Intermediate Accounting III, Study Guide for Test 1, Chapters 16...

advertisement

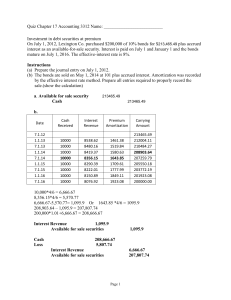

Intermediate Accounting III, Study Guide for Test 1, Chapters 16 & 17 I would be negligent if I did not point out that the questions below relate mostly to theory and concepts. However, the bulk of the points on the test will come from applying theory (problems, journal entries, etc.). Therefore, it would behoove you to review your assignment problems as well as the questions below. Two review problems have been provided at the end of this document, which should serve you well if you take the time to do them. Chapter 16 1. How are convertible bonds accounted for (a) at date of issuance, (b) at date of conversion (c) at date of retirement? Are (a) and (c) handled the same as regular bonds? How is any cash “sweetener” that is provided with the bonds accounted for? 2. How is convertible preferred stock accounted for? If warrants are issued together with other securities and are non-detachable, how are they accounted for? Know both proptionIf they are detachable, must the values between the equity and debt portions be split using relative market values? 3. Be able to intelligently discuss the debate that has occurred regarding stock options. How does the intrinsic value of stock options differ from their fair value? Why has Congress been involved? What approach to valuing stock option compensation does the FASB now require? Why are some businesses opposed? What industry is the primary opposition to expensing options at fair value? What are the main arguments for and against expensing stocks options at fair value? 4. Be able to intelligently discuss the recent backdating scandal with stock options. How does backdating stock options benefit the executives who get the options? Why is it considered illegal? 5. Be able to prepare journal entries to record the expensing of stock option compensation according to fair value. Pay attention to the grant date, exercise date, and service period. 6. Why is restricted stock becoming more popular than stock options as a way for employers to compensate employees? How does the accounting for restricted stock compensation differ from the accounting for stock option compensation? 7. How do IFRS differ from U.S. GAAP for the concepts in this chapter? 8. Why are investors interesting in seeing both basic and diluted earnings per share? What does diluted EPS indicate to an investor? Review the problems on earnings per share. Be able to do similar problems to those on your assignment and the handout/review problems. You need to be able to work a problem where there are several different kinds of dilutive securities at the same time. There may also be theory questions as well; for example, T or F: stock options always have a dilutive effect on EPS when exercised. Chapter 17 9. How do debt securities differ from equity securities? 10. What criteria must be met for a security to be classified as HTM? How are HTM securities valued on the balance sheet? Why is no unrealized gain/loss recorded for HTM securities? Can common stock be considered HTM? 11. How are available-for-sale securities defined? How are they valued on the balance sheet date? Where is the unrealized gain or loss recorded? What rationale could possible justify unrealized gains/losses bypassing the income statement? 12. How are trading securities defined? How are they valued on the balance sheet date? Where is the unrealized gain or loss recorded? 13. Are premiums or discounts on debt investments (e.g. bonds) usually recorded in a separate account? Review again how premium/discount amortization is determined. Which method (straight-line or effective interest) is always considered GAAP (no exceptions)? 14. Be able to account for accrued interest when bonds are purchased or sold in between interest payment dates. For purchases, note that interest revenue or receivable can be debited, whichever meets your fancy. 15. How are equity securities defined? Note how the various percentages of ownership require different accounting treatment. Percentages over 20% (equity method & consolidations) will be tackled in Advanced Accounting, so you can ignore these topics for this class. 16. If securities are non-marketable, on what basis should they be recorded? 17. Does the cost basis when buying securities include brokerage fees and other transaction costs or are 18. 19. 20. 21. 22. 23. 24. 