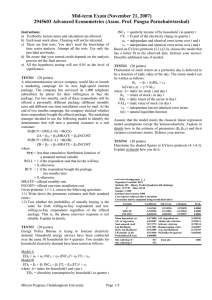

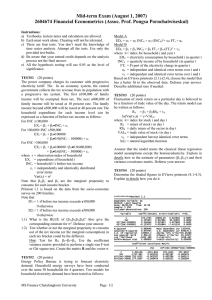

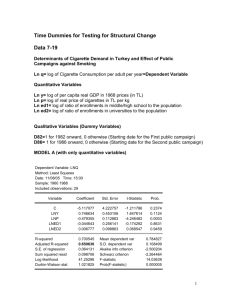

Assignment 4 FIN 690 This assignment must be submitted as a single Microsoft Word docx file through the assignment link in this module. Download this file and rename it to follow the naming convention LastNameFirstInitialAssigt4.docx. For example, if I were submitting an exam, it would be named NelsonHAssig1.docx. General requirements for all assignments You must use Eviews to complete the assignment. The Eviews output must be copy-pasted into your assignment. Work done in Excel is not acceptable. You must use the equation editor to write any equations which may be required in your submission. Equations written in plain text are not acceptable. You must provide explanatory material interwoven with whatever tables, equations and/or graphs are needed. Place your work in the designated locations. Assigned Problems Q4.1 Replicate the regression output on page 159 of the text and place your output here. Breusch-Godfrey Serial Correlation LM Test: F-statistic Obs*R-squared 1.497460 15.15657 Prob. F(10,234) Prob. Chi-Square(10) 0.1410 0.1265 Test Equation: Dependent Variable: RESID Method: Least Squares Date: 07/14/14 Time: 00:30 Sample: 1986M05 2007M04 Included observations: 252 Presample missing value lagged residuals set to zero. Variable Coefficient Std. Error t-Statistic Prob. C ERSANDP DPROD DCREDIT DINFLATION DMONEY DSPREAD RTERM RESID(-1) RESID(-2) RESID(-3) RESID(-4) RESID(-5) RESID(-6) RESID(-7) RESID(-8) RESID(-9) RESID(-10) 0.087053 -0.021725 -0.036054 -9.64E-06 -0.364149 0.225441 0.202672 -0.199640 -0.126780 -0.063949 -0.038450 -0.120761 -0.126731 -0.090371 -0.071404 -0.119176 -0.138430 -0.060578 1.461517 0.204588 0.510873 0.000162 3.010661 0.718175 13.70006 3.363238 0.065774 0.066995 0.065536 0.065906 0.065253 0.066169 0.065761 0.065926 0.066121 0.065682 0.059563 -0.106187 -0.070573 -0.059419 -0.120953 0.313909 0.014794 -0.059360 -1.927509 -0.954537 -0.586694 -1.832335 -1.942152 -1.365755 -1.085803 -1.807717 -2.093571 -0.922301 0.9526 0.9155 0.9438 0.9527 0.9038 0.7539 0.9882 0.9527 0.0551 0.3408 0.5580 0.0682 0.0533 0.1733 0.2787 0.0719 0.0374 0.3573 R-squared Adjusted R-squared S.E. of regression Sum squared resid Log likelihood F-statistic Prob(F-statistic) 0.060145 -0.008135 13.80959 44624.90 -1009.826 0.880859 0.597301 Mean dependent var S.D. dependent var Akaike info criterion Schwarz criterion Hannan-Quinn criter. Durbin-Watson stat -1.94E-16 13.75376 8.157352 8.409454 8.258793 2.013727 Q4.2 Then answer the question in the last sentence on page 159. The conclusion from both versions of the test in this case is that the null hypothesis of no autocorrelation should not be rejected. Does this agree with the DW test result? The Durbin-Watson statistic is equal to 2.013727; when the DW is near 2 this means there is little evidence of autocorrelation and the null hypothesis would not be rejected. Q4.3 Replicate the regression results on page 169 of the text and place your output here. Dependent Variable: ERMSOFT Method: Least Squares Date: 07/14/14 Time: 02:28 Sample (adjusted): 1986M05 2007M04 Included observations: 252 after adjustments White heteroskedasticity-consistent standard errors & covariance Variable Coefficient Std. Error t-Statistic Prob. C ERSANDP DPROD DCREDIT DINFLATION DMONEY DSPREAD RTERM FEB98DUM FEB03DUM -0.086606 1.547971 0.455015 -5.92E-05 4.913297 -1.430608 8.624895 6.893754 -69.14177 -68.24391 1.458963 0.182655 0.336288 0.000149 2.318278 0.762907 8.961837 2.561914 1.567592 1.415784 -0.059361 8.474848 1.353050 -0.397263 2.119373 -1.875206 0.962403 2.690861 -44.10699 -48.20221 0.9527 0.0000 0.1773 0.6915 0.0351 0.0620 0.3368 0.0076 0.0000 0.0000 R-squared Adjusted R-squared S.E. of regression Sum squared resid Log likelihood F-statistic Prob(F-statistic) 0.358962 0.335122 12.56643 38215.45 -990.2898 15.05697 0.000000 Mean dependent var S.D. dependent var Akaike info criterion Schwarz criterion Hannan-Quinn criter. Durbin-Watson stat -0.420803 15.41135 7.938808 8.078865 7.995164 2.142031 Q4.4 Read the second paragraph on page 170. Then add one additional dummy variable to eliminate an outlying observation. How much improvement did you see? 40 Series: Residuals Sample 1986M05 2007M04 Observations 252 30 Mean Median Maximum Minimum Std. Dev. Skewness Kurtosis 20 10 Jarque-Bera Probability -3.69e-16 0.924395 24.32716 -58.99873 11.78726 -2.033978 11.05478 854.9910 0.000000 0 -60 -50 -40 -30 -20 -10 0 10 20 I created another table for ermsoft , then looked for another outlier which I found to be April 1990 (-57). I then created a dummy variable for this and achieved this result: Dependent Variable: ERMSOFT Method: Least Squares Date: 07/14/14 Time: 02:43 Sample (adjusted): 1986M05 2007M04 Included observations: 252 after adjustments White heteroskedasticity-consistent standard errors & covariance Variable Coefficient Std. Error t-Statistic Prob. C ERSANDP DPROD DCREDIT DINFLATION DMONEY DSPREAD RTERM FEB98DUM FEB03DUM APR90DUM 0.569156 1.496274 0.338132 -0.000112 4.074575 -1.324322 7.970906 6.954852 -68.96408 -68.16981 -58.50680 1.319854 0.170651 0.317837 0.000141 2.164847 0.760826 8.937300 2.569879 1.537527 1.424409 1.842768 0.431227 8.768054 1.063854 -0.791244 1.882154 -1.740638 0.891870 2.706295 -44.85391 -47.85831 -31.74942 0.6667 0.0000 0.2885 0.4296 0.0610 0.0830 0.3734 0.0073 0.0000 0.0000 0.0000 R-squared Adjusted R-squared S.E. of regression Sum squared resid Log likelihood F-statistic Prob(F-statistic) 0.415015 0.390742 12.02933 34873.84 -978.7605 17.09765 0.000000 Mean dependent var S.D. dependent var Akaike info criterion Schwarz criterion Hannan-Quinn criter. Durbin-Watson stat -0.420803 15.41135 7.855242 8.009304 7.917233 2.109565 The Bera-Jarque test had value of 855, showing it was moved farther away from a normal distribution. My conclusion is that it is not possible to achieve normal residual in this case and that three dummy variables it is too excessive under the circumstances.