. Receivable Turnover Ratio - The ratio that indicates the number of times the firm collects its accounts receivable during the year. A low receivable turnover ratio indicates that the firm is making excessive investment in receivables or it is unable to make timely collection of credit sales. Days sales outstanding (DSO) - The average length of time in terms of number of days that a firm must wait for receiving back cash after making sale. A higher average collection period indicates that customers are not paying their bills in time. Fixed Assets Turnover Ratio (FATOR) - The measurement of effectiveness of firm's ability to make efficient utilization of fixed assets. A low fixed assets turnover ratio indicates that the firm is using its fixed assets not as efficiently as other firm in the industry. It points out that the firm needs to re-evaluate overall strategies, marketing efforts and capital expenditure program. Total assets turnover ratio (TATOR) - Measures the efficiency of assets management in relation to all of the firm's assets. Problem Solving Please solve Problem 2.4 and 2.5 to illustrate and interpret various types of asset management ratio Debt Management Ratios Also known as leverage ratios, indicate the extent to which debt financing is being used by a firm. Measure of long-term solvency of a firm. Used to analyze long-term solvency position from two prospects: first, how firm is using the borrowed funds to finance its assets; second, how far the firm is able to serve its debt in terms of satisfying fixed interest charges. Debt-asset ratio (DA)- Shows the proportion of total debt used to finance total assets of a firm. Total debt consists of long-term debt, notes payable and other interest-bearing debt instruments. Non-interest bearing liabilities are excluded from total debt. Low debt-asset ratio provides a cushion of protection against possible losses at the time of liquidation. However, from the firm's management point of view, the firm with low debt ratio is not able to take leverage advantages of debt. Debt-equity ratio (DE)- The relationship between debt capital and equity capital, and reflects the relative claim of them on the assets of the firm. Total common equity includes paid up capital, share premium, and any balance of undistributed profits net of fictitious assets. Used to analyze financial risk both by creditors and the firm. A high debt-equity ratio indicates higher contribution of creditors towards total financing of the firm. A high debt-equity ratio of a firm is riskier to creditors as the firm may be unable to satisfy their claim. Creditors may put unnecessary pressure and intervene into firm's management with a high DE ratio. Equity multiplier (EM)- Also known as the leverage factor, measures the extent to which the total asset of a firm is greater than the firm's common equity capital. Market Debt Ratio - The debt ratio expressed in terms of market value. Market value of equity is the number of shares outstanding multiplied by market price per share. It is not common to find the market value of debt. So, financial analysts can use value of debt reported in the financial statements. Liabilities-to-assets-ratio - Debt ratio expressed as the ratio of total liabilities used by firm to its total assets. Shows the extent to which firm’s assets are not financed by equity. The total liabilities include all interest –bearing and non-interest bearing liabilities. Interest Coverage Ratio - Indicates the extent to which the firm is able to satisfy interest payments out of EBIT EBITDA coverage ratio- evaluates the firm's debt serving capacity out of all the cash flow available to service debt. Problem Solving Please solve Problem 2.6, 2.7, 2.8, and 2.9 to illustrate and interpret various types of debt management ratios Profitability Ratios Profitability is the end result of a number of corporate policies and decisions. It measures how effectively the firm is being operated and managed. Owners and managers of a firm are interested to know the profit earning capacity of the firm. Following are the major ratios used to measure the profitability of a firm: Net profit margin - The ratio between net income available to common stockholders and sales of a firm. It shows the firm’s ability to generate net income per rupee of sales. Higher net profit margin is desirable for a firm. It shows the operating efficiency of generating net income per rupee of sales. Gross profit margin - The ratio between gross profit and sales of a firm and shows the firm’s efficiency to generate the amount in gross profit per rupee of sales. It is calculated as: Higher gross profit margin indicates that the firm’s cost of goods sold is relatively lower Operating profit margin (OPM) - The relationship between operating profit (EBIT) and sales. It shows the pure operating efficiency of a firm as it measures only the profits earned on operation and ignores interests and taxes. Basic Earning Power - The ratio of firm’s earnings before interest and tax to total assets… Used to evaluate the firm’s ability to generate profit before the payment of interest and taxes out of the assets used. Return on Assets (ROA) - Measures the overall effectiveness of management in generating profit with its available assets. The higher the firm's return on assets the better it is doing in operation and vice versa. Return on Common Equity (ROE) - Measures the return on the owner's investment in the firm. Higher ratio of return on equity is better for owner. It is calculated as net income available to common stockholders divided by common equity. Market Value Ratios The market value ratios are used to assess firm’s stock price in relation to its earnings and book value of shares. Price-Earning Ratio (PE) – Represents the amount per share that investors are willing to pay for each rupee of the firm's earnings. The higher PE ratio indicates the greater confidence of investor in the firm's future. Market-to-book ratio - Measures the extent to which the financial market has added