25. brokerage fees expensed? How are brokerage fees handled on the sale of securities? Be able to do a problem that includes both debt and equity securities and that involves all three possible classifications (HTM, AFS and Trading). What is comprehensive income and how does it differ from net income? Why did the FASB create comprehensive income? Under the rarely-used fair value option, how does the reporting of unrealized gains/losses for AFS securities differ from that of regular accounting? If a decline in market value is considered permanent, what entry needs to occur to record this impairment of value? Is the gain/loss recorded on the income statement? What happens to the carrying value (basis) of the investment on the balance sheet? How are transfers of securities between categories accounted for? For example, what happens to the unrealized gain for a security that is transferred from trading to AFS? What about vice versa? Why should transfers from HTM to another category be rare? What is “cherry-picking” or “gains trading”? Is it legal? See ethical case assigned for this chapter. How do IFRS differ from U.S. GAAP for the concepts in this chapter? What is a derivative security? What are three examples? What purposes do they serve? How does a hedger differ from a speculator or an arbitrageur? Be able to prepare journal entries for the purchase, revaluation, exercise, and settlement of a simple call option, such as we did in E17-26. Good luck! And yes, you can bring a 3” by 5” card with as much scribble on both sides as can fit. Some review problems have been provided below for your personal pleasure and amusement. Intermediate Accounting, Ch. 16, Review Problem Net income for the year is $1,500,000, including extraordinary gain of $500,000 (net of tax) Common share activity during the year: Jan. 1, 200,000 shares outstanding Apr. 1, issued 20,000 shares Sept. 1, purchased 30,000 shares Dec. 1, two-for-one stock split declared/issued Options A: During the year, 10,000 options existed to buy common stock at an exercise price of $60. The average stock price was $50 during year. No options were actually exercised. Options B: On July 1 of this year, 300,000 options were granted to buy common stock at an exercise price of $40. The average stock price was $50 during year. No options were actually exercised. Convertible preferred stock: During year, there were 20,000 shares of noncumulative convertible preferred stock, $100 par, 3% dividend, convertible into four shares of common stock. A preferred dividend was declared and paid during the year. Convertible bonds: $2 million carrying value, 8% convertible bonds existed during the year, each with a $1,000 face value and convertible into 100 shares of common stock. None were actually converted. Tax rate is 40%. Instructions: Show how EPS are calculated and how they should appear on the face of the income statement for the year. (Note: assume the stock split is already factored into all conversion figures related to potentially diluted securities.) Check figures: BEPS DEPS Income from cont. operations 2.29 1.619 Extraordinary Gain 1.22 0.781 Net Income 3.51 2.400 ACCT323, Ch. 17, Review Problem Bell Company started business during the year. At the end of its first fiscal year, it had the following marketable securities: Cost 100 shares of Denson Company common stock 400 shares of Republic Inc. common stock Total Per Share $43.25 $ 5.60 Total $4,325 $2,240 $6,565 Market Value Per Share Total $31.15 $3,115 $ 6.10 $2,440 $5,555 During the year, the following transactions took place: 1. Feb. 16 - Sold 80 shares of Denson common stock for $45.70 per share, less brokerage fees of $37. 2. May 10 - Cash dividends of $1.00 per share were received on the Denson common stock. None of the other investments paid dividends. 3. July 1 - Purchased one hundred, 10%, Smith Company bonds with a remaining life of 10 years at a price of 98, plus accrued interest. Each bond has a face value of $1,000. Interest is payable April 1 and October 1 of each year. Smith uses the straight-line method for amortizing any premiums or discounts. 4. Oct. 1 - Received the semiannual interest on Smith bonds and amortized any premiums or discounts. 5. Dec. 27 - Purchased 300 shares of Evans Co. common stock at $40 per share, plus brokerage fees of $160. 6. Dec. 31- Recorded any accruals of interest and amortizations needed to bring accounts up-to-date. At the end of the year, the market values of the investments were: Denson Company common stock, $38 per share Republic Inc. common stock, $6 per share Evans Company common stock, $42 per share Smith Company bonds, 95 Bell has the following intentions regarding its investments: -- Denson and Republic common stock are both ready for sale when the price is right, which may be tomorrow or next year. -- Evans common stock will be sold within a few days, so that a capital gain can be earned on short-term price differences. -- Smith bonds will be held until they mature. None of the investments in stock constitute an ownership level of more than five percent of the investee’s outstanding stock. Instructions: Prepare the general journal entries to record all the transactions during the year. For any unrealized gains or losses, make it clear whether they appear on the income statement or on the balance sheet. Check figure: total interest income for the year is $5100 (-2500+5000+50+2500+50); total realized gain is $159; total unrealized gains are $440 on the income statement and $1065 in OCI.