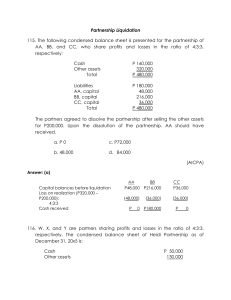

Partnership Liquidation: Chapter Outline

advertisement

Chapter 16 PARTNERSHIP LIQUIDATION Comprehensive Chapter Outline PARTNERSHIP LIQUIDATION IS THE TERMINATION OF A PARTNERSHIP AS A BUSINESS ENTITY. A B Overview of liquidation process for a solvent partnership (partnership assets are greater than partnership liabilities): 1 Noncash assets are converted into cash. 2 Gains and losses and liquidating expenses incurred during the liquidation period are recognized. 3 Liabilities are settled. 4 Cash is distributed to the partners according to the final balances in their capital accounts. Order of distribution of assets in a liquidation of a partnership (from the Uniform Partnership Act): 1 Amounts owed to creditors other than partners 2 Amounts owed to partners other than for capital and profits 3 a No distribution should be made to a partner with a negative capital balance b Partners’ loan balances should be offset against capital balances in determining distributions to partners (see exception for a partner with a debit capital balance) c A partner’s loan balance should be charged before his/her capital balance is reduced by a distribution Amounts due to partners with respect to their capital interests [All profits, losses, and drawing balances are closed to capital accounts before any distributions are made.] C Partnership liquidation statement is a summary of transactions and balances during the liquidation stage. D Debit capital balances in a solvent partnership may result from recognizing losses during the liquidation process. 1 The partners with debit balances are obligated to use their personal assets to settle their partnership obligations. 2 If the partners with debit capital balances have inadequate personal assets, the partners with credit balances assume losses equal to the debit capital balances and share the losses in their relative profit and loss sharing ratios. 3 If the partnership has a loan balance from an insolvent partner: a No cash should be distributed for the loan without agreement from all partners. b A partner’s personal creditors have a prior claim on personal assets. SAFE PAYMENTS ARE DISTRIBUTIONS TO PARTNERS THAT CAN BE MADE WITH ASSURANCE THAT THE RESOURCES DISTRIBUTED WILL NOT HAVE TO BE RETURNED TO THE PARTNERSHIP (Illustration 16-1) A B In calculating safe payments, the following assumptions are made: 1 All partners are considered personally insolvent. 2 All noncash assets are considered losses. 3 Some cash may be withheld to cover liquidating expenses, unrecorded liabilities, and general contingencies. The cash withheld is considered a loss in determining safe payments. The safe payments schedule for determining advance distributions to partners is prepared after nonpartner liabilities have been paid. 1 The schedule begins with partners’ equity which is each partner’s capital account plus loans to the partnership and less loans from the partnership. 2 Possible losses (from noncash assets and cash withheld balances) are allocated to the partners in the profit and loss sharing ratios and deducted from the equity balances. 3 Any negative partner equity is allocated to partners with equity in their relative profit and loss sharing ratios. 4 Step 3 is repeated until no remaining partner shows negative equity. 5 The amount shown for partners with equity will equal the cash available for distribution. 6 Advance distributions require approval from all partners.