value to the management and efficiency over the time. firm's overall Price-to -cash flow ratio- The ratio of market price per share to cash flow per share. Market price of a firm’s shares of stock largely depends on the firm’s ability to generate cash flows. Higher price to cash flow ratio shows better growth prospects of a firm. Problem Solving Solve Chapter end Problem 2.10 to 2.15 to illustrate and interpret several profitability ratios and market value ratios Also solve remaining Integrated Chapter Problems covering all ratio calculations. DuPont Equation DuPont System - A system of financial analysis used for classified assessment of firm's financial performance Presents an integrated view on financial analysis, planning and control process of a firm. First propounded and used by DuPont Corporation. More popular for making classified assessment of financial performance of a firm. Provides a summary of firm's profitability in terms of return on assets (ROA) and return on equity (ROE). Simple DuPont Equation ROA = Profit margin x Assets turnover Extended DuPont Equation ROE = Profit margin x Assets turnover x Equity multiplier The DuPont analysis looks at the three main components of ROE Profit margin Total assets turnover Financial leverage Profit margin is a measure of the firm’s operating efficiency – how well does it control costs Total asset turnover is a measure of the firm’s asset use efficiency – how well does it manage its assets Equity multiplier is a measure of the firm’s financial leverage Comparative Ratios and Benchmarking Financial performance analysis by using financial ratios requires a comparison of ratios of the firm with similar other firms in the industry or industry average. Compare their financial ratios against other smaller and larger firms in the same line of business. This technique of comparing financial ratios is called ‘benchmarking’ and the firms being used in comparison are called ‘benchmark firm’. For example, Standard Chartered Bank Nepal Limited may benchmark against Himalayan Limited and Everest Bank Limited. Bank Limited, Nabil Bank In the process of benchmarking, some key financial ratios are compared against those of benchmark firms, which allow the management to compare different aspects of financial performance on a firm-to-firm basis. In selecting benchmark firm, it should be noted that comparative ratios of the benchmark firm have consistent emphasis as that of own firm. Besides, the ratios being used for comparison must hold the same definition as that of benchmark firm. Uses of Financial Ratios Useful to various stakeholders. Useful in vertical and horizontal analysis. Useful in internal and external comparison. Useful in evaluation managerial performance Limitations of Ratio Analysis Requires basis of comparison. Differences in interpretation. Difference in situation of two firms. Change in price level. Short-term changes. No indication of the future Common Size Statements The financial statement that expresses all items in percentage terms of some common standard item such as sales for income statement and total assets for balance sheet. Useful to compare when two firms have different size or the size of a single firm changes over different point in time. For example, if we compare the financial performance of Microsoft Company of the USA against the financial performance of Mercantile Computers of Nepal; a direct comparison is meaningless. In case of common size balance sheet, all items are expressed as a percentage of total assets. For income statement, all items are expressed as a percentage of total sales revenue. Table 2.3 Common Size Balance Sheet of Unilever Nepal Limited as of Mid-July ASSETS Net fixed assets Current Assets: Inventories Accounts receivable Short-term investments Cash and cash equivalents Bank balance other than CCE Total Current Assets Total Assets EQUITY AND LIABILITIES Equity: Share Capital Retained earnings Total Common Equity Long-term debt Current Liabilities: Accounts payables Accruals Notes payables Total Current Liabilities Total Liabilities Total Equity and Liabilities 2017 17.5% 2016 16.1% 18.7% 20.5% 34.9% 7.3% 1.1% 82.5% 100.0% 2017 22.1% 9.8% 34.0% 17.0% 1.0% 83.9% 100.0% 2016 2.8% 59.7% 62.4% 0.4% 3.0% 64.2% 67.3% 0.4% 30.7% 4.8% 1.7% 37.2% 37.6% 100.0% 29.6% 1.4% 1.3% 32.4% 32.7% 100.0% Table 2.4 Common Size Income Statement of Unilever Nepal Limited as of Mid-July Sales revenue Less: Cost of goods sold except depreciation Depreciation and amortization Other operating expenses Net operating income Add: Other income Earnings before interest and tax Less: Interest expenses Earnings before tax Less : Taxes Net income 2017 100.0% 2016 100.0% 51.4% 0.7% 33.4% 14.5% 14.1% 28.6% 0.2% 28.4% 6.7% 21.7% 50.8% 0.7% 25.7% 22.8% 13.0% 35.8% 0.2% 35.7% 7.2% 28.4% Percentage Change Analysis Each item in balance sheet and income statement are expressed as a percentage change against a base year. Consider Table 2.5, which shows the percentage change in income statement figures of Unilever Nepal Limited in the year 2017 as compared to 2016. Table 2.5 Income Statement: Percentage Change Analysis Sales revenue Cost of goods sold except depreciation Depreciation and amortization Other operating expenses Net operating income Other income Earnings before interest and tax Interest expenses Earnings before tax Taxes Net income Percentage Change in 2017 12.6% 13.8% 24.8% 46.5% (28.6%) 22.2% (10.2%) 36.0% (10.4%) 3.4% (13.9%) Trend Analysis A tool of financial analysis that indicates whether the financial condition of a firm is likely to improve or deteriorate. By trend analysis, we look pattern of particular financial ratios whether they are increasing or decreasing over the years. A financial ratio of the firm is plotted against that of industry movement average is to confirmed industry average. identify or whether contradicted the to Figure 2.2: Trend Analysis of Profit Margin Ratio over 2012-2017 Profit Margin (%) Firm 12% Industry Average 10% 2012 2013 2014 2015 2016 2017 END