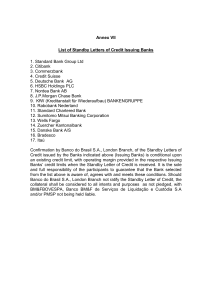

FINANCIAL STABILITY REPORT M a y 2 0 1 3

advertisement